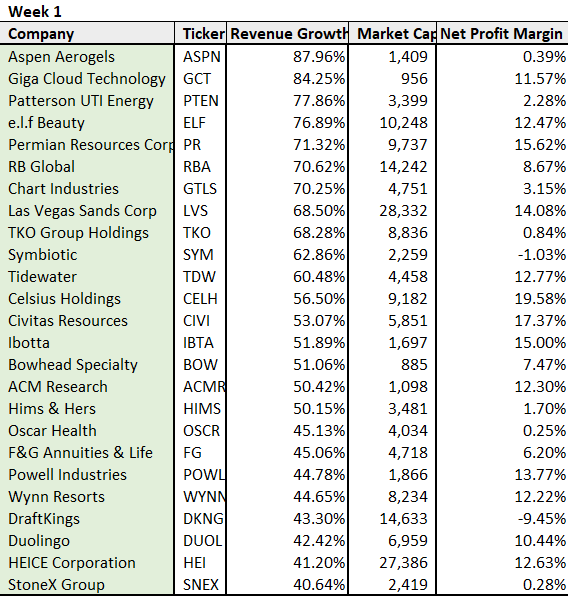

3 High Quality Growth Stocks

+30% Revenue Growth

Hi fellow investors!👋

I’m going to start releasing a short article every Monday with a few quick screens and the results of those screens. For example, I’ll focus on margin expansion, revenue growth, dividends, international growth stories, small caps, large caps, valuations etc etc. It’s a way for us all to introduce ourselves to some potential new gems. Depending on the screen results I’ll then give a bit of information on 3 or 5 of those stocks.

The narrative on the stocks won’t be in depth because I want to keep these article short and snappy and save the details for my deeper dives. Of course if any of these stocks that come up in my screens really interest me, then I’ll do a deeper dive on them at a latter date.

Here’s the details of my screen this week:

Revenue 1Y Growth: Greater than 40%

Market Cap: Greater than $500M

Net Profit Margin: Between -20% to 20%

Note: I excluded any Biotech and Pharma companies because I don’t know much on these and deem these industries too risky for my liking.

Results:

Aspen Aerogels (ASPN)

Company: Aspen Aerogels

Ticker: ASPN

Website: https://www.aerogel.com/

Current Stock Price: $22.99

52-Week High: $31.42

52- Week Low: $5.55

Market Cap: $1.684 billion

Headquarters: Northborough, MA

Number of Employees: 548

Introduction

ASPN develops, manufactures, and sells aerogel materials which are highly valued for their thermal insulation properties. These aerogels are used to create high-performance insulation products and used in many areas such as energy-related industries in pipes and vessels.

ASPN have also more recently become involved in the electric vehicle, and energy storage markets with their PyroThin and Cryogel Z products. They’re managing to become ever more diversified in their products and industries in which they compete in.

Customers of ASPN include huge oil producers, natural gas facilities, and petrochemical plants such as ExxonMobil, Royal Dutch Shell, and Reliance Industries. On top of this they also have clients such as Toyota and General Motors in the EV space.

Numbers

144% YoY revenue growth

14.3% net margin (first profitable quarter in history)

EV/Sales multiple of 5.1x and EV/EBITDA of 49.8x

Investment Thesis

ASPN have struggled to become profitable for many years until Q2 2024 where they managed a 14% net profit margin thanks to higher run rates and a 5% reduction in material costs as a percentage of revenue. This demonstrates that one of the long standing doubts of the company (failure to become profitable) should no longer be a worry.

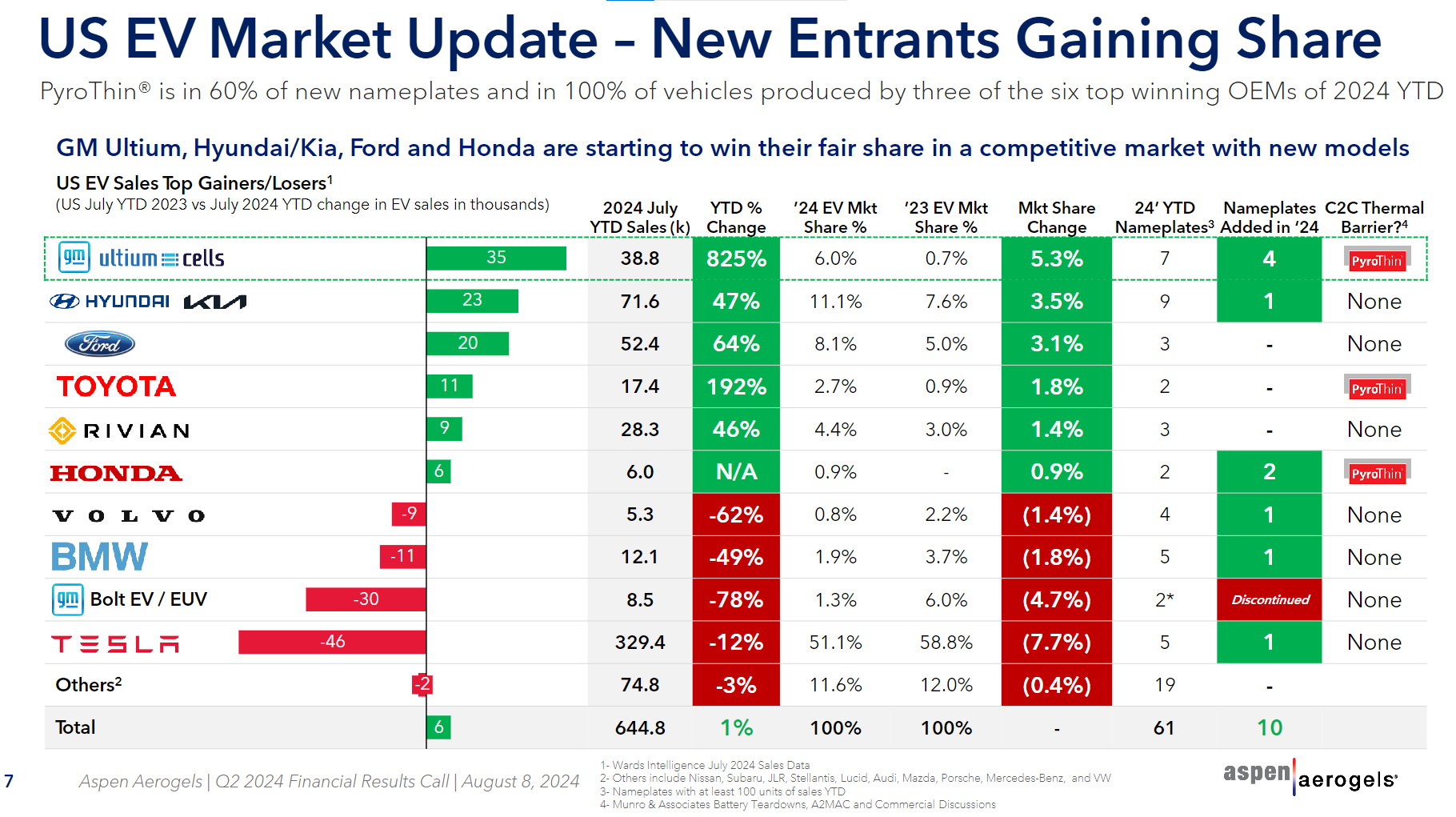

ASPN are becoming a key player in the EV space which despite recent headwinds…is set up for a big future. As EV’s become more popular, so does the increased focus on ensuring safety and reliability of these vehicles and that is where Aspen’s thermal insulation properties can be used to protect all the critical parts of an EV (battery packs, electrical systems etc). ASPN have clients as GM, Toyota, and Honda, all of which are in the top 6 of the highest growth EV brands over the last year.

I’ll likely put ASPN on my deep dive list over the next month, but ultimately the global thermal barrier market is growing at 27% CAGR to hit $9 billion by 2030. Then if you add on the global lithium-ion battery market which has projections of $200 billion by 2030, you’re starting to see just how large the TAM is for ASPN.

DraftKings (DKNG)

Company: DraftKings

Ticker: DKNG

Website: https://draftkings.gcs-web.com/

Current Stock Price: $30.03

52-Week High: $48.68

52- Week Low: $26.37

Market Cap: $14.73 billion

Headquarters: Boston, MA

Number of Employees: 4,400

Introduction

DraftKings is a leading US sports entertainment and gaming company operating in the betting and casino markets. Over the last 2-3 years they’ve gained huge popularity on the legalization of sports betting and hence revenue growth has been 6x since 2020.

Numbers

Revenue has been growing at +45% CAGR but the recent quarter slowed down to 26.2%

Q2 was first profitable quarter at 5.8% net profit margin

DKNG trade at 3.5x EV/Sales

Investment Thesis

Being involved in the sports industry is a fairly solid growth industry as more and more of the population tune in to watch various sports each year. With online streaming allowing the variety of sports to be watched to increase massively, so has the popularity of betting live on those sports.

There’s a pretty direct link between watching sports live and betting on those sports. It’s fun. It’s exciting. And many people with a bit of disposable income do so to make the experience even more thrilling. With constant free bets, bonuses, and other promotions, plus the social nature of sports betting with your friends, it’s rapidly become a very regular activity for many avid sports fans.

Because of this, and much more, online sports betting is projected to grow at 17% annually through to 2028. Further, DKNG are involved in the fantasy sports markets which have a even higher rate of growth at 24% per year. Cumulatively, the TAM for DKNG is huge today but projected to grow significantly over the next decade.

Duolingo (DUOL)

Company: Duolingo

Ticker: DUOL

Website: https://www.duolingo.com/

Current Stock Price: $181.75

52-Week High: $248.84

52- Week Low: $126.61

Market Cap: $8.158 billion

Headquarters: Pittsburgh, PA

Number of Employees: 720

Introduction

DUOL is a leading language learning platform that offers a gamified approach to language education. Using exercises, quizzes, and other game-like features, DUOL caters to pretty much every audience no matter the age of language abilities.

Numbers

41% YoY revenue growth

5 profitable quarters with net margin now at 13.7%

DUOL trades at an EV/Sales of 11.5x

Investment Thesis

DUOL makes money in numerous ways but of course the core is paid subscriptions which has rose at 54% - a similar growth trajectory to the increase in daily active users (DAU). This shows Duolingo’s ability to convert free subscribers onto a paid subscription at a point when use of the free platform becomes slightly too limiting for those daily users.

As mentioned in the introduction section, DUOL have created a product that caters to almost everybody globally. However, they are currently just at the beginning stages of growth in Asia, most particularly Japan and Korea where they have very limited penetration. DUOL didn’t fully start investing into the Asia region until about 2 years ago so they are slightly behind most other places, however, they have proven to possess a very successful international marketing strategy so success in Japan and Korea will lead to huge revenue gains over the next 2-3 years.

Further TAM expansion comes from DUOL’s potential to expand outside of languages. They currently have plans to release an app focused on teaching children literacy skills, mathematics skills, and music skills. This mobile-focused gamified approach to learning is a perfect approach to educating children. Of course, there’s apps out there that already are focused on these niches, but DUOL has the brand power and marketing ability to disrupt these markets as well.

That’s it for the day

I hope you loved this article. As I develop on here, I’m sure there will be some changes to my structure and style, so please do leave some feedback for me.

Please subscribe to my newsletter where I provide investors with all the tools to outperform the market, and retire well before you’re 65. You can also follow me on X.

Own all 3