3 Quality Stocks You Haven't Heard Of

HAFN LTNH ACGL

Hi all👋

This week we are looking at some high growth quality stocks that you likely haven’t heard of. Trust me you’ll want to see these potential gems.

Before that, I want to send a quick apology as I haven’t got a post out in 2 weeks. I’ve been a world traveler in New York, Las Vegas, Madrid, and Paris and thought I’d manage to keep up with everything but I didn’t. With that being said…I did manage to get a few first drafts complete for some posts over the next 2 weeks so you can expect at least 2 a week for the upcoming period.

For this screener I used StocksGuide, a new up and coming stock analysis tool that I’m loving that I think has the best and easiest to use screening tools out there. You can click the link above (it’s an affiliate partnership so just a heads up).

My criteria were as follows:

Market cap: >$2B

Return on equity: >20%

Equity ratio: >25%

Free cash flow margin: >25%

Revenue growth: >10%

PE: <30x

This was an inbuilt screening by StocksGuide and it showed some really nice results.

Of course this screen came back with some well known stocks such as Meta, Evolution AB, Kinsale Capital, DLocal…but I wanted to introduce us all to new companies as that’s the whole purpose of these screens that I do.

Therefore, the 3 stocks I’ve decided to review today are as follows:

Hafnia (HAFN)

Lantheus Holdings (LTNH)

Arch Capital Growth (ACGL)

Hafnia (HAFN)

Company: Hafnia

Ticker: HAFN

Current Stock Price: $7.51

52-Week High: $8.99

52-Week Low: $5.66

Market Cap: $3.66 billion

Headquarters: Singapore

Number of Employees: Not available

Numbers

Revenue growth: 18.58%

Gross profit margin: 40.50%

Net profit margin: 31.18%

EV/Sales: 1.6x

Commentary

HAFN is one of the largest operators of tanker vessels in the world. They mainly transport oil, refined products, and chemicals worldwide using their current fleet of just under 200 vessels. The company was only listed on the NYSE in early 2024 so they’re likely a company that is very under the radar and perhaps offers a nice opportunity.

Over the last year, HAFN has increased 20.5% and 8% YTD which has been mainly driven by the increasing shift of production away from high demand areas like Europe and North America and towards areas such as the Middle East, China, and India. Of course, the main beneficiaries of this shift are the vessel companies that are then in high demand to transport long distances.

There’s also expectations of a seasonal uptick in crude tanker demand along with higher OPEC exports. These increased distances obviously come at increased costs with HAFN now charging out at $34,000 per day with high occupancy around 72% of total days.

These trends have led to some very impressive numbers for HANF which is why it showed up in our screen. A ROE of 44.5%, and ROIC of 31.4%, profit increase of 21%, and a nice growing cash pile aren’t everyday finds. I do think HAFN is a nice investment over the next year or two as these trends continue to increase and HAFN continues to profit.

Valuation

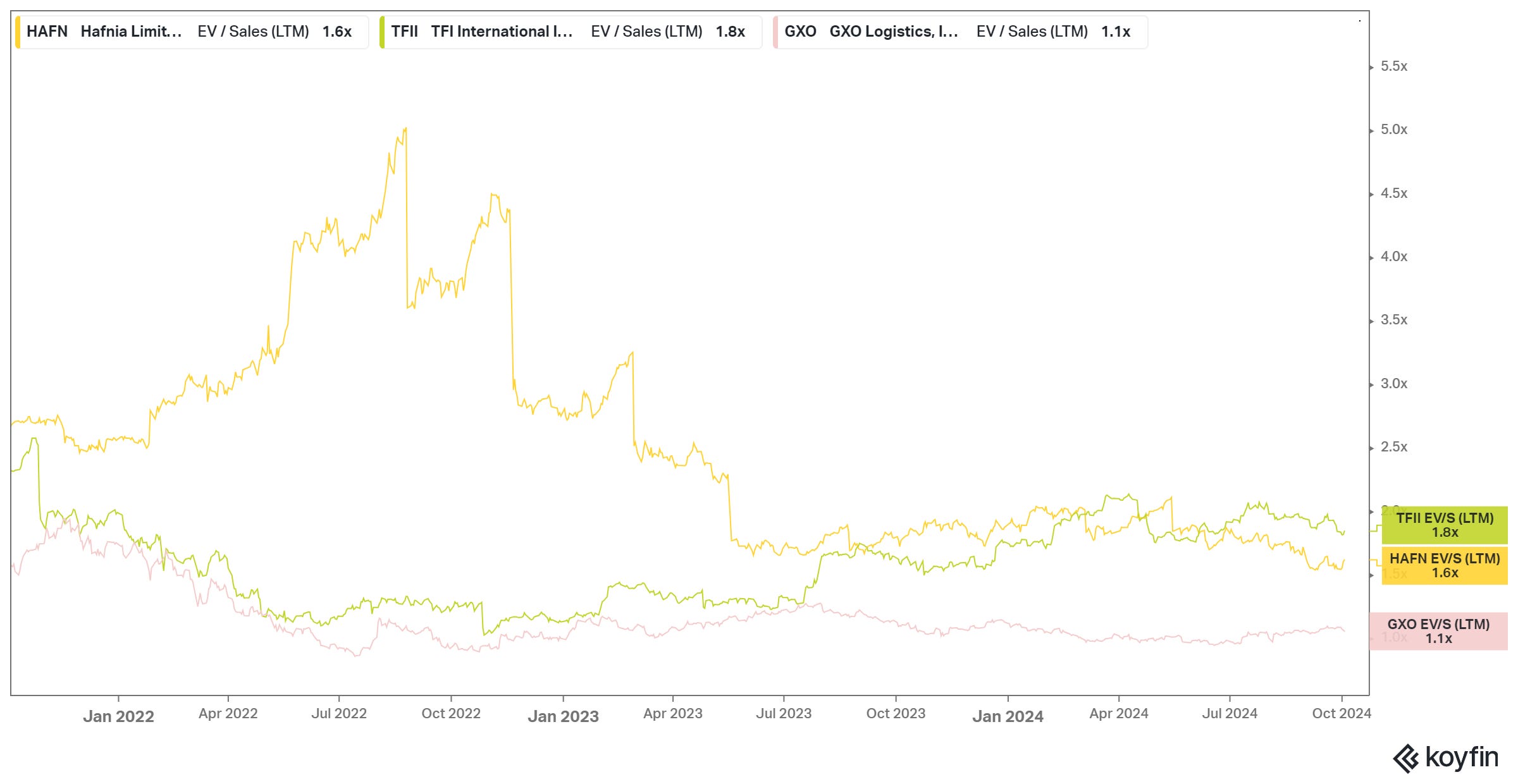

HAFN trades at an EV/Sales multiple of 1.6x for 19% growth which on the face of it seems pretty attractive. Comparing to competitors though HAFN looks slightly less undervalued than I originally thought.

I looked primarily at TFI International and GXO Logistics which both have EV/Sales multiples of 1.8x and 1.1x respectively. TFI (1.8x) has very high revenue growth at 26.5% whilst GXO (1.1x) has revenue growth around 19%, very similar to HAFN. Therefore, an argument could be made that perhaps GXO is valued better, though of course making that decision solely based on revenue growth isn’t intelligent.

Graphic

With the above being said, HAFN is trading at its lowest multiple over the last 3 years.

Lantheus Holdings (LTNH)

Company: Lantheus Holdings

Ticker: LTNH

Current Stock Price: $106.57

52-Week High: $126.89

52-Week Low: $50.20

Market Cap: $7.3 billion

Headquarters: North Billerica, MA

Number of Employees: 834

Numbers

Revenue growth: 22.50%

Gross profit margin: 64.90%

Net profit margin: 15.75%

EV/Sales: 5.0x

Commentary

LNTH caught my eye due to the huge potential, even though I rarely actually look for companies in the pharmaceutical niche. This is mainly because I see clinical trials as way too risky, but LTNH are much more mature than this and already have 3 commercial products on the market (PYLARIFY, DEFINITY, and TechneLite).

PYLARIFY is the main product and using PET imaging to detect recurring cases of prostate cancer - 29% growth.

DEFINITY has 80% market share in their niche of ultrasound agents for echocardiograms - 10% growth.

TechneLite provides the isotope used in nuclear medicine and they are the smallest revenue stream, but they are growing the quickest - 30.5% growth.

LTNH have strong potential to me because of their M&A strategy where they are expanding their pipeline of radiopharmaceutical products that are in the late-stages of clinical testing. This should of course massively diversify their revenue stream as well as avoid the long and painful process of clinical trials.

One of the most exciting possibilities for LTNH is their investment in Alzheimer’s treatment, which is a field that is very new and ready to explode over the coming years. LTNH acquired MK-6240 in 2023, and also just recently acquired NAV-4694, a next gen imaging agent that is targeting beta-amyloid (linked to Alzheimers). These two diagnostic imaging candidates could be huge and LTNH are extremely well positioned if the Alzheimer’s industry does explode like it is expected to.

One of the big risks I see with LTNH is their huge investments into R&D and acquisition costs which of course do not have guaranteed returns at all. Margin and net income could be disrupted substantially if this were the case. There’s no denying that LTNH are playing to win, and if a couple of these investments do play out as management hope then I believe LTNH has substantial upside.

Valuation

LTNH currently trades at $106 which is ~15.8x CY EPS and an EV/Sales of 5.0x. EPS predictions in 2025 are $7.2, and I believe if one or two promising products become commercially available over the next 3 years (I’m mainly thinking about Alzheimers), then there’s no reason EPS can’t be in the $12 range.

This is assuming that revenue growth can stay in the 25% range (average) over the next 3 years meaning we could see $768 million revenue by 2027. At a net income margin of 35% (when R&D and acquisition costs come back down), we have potentially $270 million of net income which is 330% higher than today.

It all depends on the pipeline of products coming through, but I’m quite impressed by management and I have hope that they’ll execute well.

Graphic

This graphic suggests that the price has gone slightly ahead of the revenue growth, but revenue growth for a company like LTNH is not consistent or predictable at all. I think the market is predicting some success for the pipeline of products and that’s why they’re trading at a slightly higher multiple today.

I don’t think there’s a good opportunity to enter into a position now, but any substantial pullback could be interesting. I’ll add this to my waitlist.

Arch Capital Growth (ACGL)

Company: Arch Capital Growth

Ticker: ACGL

Current Stock Price: $112.85

52-Week High: $114.69

52-Week Low: $72.85

Market Cap: $42.6 billion

Headquarters: Hamilton, Bermuda

Number of Employees: 6,400

Commentary

ACGL operates in the insurance, reinsurance, and mortgage insurance business. I got interested when ACGL came up in my StocksGuide screen because I’m looking to expose myself to the insurance industry with the possibility of interest rates staying higher for a bit longer than some may expect due to the unrestrained spending that we are seeing.

Perhaps I’m a little late in seeing this trend as ACGL has risen 26% over the last year, but I don’t believe this trend is anywhere near from being over and neither does Warren Buffett who invested in Chubb Limited (CB) - another stock in this industry.

Looking at the fundamentals of ACGL, I noted that gross premiums increased 26% YoY (an increase of $5.6 billion) which is an incredible result compared to competitions like CB. Further, ACGL are key players in the reinsurance business where they have a combined ratio of 82.8% compared to the likes of RNR (94.9%) and EG (95.9%). Note that the lower the combined ratio the better.

If ACGL can gain some momentum in their insurance and mortgage business, then ACGL is definitely a great stock to buy but there’s no guarantee there at all. In fact, estimates are expecting a decline in EPS down to $8.57 next year, down from $9.04 today. I’m not sure exactly where I see this because of the weakness in mortgage.

Further, for me the macro conditions correlate so highly to the success of ACGL and despite my bias being towards higher interest rates, I have to consider that I may be completely wrong here. I’m no macro specialist and this would be more of a guessing game for me.

I definitely want to still keep the insurance sector in mind and I think ACGL is a solid company to consider here, but they are trading near 52-week highs and it’s tough to argue that they’re a cheap stock now. Very strong company and I enjoyed doing my research on them, but I’m not going to invest just yet.

Graphic

Here’s a nice graphic showing the correlation between the EV/Sales and EV/EBITDA multiples and the revenue growth for ACGL.

That’s it for the day

I hope you loved this article. As I continue to develop on here, I’m sure there will be some changes to my structure and style, so please do leave some feedback for me.

Please subscribe to my newsletter where I provide investors with all the tools to outperform the market, and retire well before you’re 65. You can also follow me on X.

Disclaimer

Disclaimer: The Accuracy of Information and Investment Opinion

The content provided on this page by the publisher is not guaranteed to be accurate or comprehensive. All opinions and statements expressed herein are solely those of the author.

Publisher's Role and Limitations

Make Money, Make Time serves as a publisher of financial information and does not function as an investment advisor. Personalized or tailored investment advice is not offered. The information presented on this website does not cater to individual recipient needs.

Not Investment Advice

To add further context for the $HAFN ticker. This is how I see the issue. It’s binary on the technicals right now. I have drawn 2 scenarios that the market may be offering, currently. There appear to be 2 possible channel scenarios. One leads to higher highs the other to lower lows. I have drawn in and highlighted them on my chart idea. These are levels to be very aware of. Either way, if this stock continues bullishly it will be encountering key levels of resistance very soon. Buying these plays that are fresh of all-time lows can always be tricky. Getting involved with firms with low level trading data, equally so. Retail punters can get badly burnt if they go the wrong way. Notice the possible formation of the right shoulder of the head & shoulders pattern close to resistance and the 200 ema on the 4-hour chart, coincidence? https://www.tradingview.com/x/ZcMnBLxt/

I agree with you that this needs a correction, ideally a major one. $LTNH This stock is fresh off a July all-time high, IMO there are bearish patterns forming, possibly signalling a correction or pullback. Honestly, this stock has been enjoying a wild ride of late and no one enjoys getting to the party late, do they? Unless you're a unicorn like $PLTR or $NVDA going long at all-time highs is not advisable. I need to see value for a buy. This stock could carry on going up but everything is screaming pullback. https://www.tradingview.com/x/a89w4Irp/