03.08.2026: Ideas For The Upcoming Week

We’ve finally seen a weekly close below the 8 and 21 MA and a few daily closes below the 100 MA. The 200 daily MA currently sits at ~656 which would be a drop of ~2.5% from today’s level which seems completely feasible. The last time we broke the 200 daily on the SPY was March 7th 2025, almost 12 months ago exactly and from there the index fell another 15.4% before eventually recovering.

The QQQ actually looks a little better than the SPY at the moment. It’s been more range bound and has held structure a bit more the last couple weeks, though it remains below the 100 daily and also ~2% from a break of the 200 daily.

Definitely something to track.

Before we get into my 3 ideas for the week, take a look at my March database and portfolio. You get:

Portfolio (real monetary amounts with 100% transparency)

Watchlist

Theme tracker

Valuation models

10+ themes with stocks per theme measured by valuation

Daily notes in the paid chat

1 video chart review per week

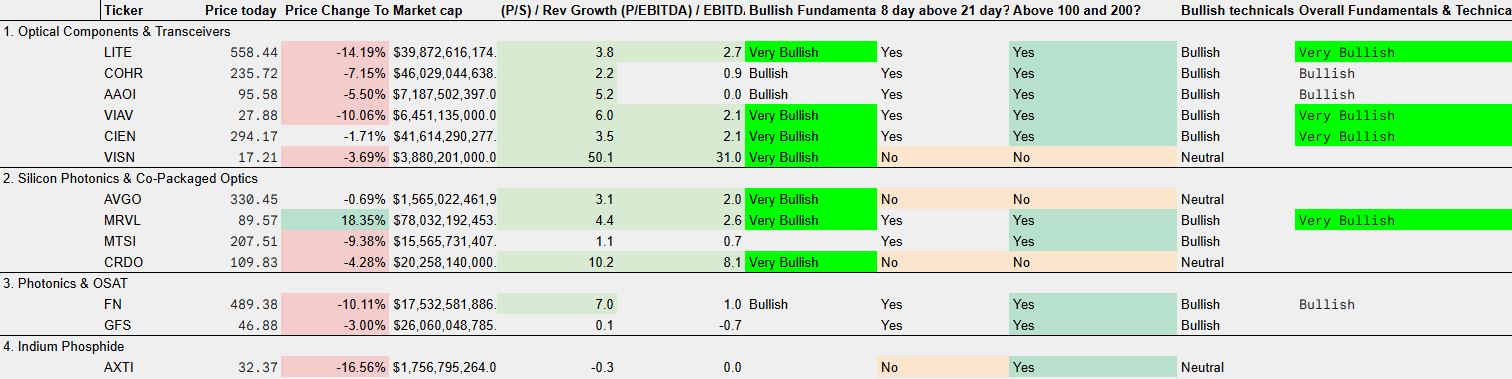

I also want to give an example of one of the many tabs within my portfolio. Here’s the optics tab:

I created this back in December 2025 before LITE and AAOI had their massive runs. It gives you a list of all the stocks within the theme measured by revenue and growth rates relative to multiples and also combines that with where the stock is trading technically vs key MA’s.

As you can see, LITE, VIAV, CIEN, and MRVL are still currently showing as very bullish. Outside of CRDO which I currently own, I think MRVL is my next favorite.

The reason I give access to all this data (and this tab is one of 10+ right now) is because I know we all invest in different ways. I offer complete transparency to my portfolio and my watchlist but I also offer you this extra benefit.

Stock picks are everywhere now. Having access to a nice quick screen is just an added benefit.

Defensive Idea

XLU & ITRI

Two weeks ago, I spoke about XLU (S&P 500 Utilities Sector ETF) and some of the key players within this theme. Today, I’m reiterating this as a great long-term hold for the next 3-5 years and one to keep watching into this week.

XLU is a simple rate cut utilities trade combined with a bet on continued AI CapEx. XLU saw a 30% move in 1995, and another sizable gain in 1996 as well as a 26% gain in 2019 during the mid-cycle cut. I think 2026 and 2027 is very likely to be a repeat story and this is before talking about huge AI CapEx.

What is structurally new in 2026/2027 compared to 1995 and 2019 is the scale and urgency of data center and AI demand which is turning boring utility companies into huge bottlenecks that the AI cycle is reliant on. Global CapEx has been predicted to be upwards of $1.7T by 2030 which seems completely feasible given $600B is being spent in 2026 by the top 4 US hyperscalers alone. That’s why players like Goldman are predicting data center power demand to increase by ~165% by 2030.

All of this incremental demand has to flow through the utilities and merchant generators. Paid subs will know that I’m currently not an owner of XLU but I am an owner of a stock within the wider sector: ITRI.

ITRI builds the smart meters, and grid-edge hardware and software that lets utilities turn an aged, and overloaded grid into a data-driven network. It modernises the grid.

It’s also now layering AI and ML on top of its data driven network with partnerships with NVDA, MSFT, and AWS. If you want a safer play, I think the XLU ETF is always going to be safer…but if you want an individual name that offers a nice play on electrification, power grids, AI infrastructure demand, grid congestion, and a play that almost forces utilities to invest in them for modernisation, I think ITRI is that play.

And it trades at just 15x NTM PEwith a historic average between 2021 and 2023 of much higher. Technically, it’s also sitting at a really nice weekly zone as well.

Here’s the NTM PE for ITRI over the last 12 years from Tikr.

Nvidia | NVDA

NVDA’s valuation currently doesn’t make much sense to me and it’s one of the names I’d be more than happy to buy into today at 21.5x NTM PE (for reference the 5Y average is ~38x).

I still believe that the current valuation is missing the growth estimates and it makes it the cheapest Mag 7 stock to own today based on PEG.

As long as NVDA stays above this $170 level marked on the chart above, I’ll be more than happy to buy in more.

The difficult thing is here just deciding where we are in a wider cycle. If we’re set for a ~15-20% index drop from here, NVDA (along with a couple more) is probably one of the safer stocks to own based on multiples, beta, and overall safety. With that being said, the opportunity cost of adding to NVDA here vs many other high growth plays I have on my watchlist (or already in my portfolio) is difficult to gauge.

That’s a decision I’m going to have to make based on price action, geopolitical risk, and a few other factors. I suspect that decision will have to be made quite soon.

Neutral Risk

Three stocks to discuss here:

Nebius | NBIS

NBIS has chopped around for a while now on news from almost anything completely unrelated to NBIS.

ORCL and OpenAI ending plans to expand Texas data center

IREN share dilution

IREN reporting earnings with no new hyperscaler deals

Blue Owl not securing financing for a $4B data center project with CRWV

These are all firm specific issues and unrelated to NBIS. In fact at the Morgan Stanley conference earlier this week, CRO of NBIS said this:

“We’re now securing upfront payments from customers, up to and including, in some cases, customers paying 100% upfront.”

And don’t forget that is essentially 5 different companies all scaling very quickly. It’s far more than a neocloud. I don’t believe the sum of the parts valuation is priced in at all (just like for AMZN).

SoFi Technologies | SOFI

In the past week alone, the CEO of SOFI bought $1M worth of stock and they partnered with Mastercard (MA) to use SoFiUSD within the card network. Quite difficult to gauge the value add of this right now, but most definitely a material value add to the business.

On top of this, here’s a great quote from Noto (CEO):

“In Q1 our revenue growth is 35%… I would be incredibly disappointed if our first quarter was the fastest quarter of the year.”

Valuation wise, SOFI’s forecasts are incredibly good. They’re set to grow EPS at 61% in FY26, and 31% in FY27, and 27% in FY28, all whilst trading at a 31.3x NTM PE. This puts them at a PEG ~0.5x. For reference, I ran a screener on Tikr for stocks growing EPS at +60% with a PE below 35x. Here’s the results (excluding pharma/biotech/mining and with a market cap above $5B):

SOFI (portfolio)

WULF

SANM (portfolio)

IONQ

NVDA (portfolio)

SOLS

AFRM

SE

RKT (portfolio)

LUMN

MU

CRDO (portfolio)

SNDK

Not a bad group of stocks there…

Harrow | HROW

The market seems to be forgetting that forecasts for HROW are $250M in Q4 FY27 revenue or it simply doesn’t believe management will make those numbers. I think that’s partly fair enough considering revised and lowered guidance this quarter, but management seem still on track for this milestone by Q4 2027. IF management hit this revenue milestone, then HROW at $36 is simply too cheap to ignore.

Quarterly revenues are quite lumpy for HROW, so I think $1B in revenue (based on $250M in Q4 FY27) probably is a little optimistic. Anyhow, I think assuming $900M in FY28 revenue is more than reasonable given this guidance.

On top of that, HROW have said margins will be expanding nicely over the next few years so I think the 31.8% analyst estimates for EBITDA margin (compared to 22.7% today) seem fair.

If we get, $900M in revenue in FY28 at 31.8% margins we have $286.2M in EBITDA in FY28 which would be a 66% CAGR. For that we currently have a 18x NTM EBITDA multiple.

If we assume a very conservative 25x multiple (when the market has proof that HROW is putting up those numbers), then 25x on $286M gives an EV of $7.2B which is 4.7x from today.

HROW is currently below the 200 daily but on the weekly still looks absolutely fine right at the 100MA.

Higher Risk (& A Couple of Plays on the Middle East Tensions)