AI Will Enter the Application Era Soon

A Thematic Check In

In a lot - but not all - of the infrastructure buildout, the easy money has been made.

Growth is still very strong, forecasts are still very strong, the economy is in good stead.

But the market front-runs what is actually happening, and I suspect that by 2027/2028 the rate of growth in the hardware buildout will start to cool. When that happens, the risk/reward profiles across some segments of this AI trade will look a lot less attractive than they do today.

Let me be clear before I go further: this is not a bearish take.

I’m probably one of the more optimistic bulls out there. I think capital will continue flowing into this once-in-a-lifetime technological revolution for years to come.

But at some point we have to start asking which niches of that revolution will outperform from here?

The first thing to understand is that the growth slowdown and the valuation re-rating are not on the same clock.

The hardware buildout has years left in it. Nvidia’s Vera Rubin platform only began shipping in volume this quarter, with Rubin Ultra’s 600-kilowatt racks not arriving until 2027.

In absolute terms, that part of the story is still early.

But the price you pay for exposure to it is a different question entirely. Big Tech CapEx is tracking toward roughly $725 billion this year, capital spending as a share of revenue has climbed past 23%… more than double what it was pre-ChatGPT. And credit spreads tied to the buildout are already widening as bondholders start asking who is actually paying for all of this.

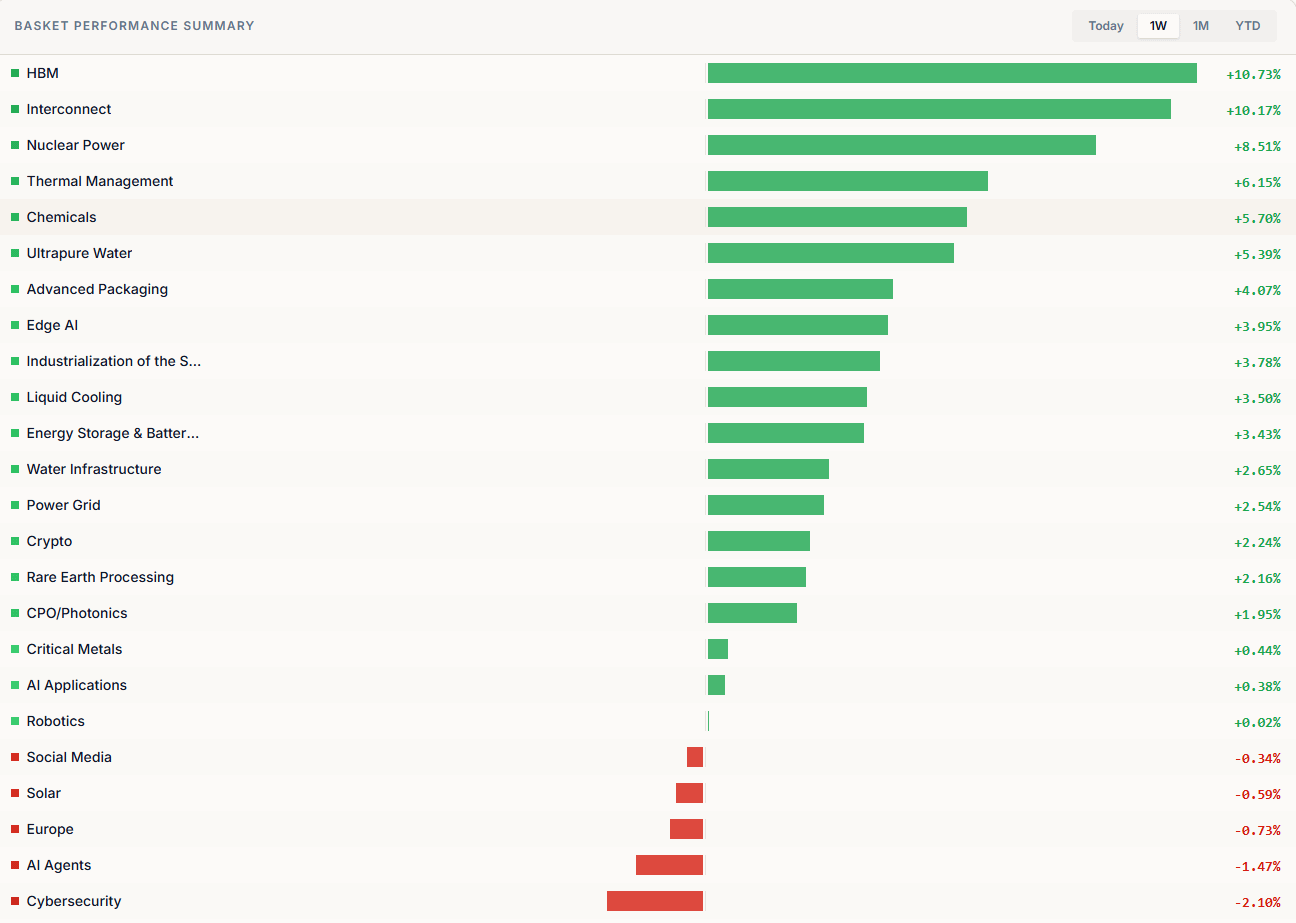

The second thing to understand is that the infrastructure trade has matured from a basket into a stockpicker’s market. For two years, owning the buildout meant owning everything attached to it (chips, power, data centre landlords) and watching them move together. That is largely over.

The bottleneck has migrated from raw compute toward cooling, power, optics and memory, and each time the bottleneck moves it the baton to a different set of winners. Of those, I remain most bullish on optics and memory.

But the broader point is this: the names that carried the basket higher are not necessarily the names that carry it next.

Which brings me to the bigger question.

If these models are this good (and they are) and if agents can now act rather than merely suggest, where does the return on all this CapEx actually show up?

The first phase funded the obvious things: chips, data centres, power. That was the easiest trade to see and the easiest to underwrite.

The next phase is harder to see, which is exactly why it hasn’t been priced yet.

For me, the answer is the application layer - the companies turning extraordinary intelligence into something a customer genuinely needs and depends on, and finds painful to remove.

Before we move on I just want to shout out my paid service for you. I’m building a fully functional web-app / database / research website all in one go. You get:

Daily market commentary

My personal portfolio and watchlist

Weekly thematic commentary

New Ideas

Weekly Videos

All for ease on a nicely designed web-app.

All for just $24 a month (or $240 a year).

The Application Layer

The bull case for the application layer is simple. Once the underlying models are this capable, the constraint stops being “Is this intelligence good enough?” and becomes “Who turns it into something a customer will pay for and depend on?”.

The trigger that turns this from theory into an actual capital flow is enterprise adoption moving from pilot to production.

For the better part of two years, "AI productivity gains" lived all in narrative.

But what's changing now is that that narrative is actually starting to show up in the numbers… in margins, in headcount that stops scaling with revenue.

Agents now can take an open-ended, difficult problem, and work autonomously on their own. Systems now don’t just answer questions but generate hypotheses, run experiments, execute transactions, and do all of this with zero human approval.

The companies that win here the most are within:

The largest industries

The most inefficiently ran industries

Those are:

Insurance

Drug design

Some areas of finance

Materials science

The prize is enormous. But gauging how much some of these sub $10B companies can actually disrupt the market is something I could argue both ways.

However, positioning yourself on the long side of some of these companies I’ll talk about here is right now, in my opinion, probably the best risk to reward set up in the market.

If these companies do end up disrupting these markets…the upside in some cases is enormous.

How to Invest: