Biggest Outflows From US Equities In History - Here's Some European Quality

Hi fellow investors👋

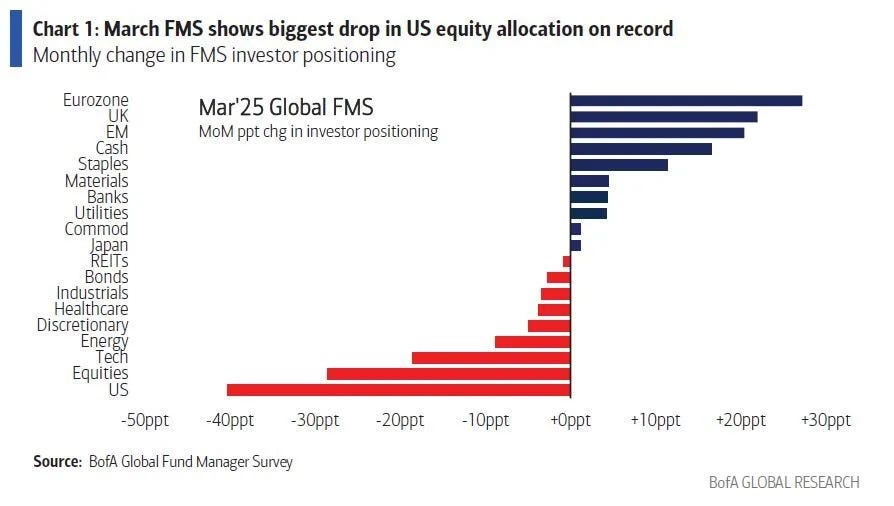

In March, we saw the biggest drop in US equity holdings in history. That’s some big news. Investors are flocking to Europe, UK, emerging markets, and cash…but I’m not.

Here’s what I recommend:

Do not get scared away from the US. 3 months ago was the time to consider decreasing your US exposure, but not today when the market is beginning to drop. FWIW, I do see us going lower, but this is no reason to completely sell out of the US. This is the most important time to DCA (or lump sum if more confident) into high quality names. Do the opposite of the crowds. I’ll be sending out my exact playbook to paid subscribers over the next day.

Also realize that Europe, UK, and emerging markets maybe do offer some value (but not because you’re scared of the US market). I’ve been investing into India, and a couple of stocks in the emerging markets (MELI & NU). This article will show you my 3 favorite European stocks. Disclosure: I am not currently invested in any of these 3 but I think they are great businesses. This is to purely give you some details on some quality stocks in Europe if you were looking to diversify your portfolio there.

1. Nebius | NBIS

Nebius is traded on the NASDAQ but its operations are in Amsterdam and it operates globally. I wouldn’t call it a true European company but I’ve been wanting to express my thoughts on this company for a while and thought now is a good time.

Introduction

NBIS operates a data center in Finland as well as renting data centers in Iceland, France, New Jersey, and Missouri. They provide 2 services:

AI Cloud which is a platform offering GPU clusters for AI training, inference, and data processing. Biggest competitors are the hyperscalers like AWS, Azure, and Google Cloud.

AI Studio which is a platform designed for AI model development and deploying machine learning models.

Investment Thesis

NBIS operate in a market where they are supply constrained. The demand for NBIS is extremely high.

Exposure to the AV market through Avride. Has a large stake in Clickhouse too.

NBIS are in the midst of a heavy investment cycle with $1B in European data centers this year and GPU deployments. With the cash they have on the balance sheet the risks of this big investment period are mitigated.

NVIDIA backed.

Valuation

NBIS core business will have $750M-$1B in ARR by FY26 (and they still have triple digit growth expected in 2026).

The other data centers have another $1-1.5B in potential meaning $2-2.5B in ARR is possible by FY26. At a current EV of just $3.6B, NBIS is trading at just 1.44x FY26 revenue.

More mature data center companies like Equinix trade in the 9x-10x sales range which would give NBIS a $23.75B EV which is 6.5x higher than today. This isn’t incorporating any equity stakes NBIS has like ClickHouse for example.

LMND Valuation

I put this in the Substack chat yesterday but just wanted to make sure you saw it here too. It’s some notes I put together on LMND’s valuation:

It includes:

Peer comparison

Investment model & assumptions

I’ll be only giving this to paid subscribers in the future, but here it is for everyone this time.

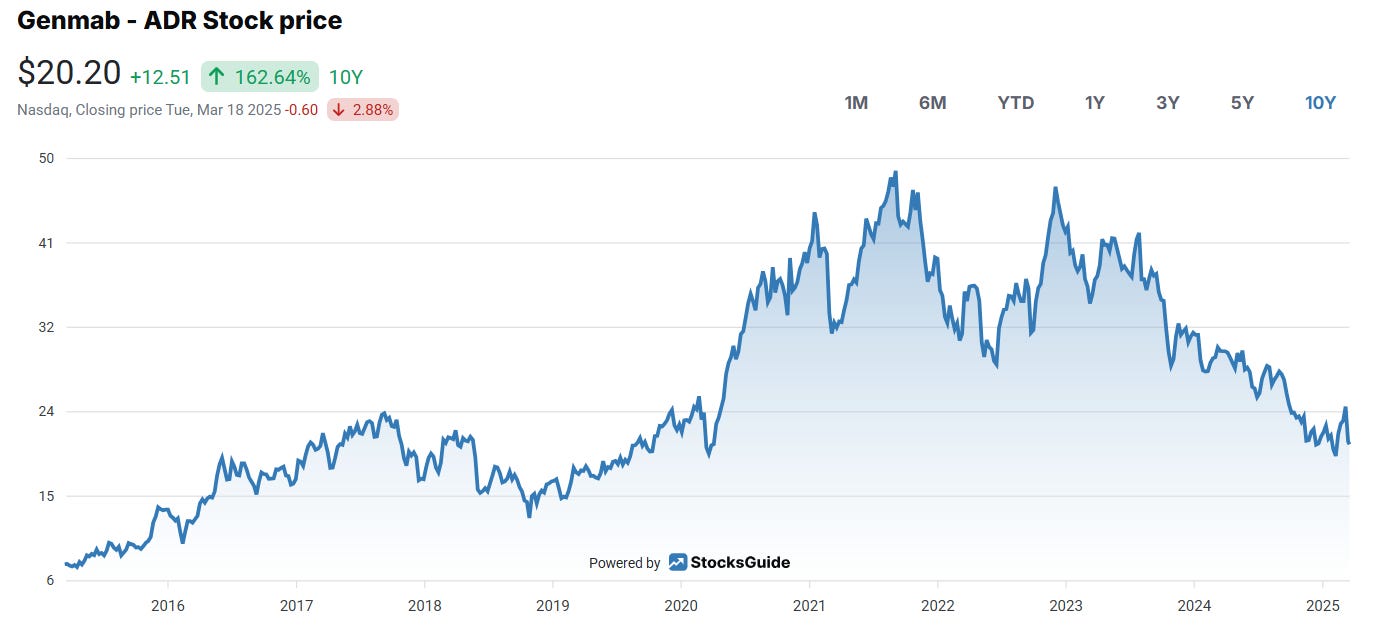

2. Genmab | GMAB

Introduction

GMAB is a leading biotech company based in Copenhagen that develops antibody based products for cancer. They primarily operate a partnership driven model collaborating with large pharma companies like JNJ and Pfizer to co-develop and commercialize drugs. This means they focus more on licensing products in exchange for royalties, and milestone payments.

I don’t love the high risk nature of biotech companies like GMAB to be honest. It’s the main reason I tend to stay away. A lot of the companies success relies on clinical trials of which there’s 3 expected to be completed by FY26. If successful, then GMAB’s sales will likely exceed the $6-7B range. However, my lack of knowledge in this area makes this more akin to gambling in my opinion. The only stock I actually like in this niche is LNTH.

However, I see the benefits of investing in companies like GMAB and to be honest I think they have a bright future from my understanding. But my understanding is admittedly too little for me to own the company.

Investment Thesis

Slowly transitioning away from relying solely on royalty payments to actively co-developing and co-commercializing products.

Out of the biotech companies that I follow, GMAB have a very healthy pipeline with 7 products in phase III trials. Rina-S (ovarian and endometrial cancer treatment) is the most exciting product projected to be an option for 85% of total ovarian cancer patients. Today, effective treatments are available for a much smaller % of the individuals.

Although risky, GMAB have proven they have a very disciplined approach to acquisitions. This is always nice to see for those companies that grow in this manner.

Valuation

Relative to peers like ABBV, GILD, ARGX, ZEAL, MRUS, ADCT, and PHM, GMAB trades lower on a NTM Sales, a NTM EBITDA, and a NTM PE multiple.

For me, because the outlook is a little more unknown for GMAB now they are transitioning slowly away from more predictable royalty payments to co-developing drugs, I think the best way to look at the valuation is relative to peers. Modelling out revenues is very difficult as it’s far too dependent on clinical trials.

Therefore, I think the best way to look at them is relative to peers and currently they’re very discounted trading at 37% of ABBV and 50% of GILD.

3. Wise | WISE

Introduction

I find it quite hard to list multiple great UK tech companies but I think WISE is one of them.

WISE is a disruptive fintech company with some of the best unit economics out there. They specialize in cross-border transfers and generate revenue via low cost FX conversion fees that are saving customers ~2.5% vs traditional banks each time they translate currencies.

Investment Thesis

WISE have incredible unit economics. EBITDA margins expanding from 18% to 36% in 18 months driven by a 45% increase in sales. This shows how they have a largely fixed cost base.

WISE is still founder led and his name is Kristo Kaarmann. He is obsessed with customer experience and currently the vast majority of all profits made are reinvested back into the company. This shows early signs of a great long term compounder.

Currently only 9 million users are on Wise but they’re growing nicely with 20% increase YoY. There’s not many companies out there where huge increases in scale and volume also lead to very positive margin expansion opportunities.

The global remittance market is worth $860 billion and WISE currently only account for 1% of SMB remittances globally.

Valuation

WISE currently trade at 5.3x sales for 23% revenue growth. This makes them slightly more expensive than the likes of NU and SOFI for less revenue growth. I do think WISE is a quality company that has the potential to compound for years, but I wouldn’t invest in them if they’re trading at a higher multiple than other fintechs (with more product variety) like NU and SOFI.

WISE is most definitely a company I’d have on my watchlist though if the time becomes right.

That’s all for today

I do hope you enjoyed this post and it gave you some ideas. If there’s any feedback or additional information that you think would be necessary, please do reach out to me and let me know or leave a comment below.

Next Deep Dive….NU

Good stuff here. Big fan (and customer) of Wise, though i feel its share is pricey right now. And Genmab is on my radar here in the Nordics but hard to feel confident about. Smart post, thanks.