First Solar - Investment Thesis

+45% in 1 month

Hi all 👋

As paid subs will know when I called it out to them a few weeks ago, FSLR is now a small position in my portfolio and it’s already returned +44% in a matter of weeks. It didn’t make a significant change to my overall portfolio because I initiated only quite a small position, but I still am bullish on the name in the long term and am currently looking for a good place to add.

Introduction

FSLR is a vertically integrated, US based, solar tech firm. Most solar companies like CSIQ, JKS, SHLS use crystalline silicon (c-Si) which currently dominates ~90% of the entire solar market and a lot of the manufacturing happens in China. Amongst the trade war and “made in America” push by Trump, this is exactly one of the reasons FSLR has performed well. They are:

Manufactured mostly in America

Use Cadmium Telluride which is more cost effective per watt

~58% of FSLR’s manufacturing footprint is in the US, with 37% in Malaysia & Vietnam, and the rest in India.

Unlike other solar companies which you may know like Enphase or SolarEdge, FSLR does not sell directly to households. Instead, they sell to utility-scale project developers (who build solar farms), and independent power producers (those who operate solar power plants). This makes the FSLR revenue slightly higher volume, and less cyclical as opposed to selling to households.

In this article, I’ll touch on:

Q1 Earnings Report (it was quite complex. I do my best to simplify it)

Opportunities ahead for FSLR

Valuation - is it worth buying today?

Q1 Earnings

Now this is complex. Writing this earnings review and investment thesis, a lot of which has been based on the Q1 earnings call wasn’t an easy task but a huge chunk of the call was awfully complex. This is no disrespect to the management team, but it paints a picture of just how complex the macro solar environment is today with the trade war and 45X tax credits.

On first glance, the Q1 earnings report was not great. We had a missed revenue estimate of $844.57M, down from Q4 2024 which was $1.51B and also down from Q3 which was $887.6M. These numbers alone show you the complexity and uncertainty of the macro solar environment.

Combining this with a significant guidance reduction in FY25 revenue and EPS (guidance was cut 10% and 18% respectively looking at midpoints), and you’ve got quite a bleak picture, hence why the stock finished 9% down post earnings. However, as investors took time to understand the numbers which I’ll try summarize here, you’ve actually got quite a nice looking opportunity ahead.

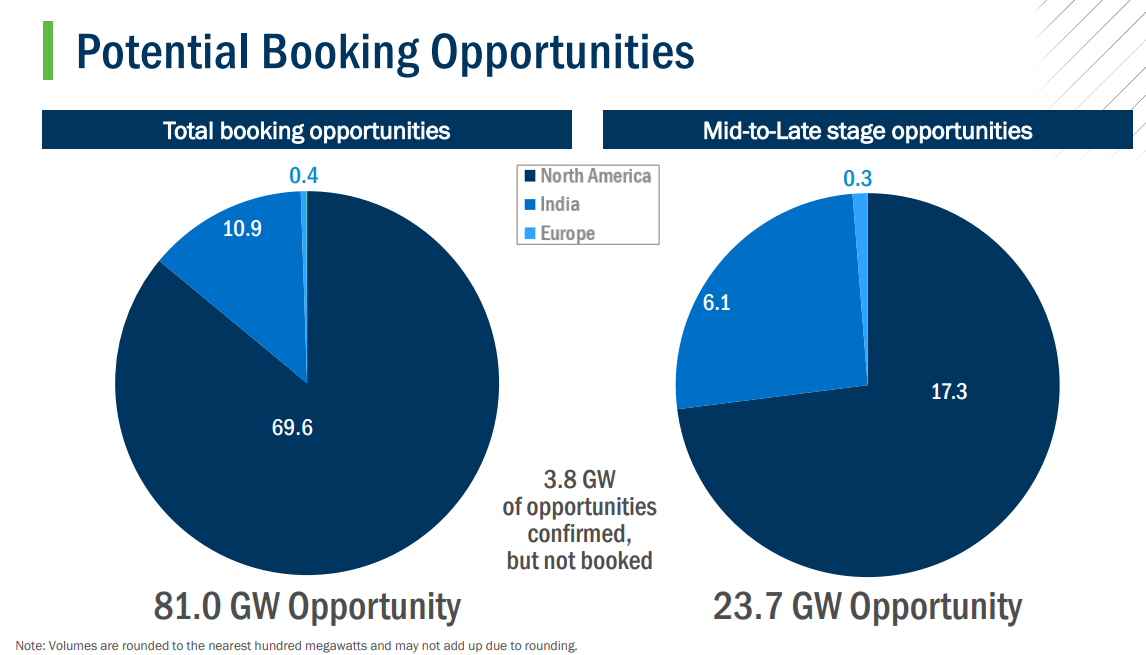

Essentially what we’ve got at FSLR is a situation where the contracted backlog is strong (66.1 gigawatts which gives a value of ~$19.8B). Obviously these contracts are multi-year spread out typically through to at least 2028 so it gives some nice revenue visibility ahead.

However, the issue at the moment with FSLR is that these contracted backlogs aren’t as certain as they have been in previous quarters because of the trade wars. These trades wars can be a net benefit to FSLR over the long term, especially relative to peers, however, the uncertainty at the moment creates a ton of volatility namely because of the manufacturing centers in India, Malaysia, and Vietnam which have been hit with reciprocal tariffs of 26%, 24%, and 46% respectively. Here’s what can happen:

A material hit to gross margin happens on all goods sent for sale in the US.

The module buyer absorbs all of the costs of the extra tariffs.

FSLR and the module buyer both absorb the extra costs.

FSLR can choose to terminate the contract.

The question then becomes how much of the current backlog is at risk of the above happening. Of the current 66.1 gigawatt backlog, 13.9 gigawatts are set to be manufactured internationally but contracted to be delivered in the US marking quite a substantial risk to revenue going forward. In an ideal world, FSLR would lean more into their domestic production but this is no quick fix. There are however domestic expansion plans with the Louisiana and Alabama facilities which will begin commercial operation in 2H 25 and ramp up in 2026.

The above complexities show why guidance in Q1 was restated lower.

Ultimately, from an investor point of view and without diving too much into the short term noise, there’s a couple of ways to think about FSLR’s current performance.

Guidance was cut but it doesn’t matter: The reason for the uncertainty is purely a macro wide uncertainty that should eventually be a net positive to FSLR. There’s no signs or data to show that FSLR is being disrupted, or losing market share to competition. It’s purely a macro driven event, hence why we’ve seen FSLR move +20% post earnings (as investors realized FSLR was not in danger) and -10% this week (on announcement of the 45X tax credit removal in 2028).

Guidance was cut but it does matter: FSLR is a solar tech company with struggling profitability, especially post ex-45X which should total in the region of $1.7B. With operating income in FY25 in the $1.7B range, you then realize how material these 45X tax credits are. FWIW, as someone who has initiated a small position in FSLR, I am less in this camp though it’s a fair argument.

My take on earnings:

Currently, the narrative around FSLR matters much less about EPS growth, revenue growth, and alike, and more on the trade war narrative. That is exactly what is going to move the stock price over the next 12-18 months and that is ultimately what is going to position FSLR as a winner or loser in the coming years in the US solar market.

The general narrative is that FSLR will be fine because the US solar market is growing, and FSLR have a worst case scenario where they lose a big portion of their non-US manufacturing facility (perhaps even write it down to nil), but they have a product that will be strong domestically. The only issue domestically will be some margin hit with a direct impact because of raw material (aluminum mainly) cost increases. Despite being material, FSLR estimate these costs to only be ~6% of operating income guidance for FY25. Relative to tariff expectations, a 6% hit isn’t too bad, especially considering that this could be a worst case scenario.

This tariff war essentially prevents any significant competition in the US from being a threat so a 6% hit to operating income can’t be deemed too bad. The reason there’s no competition anywhere near FSLR in the US market is because the vertically integrated supply chain that FSLR has been building since the 2000s. There’s no company today that can replicate the supply chain, scalability, or capacity of FSLR anytime soon. Therefore, looking at this from a net position, I think FSLR will do well long term.

Although we may see some short term hits to the numbers, to me FSLR looks like a tariff winner long term and if investors want exposure to the solar market (highly recommend), then I think FSLR is perhaps the best play in the market to do that right now.

Opportunities

Solar Industry

One way I like to look at FSLR is a second-beneficiary of the AI trend. We’ve got the NVDA’s, the NBIS’s, and the hyperscalers, we’ve got the new AI trend (the LMND’s, the HIMS’s, the fintechs etc) and now we’ve got those companies that will benefit massively from the surge in data centers, the surge in compute power required, and the pressure to meet clean energy goals. Some of the above companies (NVDA’s, NBIS, etc) have been given some nice multiples, and there’s some (LMND’s, FSLR’s) which have yet to fully convince investors that they are also ready to ride the AI wave.

For the last few years, solar has been the fastest growing renewable energy source by quite some distance. Although the likes of wind, fission, fusion, geothermal, and gas carbon capture can work, the huge bulk of this 165% increase in power demand (just from data centers) by 2030 is set to come from solar. The reason being:

Solar is far cheaper than alternatives (in most regions).

Solar build out is far quicker than alternatives like nuclear, hydro, or wind which can take 4-5 years as opposed to 1-2 years for solar. The AI wave is happening fast and hyperscalers can’t afford these slow build outs.

The hyperscalers like GOOG, AMZN, META etc all are under intense ESG pressure for 100% renewable energy use.

Solar is the most scalable renewable energy source.

To me, it’s quite clear that the solar build out is only really just getting started. There’s going to be a lot of volatility along the way no doubt about that, but I wanted some exposure to the solar market and I think FSLR is the best company to do that.

Elon and Google CEO Sunar Pichai sure agree 👇

International Market

The international market isn’t considered too much of an opportunity for FSLR as most of the bull case is focused around domestic US production. However, FSLR’s cadmium telluride panels perform much better in hot and humid conditions relative to the traditional silicon panels. Some target areas for FSLR therefore are the likes of India (where FSLR have production capacity), LatAm, and potentially Middle East later down the road.

With current capacity in India mostly originally being forecast to be sold into the US market, the current revisions to this post tariff changes now mean that at least 50% of this capacity is now being sold domestically into the Indian market. India is a huge opportunity for FSLR, though the competition is fierce. However:

The humidity in India makes FSLR’s Cadmium Telluride better

India also have a “Made in India” approach and FSLR have production capacity in India

So the oportunity is there, but you’ve also got the bigger players like Adani Solar, and Tata Power Solar who can undercut FSLR on price which is key in arguably one of the most price sensitive markets globally. Nevertheless, FSLR are looking to expand their capacity domestically in India so there’s an opportunity for FSLR to increase Indian revenues from 4.7% of the total revenue to materially higher.

Tariffs

I spoke a lot about this in the Q1 earnings review section above so I won’t repeat myself.

Technology

From a technology point of view, I’ve briefly mentioned that FSLR use Cadmium Telluride (CdTe) whilst most peers use crystalline silicon. Most simply, crystalline silicon is slightly more efficient than CdTe (~2-3% more efficient), however, this changes when you put the panels in much warmer, and high humidity areas because of their temperature coefficient characteristics.

The other important characteristic to note about FSLR’s CdTe is that manufacturing and installation costs are far cheaper than alternatives so even if efficiency is slightly less, the long term economic return from CdTe tends to be higher than the traditional silicon counterparts. Not only that, but in large scale utility projects the useful life of CdTe panels is longer. They’re much more PID resistant and considerably less prone to microcracks, or other forms of physical degradation over time.

That’s a quick snapshot of the FSLR tech vs crystalline silicon, but currently the wider market massively favors crystalline silicon with ~90.9% market share in the global PV market vs just 6% for CdTe.

However, growth rates for these markets are very dissimilar with a 15% CAGR forecast for CdTe through to 2033 and just 4.4% CAGR for crystalline silicon through to 2033. FWIW, FSLR makes up nearly 100% of the CdTe market so this growth rate should be completely feasible for FSLR if they merely just meet the market forecasts.

Valuation

Now the reason why FSLR is a 2x opportunity. I first bought at $138 (as paid subs will know), so for me to reach 100% on my position I’d like to see FSLR hit $276 which would put them just below all time highs ~$299.

FSLR revenue growth is inconsistent, with some quarters in the 48% range and some in the low single digits range, but if you average them out over a 3 year time frame, taking into account the tailwinds above, then I think it’s completely reasonable to assume that FSLR averages a growth rate of 15% CAGR with EBITDA margins in the range of 45%. That would give FSLR a projected EBITDA of $3.195B which is just below analyst estimates for FY2027.

Looking at peers, you’ve currently got:

Jinko Solar (JKS) trading for 5.1x EV/EBITDA (module manufacturer like FSLR)

Canadian Solar (CSIQ) trading for 6.9x EV/EBITDA (module manufacturer like FSLR)

Enphase Energy (ENPH) trading for 15.8x EV/EBITDA

Complete Solaria (SPWR) trading for 37.9x EV/EBITDA

Shoals Technologies (SHLS) trading for 8.0x EV/EBITDA

This puts FSLR at 7.5x EV/EBITDA right in the middle of the pack, yet they differentiate themselves by having almost a complete monopoly in the CdTe space which is growing far quicker than any other solar niche.

Based on my conservative assumptions (below analyst estimates), you’ve got a company set to grow EBITDA at a 20% CAGR for 3 years which should give an EV/EBITDA multiple in the range of 10x, especially with FSLR’s niche potential. So at $3.195B in EBITDA and a 10x multiple, you’ve got an EV of $31.95B which is a 80% increase in value (from todays value) over 3 years using very conservative growth rates and a multiple still below peers like ENPH, which should in turn give me at least a 100% increase.

That’s all for today

I do hope you enjoyed this mini look into FSLR. If there’s any feedback or additional information that you think would be necessary, please do reach out to me and let me know or leave a comment below.

My favorite company atm.

Really solid breakdown — appreciate the nuance you brought into the Q1 call, especially on the trade war impact. I’m in a similar boat with a small FSLR position and debating whether to size up. Curious though, with the India/Vietnam/Malaysia tariffs creating near-term headwinds, how confident are you that the Louisiana/Alabama facilities can ramp fast enough to offset the risk before 2026?