5 Charts For The Week

11/08/2025

Hi all 👋

Continuing my new series which gets released every Sunday/Monday before market open where I look at some potential adds/trims/buys/sells for the week.

The first 3 will be open to all and the last 2 will be for paid subscribers.

1. Eos Energy Enterprises | EOSE

EOSE is a development-scale company in the battery niche with zinc chemistry, which has huge market potential. The company’s tech directly addresses grid reliability challenges, enabling wind and solar to meet demand peaks for effectively. Wins this year include a 216 MWh order from Springfield, a 400MWh contract for Marine Camp, and a DOE loan of just over $300M.

Even if EOSE capture just 5% of the available market, we’d seen major expansion opportunity. This growth likely with come from partnerships with AI-driven data center operators in need for quick, and clean power. I see EOSE being very well placed to become a dominant LDES provides, and they’re a nice US based bet on the energy transition and grid modernization trend if execution remains strong for them.

Technically, I wouldn’t be buying in just yet. We’ve hit this resistance level 3 times in the past 8 months and each time we’ve rejected it. A safer place to buy would be to wait for this $5.00 region in line with a good support and the 100MA.

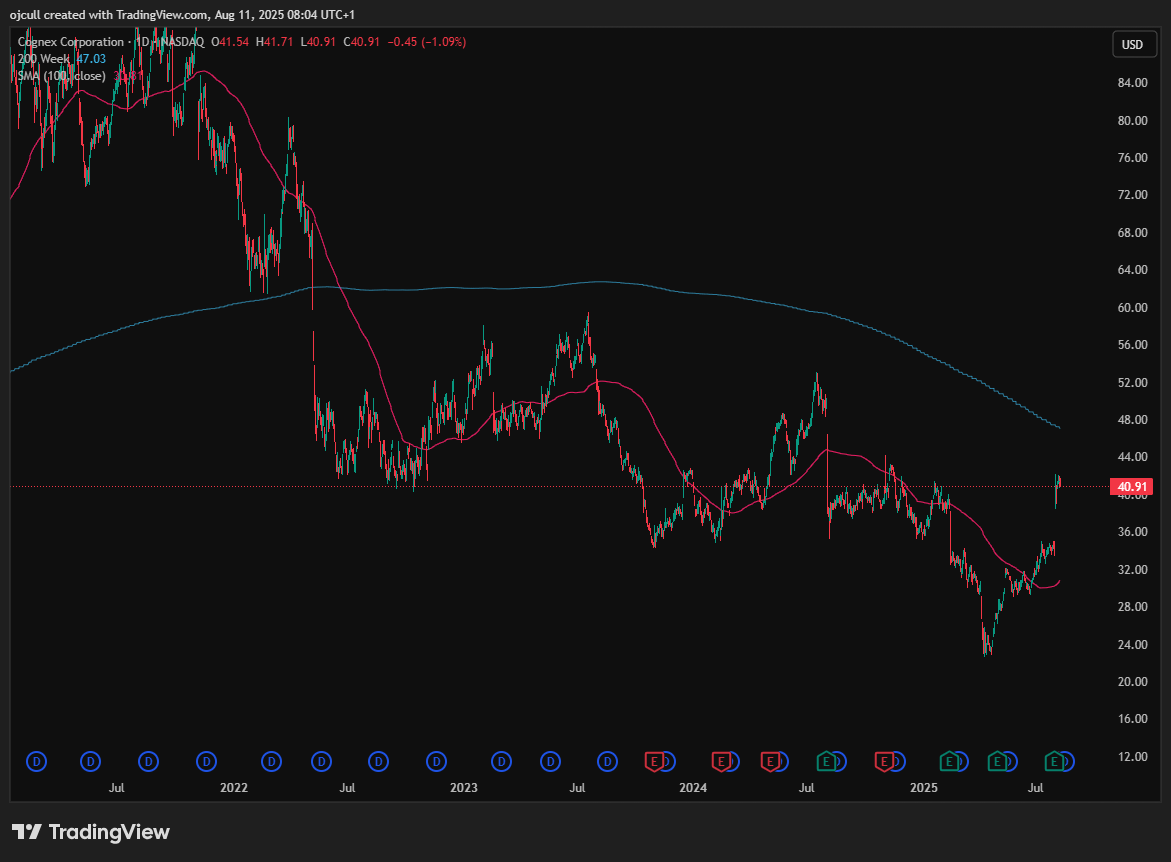

2. Cognex Corporation | CGNX

CGNX is a company I have recently started studying more as a bet on:

Growth of industrial robotics

Growth of automated logistics

CGNX is effectively a leveraged play on the accelerating adoption of robotics and industrial automation. Its machine vision cameras, sensors, and software enable robots to locate, identify, and inspect objects in real time - which is required for precision manufacturing and high-speed logistics.

Half of CGNX’s revenue comes from automation in industries like electronics, automotive, and pharmaceuticals, whilst the other half is driven by booming demand in e-commerce and warehouse scanning.

I haven’t taken this one too seriously yet because I don’t think the valuation is that attractive when you look at a 37x EBITDA multiple for 10% EBITDA growth. However, many companies in this space are valued at a premium and rightly so and therefore it’s weighing up the risk/reward of this one over a 5 year time span. It’ll definitely be a watchlist position and one to watch.

They’re also sitting at a very interesting technical level with this resistance zone that has been in play since 2022. I’m going to see if they can turn this zone into a support and perhaps bounce from there. All in all, I think this one is definitely worth watching but not a buy right now.

3. Upstart | UPST

A portfolio position that recently reported earnings and crushed it, yet dropped over 10%.

UPST are now trading back in the $60s just above this zone (bottom blue line) which is where I added last week as paid subs will know.

If UPST drops below here into the $55 range, UPST will become a very big position in my portfolio.