Edge AI: The Stock Basket (All Layers)

AI is leaving the cloud.

The dominant model for AI infrastructure for the last decade or so has been massive data centers, hyperscaler compute, and models too large and power-hungry to run anywhere else but the cloud.

That model is being extended now by a new reality where inference happens at the point of need (the device, the vehicle, the robot etc).

That’s all old news though.

But what’s more important is how to invest in this transition now.

We’ve had lots of names move a lot already.

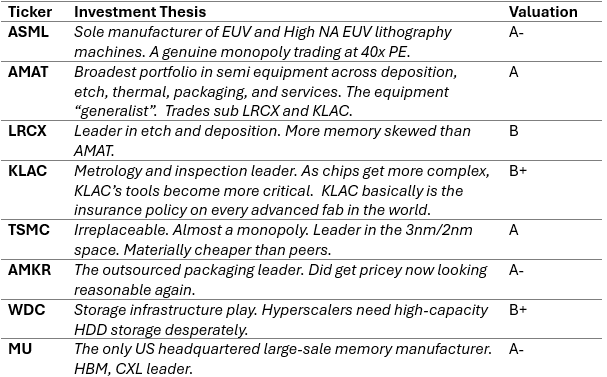

KLAC has moved 150% in the last year.

AMKR has moved 259% in the last year.

MU has moved 704% in the last year.

The question now is where is the value? Are some of these names still valued fairly or is there new names to seek out?

The important thing to understand is that there is always another bottleneck. The bottlenecks just shift around when one bottleneck is solved. I.e. when silicon performance scale, the constraint shifts to memory bandwidth. When that improves, it shifts to advanced packaging…then power conversion efficiency…then thermal dissipation…then materials etc.

Understanding where those constraints are is the challenge and in this brief paper I’m going to outline it for you.

The Edge market is currently valued at $31 billion and set to grow to ~$70 billion in 2031. That’s a CAGR of 17.5% for 5 years. That’s a market we want to be a part of.

Here’s how I have broken down the layers:

Layer 1: The Bedrock (Materials, Mining) - 0 to10 years

Layer 2: The Foundation (Equipment, Packaging, Memory) - 0 to 4 years

Layer 3: The Enablers (Power, Cooling, Connectivity) - 0 to 4 years

Layer 4: The Builders (Systems, Design Infrastructure) - 1 to 5 years

Layer 5: The Perceivers (Sensors) - 1 to 5 years

Layer 6: The Brains (Edge Silicon, Software) - 0 to 4 years

Layer 7: The Frontier (Humanoids) - 3 to 8 years

You’ll note I added a timeframe next to each year. That’s my best estimate on when I think this layer is going to generate the most returns and for how long. You’ll note I start a few of them at 0 years…indicating we’re already in the big move for that layer.

You’ll also note based on the timeframes that Layer 1, Layer 4, and Layer 5 are to me the best places to be invested right now to be ahead of the moves.

Layer 1: The Bedrock (Materials & Mining)

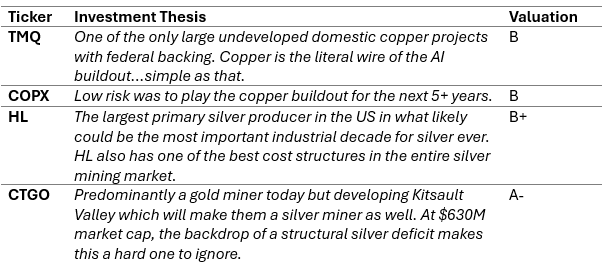

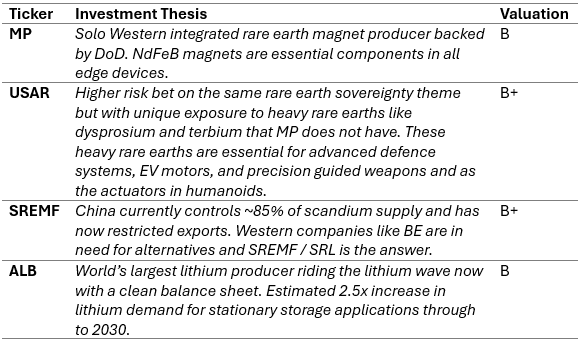

Every technology revolution eventually runs into the physical world. Edge AI is no different. Beneath the silicon, the software, and the systems lies a layer of materials that no amount of engineering ingenuity can replace. Copper for power. Silicon for conductivity. Rare earths for magnets. Silver for connectivity.

The bedrock layer is the most upstream layer and often the most overlooked by tech investors.

But it’s also the most structurally compelling part of the entire investment universe which I am well positioned for.

Core (Copper & Silver)

Rare Earths

Layer 2: The Foundation (Equipment, Packaging, Memory)

This is one of the more concentrated layers in the Edge AI universe. ASML is the sole manufacturer of the extreme UV lithography machines where literally no advanced chip can be made without it.

TSMC’s CoWoS advanced packaging process which is the critical tech for stacking memory onto compute.

And then you have memory production dominated by 3-4 companies.

It makes this layer a key chokepoint controlled by a handful of companies. Every Edge AI device for the next decade passes through the following companies.

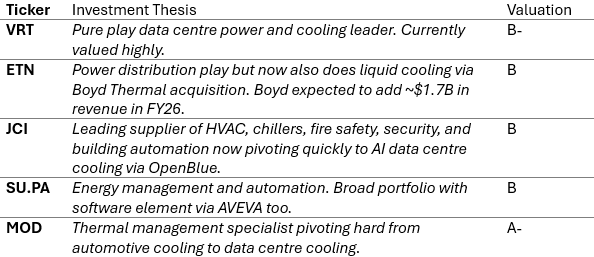

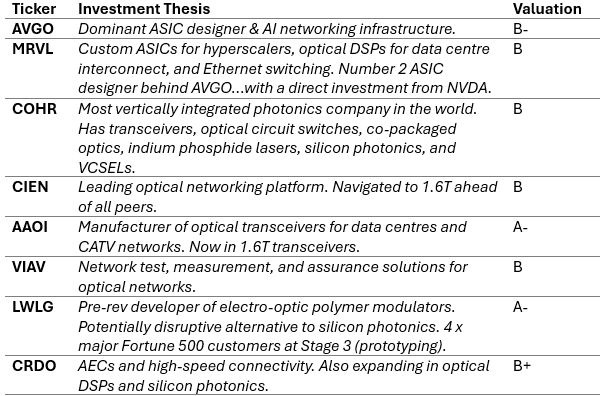

Layer 3: The Enablers (Power, Cooling, Connectivity)

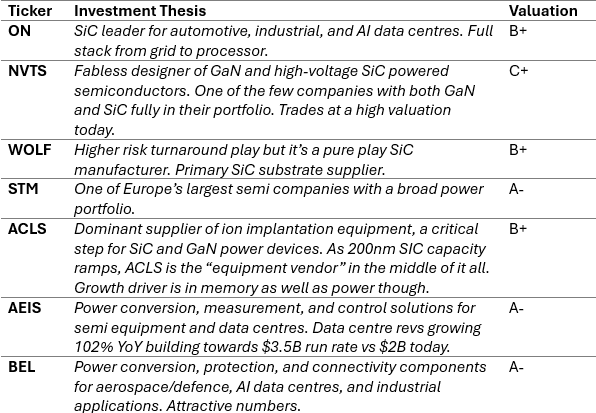

This is the unglamourous, but necessary layer of Edge AI. It’s where incredible technology is met efficiency priorities.

Every additional watt of AI compute that has been generated has to be removed. Power has to be converted. Data has to be transmitted. And it all has to be done as efficiently as possible.

Air cooling is no longer feasibly possible, so liquid cooling is the new norm. Power conversion efficiency becomes a first order cost driver. Optical interconnects are becoming first order cost in deployments.

Power

Thermal Management & Cooling

Networking & Interconnect

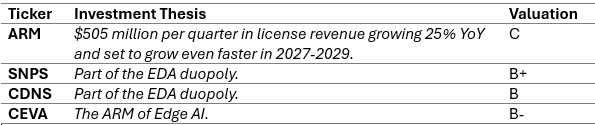

Layer 4: The Builders (Systems, Design Infrastructure)

This is the layer where the physical infrastructure of the Foundation and Enablers is translated into deployable intelligence. It’s the layer of design tools, intellectual property, and system integration that determines how chips get designed, assembled into systems, and how enterprises deploy them.

AI chips are becoming far more complex and harder to design. ARM’s set architecture sits inside virtually every edge device on earth collecting a royalty on each one.

And then the electronic design automation (EDA) software is basically a duopoly with Cadence and Synopsys. EDA market is growing +11% through to 2030. Nothing too exciting but structurally also key to the next few years.

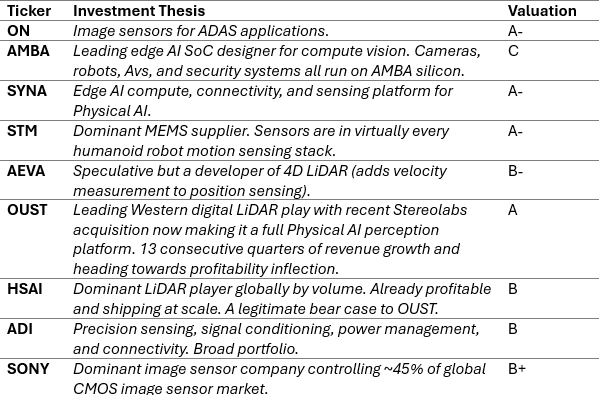

Layer 5: The Perceivers (Sensors)

What makes this layer structurally interesting now is that it’s all about the migration of AI inference onto the sensor. Processing is moving from centralised compute to the point of capture, reducing latency, bandwidth consumption, and power draw.

Historically, sensors were a commodity component but today they’re becoming a compute platform in their own right. That should lead to software like margins.

This layer will lag the silicon buildout. Sensor platforms mature after the compute infrastructure that will process their output is in place. This makes the next 12 months a perfect time to start considering some of the plays in this basket.

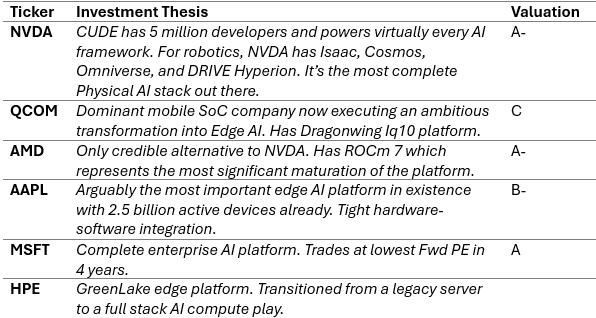

Layer 6: The Brains (Edge Silicon, Software)

This is the layer we all know about…the NVDA’s, QCOM’s, AMD’s. NVDA has Jetson and DRIVE, QCMON has Snapdragon X Elite.

The hardware is almost the old story here. The more interesting part of these plays today is the software. This software determines which silicon gets designed in at the platform level. It’s ultimately the level that will prove far more durable over time.

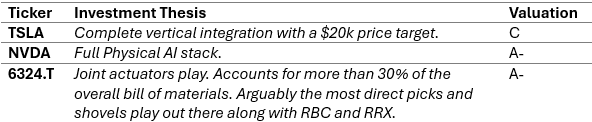

Layer 7: The Frontier (Humanoids)

This is a market projected to be worth ~$40B by 2035. We already have Tesla Optimus entering low scale production with goals to price Optimus at $20k. Figure AI has been valued at $39 billion as of September 2025. Boston Dynamics is in commercial production.

This is where the value will ultimately accrue at the end but we’re still years away and there’s a lot of money to be made in all other layers before we get there.

For packaging what about other international companies like TOWA Corporation (6315.T) , BE Semiconductor Industries N.V. (BESI.AS) and Ibiden Co.,Ltd. (IBIDY)

Killing it. Love the research 🙏

Have you written or plan on writing anything about the impact of AI in healthcare, pharmaceuticals, genomics?