5 "Fallen Angels" That Could Be Worth The Investment

Hi fellow investors 👋

This is a short article with 5 stocks (3 of which are very high growth) that have had weak stock performance over the last year and therefore offering some nice potential opportunities.

Just as a heads up, I have a deep dive on Lemonade (LMND) coming out soon. The majority of it will be for free subscribers, but the opportunities and risks section will be for paid subscribers. I charge just $14 a month for my paid service which includes deep research that takes me hours (if not days…). If you could spare this cost, and were interested in my work, please do consider becoming a paid subscriber.

Let’s get into the article👇

1. Advanced Micro Devices | AMD

Introduction

AMD has been in the NVDA shadow for the last couple of years. They operate in the semiconductor business but their focus is more on the slightly cheaper CPU market which has benefits for the upcoming inference boom. In such a bullish period for semiconductors, AMD has dropped 43% over the past year signaling struggles in competing against a once in a lifetime company like NVDA.

Numbers

Revenue growth: 24.2%

EV/Sales: 5.0x

Net income margin: 6.3%

Investment Thesis

Training AI models is very compute intensive and relies on thousands of GPUs. This is where NVDA dominates the market. However, inference is where the model is used and where less compute power is required meaning more CPUs should be used. This is where AMD can better compete with NVDA due to their chiplet architecture that allows for both CPUs and GPUs to be on the same chip.

META runs their latest model entirely on AMD chips and said that their inference success was purely down to AMD.

The valuation is starting to look very attractive below $100. If AMD can grow revenues at a CAGR of 15% for the next 10 years (considering data center revenue is 69% I think this is feasible), then we have potentially $104 billion in revenue. At a net income margin of 25% (NVDA has 56%), we have $26 billion in net income which would be a $650 billion company at a 25x PE. This is a 4x opportunity from today.

2. Enphase Energy | ENPH

Introduction

ENPH has been crushed, as with all other solar companies over the last 3 years dropping 66%. It’s been on my watchlist for the last few months but it’s not in my portfolio currently as I want to see some sign of a reverse around solar that we aren’t getting at the moment.

Numbers

Revenue growth: 26.5%

EV/Sales: 4.7x

Net income margin: 16.2%

Investment Thesis

There’s a current industry wide downturn in the solar market, but ENPH have a nice balance sheet set to withstand this downturn. FCF is still enough (despite a slow down) to pay off all long term debt for the next 3 years. The fundamentals aren’t obviously perfect for ENPH at the moment but if you compare them to other solar names, they’re doing well.

Trump’s policy changes aren’t good for ENPH, hence the recent downturn but that will all be priced in soon and I think the global push for green energy will eventually prevail and ENPH will be one of the key beneficiaries of this.

I think there is some more downside coming with ENPH, but anything below $50 has to start to look very attractive over a 3-5 year time frame.

3. ICON PLC | ICLR

Introduction

ICLR is a Clinical Research Organization (CRO) providing outsourced services to pharma, biotech, medical device, and government organization to get new drugs and therapies through FDA approval.

Numbers

Revenue growth: -1.2%

EV/Sales: 2.2x

Net income margin: 12.7%

Investment Thesis

ICON, though relatively unknown by the masses has a huge market share in Clinical Research Organization contributing to 60% of FDA approved drugs over the last year.

They now trade at a 1.6x P/B value. Compare this to Medpace (MEDP) and IQVIA (IQV) which have P/B multiples of 12.1x and 5.5x respectively and you’ve got a good opportunity with ICLR.

Drug development is becoming ever more complex meaning reliance on CROs is increasing YoY creating a nice opportunity for a market leader like ICLR.

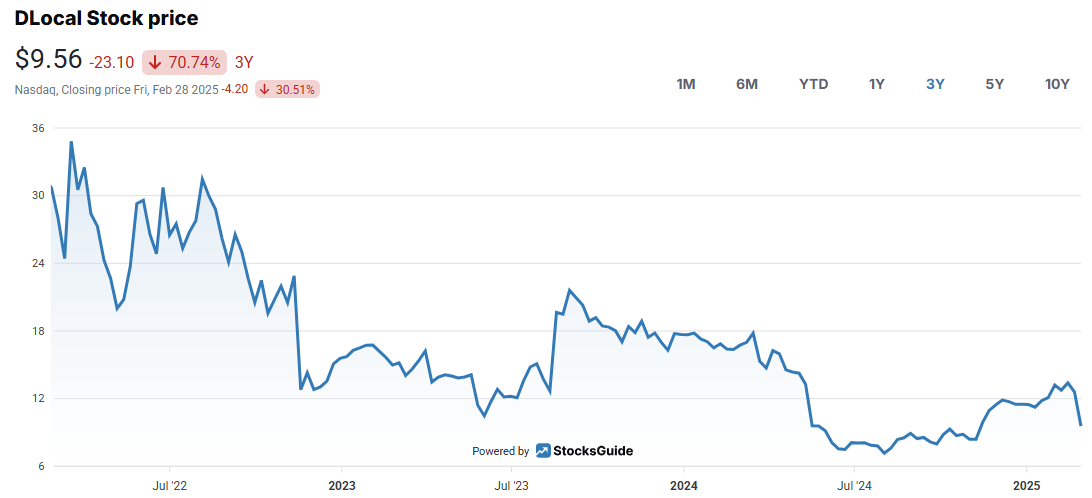

4. DLocal | DLO (portfolio company)

Introduction

DLO is a portfolio company of mine that hasn’t performed that well currently making it one of the worst performers along with CELH, however, I’m still bullish on this emerging market fintech name.

Numbers

Revenue growth: 8.8%

EV/Sales: 2.3x

Net income margin: 14.5%

Investment Thesis

There’s not many quality fintech companies out there that focus solely on the emerging landscape market meaning DLO has a nice competitive advantage in their unique knowledge of the difficult emerging market landscape. This is why merchants rely on the likes of Stripe and Adyen for their operations in developed markets, and DLO in emerging markets where the costs of compliance and research are not worth it to do it in house.

The macro tailwinds behind long term growth are increased digitalization in emerging markets. This has led to projections upwards of $65T in cross border payments by 2030 of which DLO is positioned to take a nice share of this.

The volatility over the last 18 months is stabilizing with nice take rates, more diversification, and reaccelerating TPV. I still believe DLO is a nice play over the next 5 years.

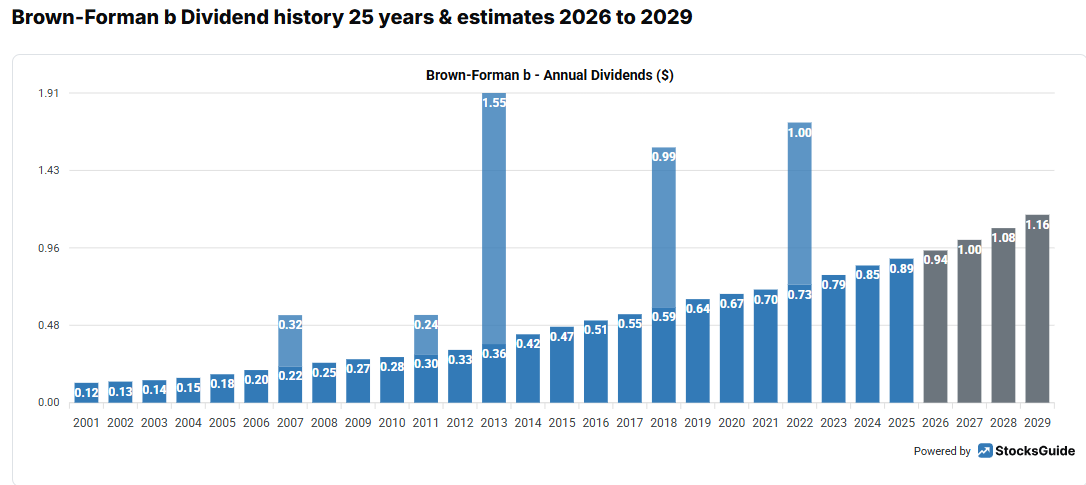

5. Brown Forman | BFB

Introduction

BFB is one of the largest spirit and wine companies worldwide competing with Diageo and Pernod Ricard. They own major brands like Jack Daniels, Old Forester, Chambord etc.

They currently trade at lower levels than 2015.

Numbers

Revenue growth: -1.08%

EV/Sales: 4.4x

Net income margin: 23.5%

Investment Thesis

The negative sentiment around companies like BFB has gone too far in my opinion. Most of the risks are worries to investors such as high inventory and increased tariffs. However, BFB (relative to peers) have far more sales coming from their home market so these tariff risks should be less.

I think a wait and see approach is best because the sentiment around BFB and peers is not improving, but the fact that the company trades below 2015 levels is quite interesting. Revenue has increased ~$800 million since 2015, and net income has increased ~400 million, but FCF has decreased.

The other huge positive for some investors is that BFB is a nice dividend stock with consistent dividend increases for the last 39 years.

That’s all for today

I do hope you enjoyed this short article. If there’s any feedback or additional information that you think would be necessary, please do reach out to me and let me know or leave a comment below. LMND deep dive coming soon!

FSLR)

Hi, I was curious about your thoughts on the short report by Hollenden Square. I'm also bullish on the company but given that it is the second major allegation of fraud, do you see any major risk there?