Grid Upgrade: All the Bottlenecks You Need to Know

The Full Ecosystem

Everyone is talking about the grid…and for the right reasons.

But if there’s one lesson we’ve all learnt from the optics megatheme, it’s that huge money can be found by looking where nobody else is.

That’s why I’m writing this piece. I’m bullish on the plays a lot of us know about (ETN, HUBB etc), but there’s far more ways to play this theme than owning these stocks which now trade at PE multiples +30x.

The power grid upgrade isn’t an AI trade, nor a clean energy trade. It’s something far more fundamental. We’re on the verge of major economic growth, technological leadership, and energy transition…but every single one of these run through wires.

Not least old, overloaded, and massively underfunded wires.

BNEF’s latest grid outlook showed that globally grid CapEx has now topped $470B in 2025 and that rate of CapEx growth is still growing in the double digits. Capital is flowing into hardware, software, advanced power-flow control systems, and grid-enhancing technologies simultaneously. This is not just a cyclical spending spree…it’s the beginning of what forecasts are predicting as a $1.4 trillion infrastructure super-cycle running to 2030.

Here’s the part you need to understand though. You can’t simply just modernize a grid. You can’t train a transmission line crew in a few months. You can’t get HVDC cables delivered in under two years. You can’t manufacture a large power transformer to order and receive it before 2027.

The supply chain that builds and upgrades this infrastructure has some real constraints… in materials, in manufacturing capacity, in labour, in regulations that can’t be resolved by just increasing CapEx. This pressure is what makes the grid infrastructure buildout one of the most non-discretionary investment themes in the global economy today.

Before we get into this article, I want to mention my database that I am building for paid subscribers.

For the last 1-2 years I have shared a Google Spreadsheet. You can see the latest one here:

This document gives you access to:

My portfolio

My watchlist

My theme tracker

All of the stocks per theme I follow ranked by growth vs multiples (250+ stocks tracked amongst the one exciting themes).

What’s even better is that this document is becoming a web app.

Over the next few weeks I’ll be sharing sneak peeks as we enter beta testing with a group of paid subscribers helping shape the product into exactly what this community needs. This is being built with you, not for you.

Because what I’m building goes well beyond stock picks and data dumps. I’m building a platform where subscribers have access to all the research, all the data, and all the commentary they need — in one place, updated in real time. And I do it fully transparently. My exact portfolio is shared so you always know precisely where my own money is going as well.

If that sounds like something you want access to, the link is below.

Contents:

Why this is a decade-long structural theme

Bottleneck 1: The Transformer

Solid-State Transformers

Bottleneck 2: Grain Oriented Electrical Steel(GOES)

Bottleneck 3: Switchgears & Breakers

Bottleneck 4: High Voltage Cables

Bottleneck 5: Interconnection

Bottleneck 6: Transmission Line Construction

Bottleneck 7: Towers, Poles, & Structural Hardware

Bottleneck 8: Grid Resilience

Everyone is talking about the grid. But almost nobody is talking about it correctly.

A proper thesis requires understanding why the money flows, where it gets stuck, and which second and third-order beneficiaries capture the value that the first-order trades have already priced in.

This piece does that. We’re going to walk the entire grid upgrade chain from raw material to software layer, identify every genuine bottleneck, price those constraints, and give you the full investable universe for each one (which you’ll then see on my database/web-app). I mention every relevant public stock, and then offer my highest conviction name/names within each section.

Why This Is a Decade-Long Structural Theme

U.S. electricity demand is doing something it hasn’t done since the 1970s: it’s growing meaningfully.

For two decades, from 2000 to 2020, overall electricity consumption in the U.S. actually declined slightly as efficiency gains offset population growth. That era is over.

AI data centers, manufacturing reshoring, EV fleets, and the electrification of homes and industrial processes have reversed the trend sharply. Analysts now project the US will need more than 150 gigawatts of additional capacity by 2030. To put that in context, the entire existing U.S. power fleet is roughly 1,200 GW — so we need to add the equivalent of ~12% of the entire grid in 5 years.

The grid itself — the wires, poles, substations, transformers, switches, and software that move electrons from generation to consumption — was largely built in the 1950s through 1970s. More than half of U.S. distribution transformers are beyond their expected service lives. Many transmission lines are 40-50 years old. The system was designed for a one-directional flow of power from central plants outward. Now we’re asking it to handle bidirectional flows from millions of rooftop solar installations, intermittent wind, distributed storage, and the concentrated power demands of 50MW data center campuses.

Global grid capital spending crossed $470 billion for the first time in 2025, up 16% year-on-year. U.S. utility capex hit $202 billion in 2025, up 8% from the prior year which itself was up 12.6%. This isn’t a one-year event. It is the beginning of what many analysts are calling a $1.4 trillion utility infrastructure super-cycle from 2025 to 2030.

The constraint is not capital. Capital is flowing well.

The constraint is physical: you cannot build the grid faster than the materials and workers that go into it.

The Eight Bottlenecks

Bottleneck 1: The Transformer

Electricity is generated at power plants at quite low voltages…10,000 to 30,000 volts. But the transmission of electricity at these voltages is inefficient today. Basic physics…the longer the wire, the more resistance, the more energy is lost as heat.

To move electricity economically across hundreds of miles of wires you therefore need to increase the voltage to +200,000 volts. This is what a transformer does. It steps voltage up before transmission and steps it back down before it reaches its end destination.

Pretty much all electricity generated in the US passes through at least 1-2 transformers before it is used.

How are transformers made?

Most transformers are made from a highly specialised steel alloy. It’s called grain-oriented electrical steel (GOES) - that’s the core part of a transformer.

You’ve also got:

The windings made from copper.

The insulation

Here’s some basic stats to evidence this bottleneck:

Power transformer demand has surged 119% since 2019 whilst distribution transformer demand is up 40%.

Wood Mackenzie estimate 30% supply shortfall for power transformer and 10% shortfall for distribution transformers.

Power transformers now have a 2.5 year (128 week) lead time.

Utilities are paying 4-6 times what transformers cost in 2022.

The global transformer industry carries a 2-3 year manufacturing backlog not expected to ease before 2027.

List of stocks:

Eaton | ETN

GE Vernova | GEV

ABB Ltd | ABBNY

Siemens Energy | SMNEY

Powell Industries | POWL

Hubbell | HUBB

Hammond Power Solutions | HMDPF

Hitachi Energy | HTHIY

SPX Technologies | SPXC: Has transformer components and electrical testing equipment business relevant to the bottleneck.

Legrand | LGRDY

Favorites:

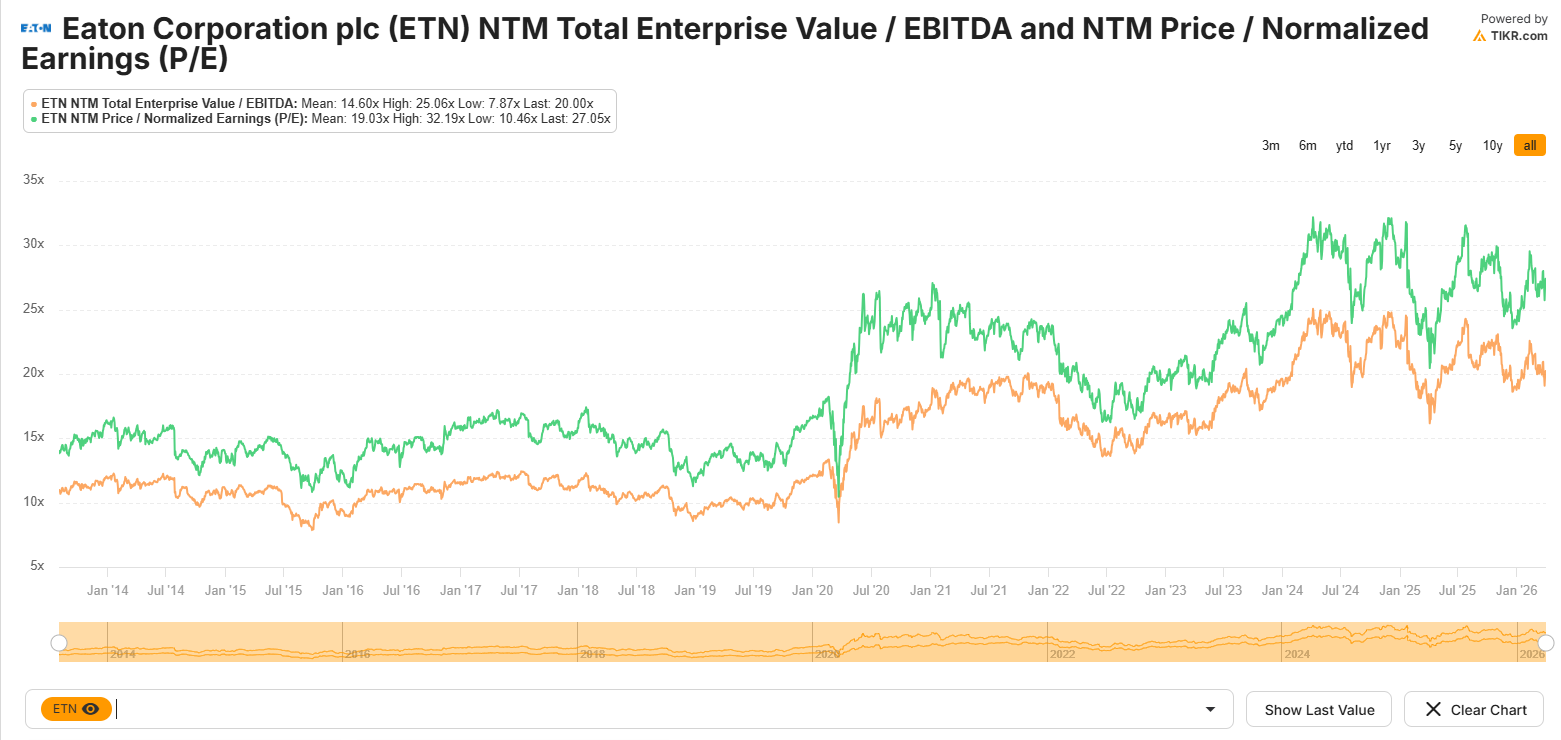

Eaton | ETN | $140.1B

ETN is a diversified power management company that sits right in the middle of the US grid modernisation theme. It designs and manufactures the full stack of electrical infrastructure - transformers, switchgear, circuit breakers, power distribution units, busway systems etc - across every voltage class.

Specifically in the transformer space, ETN is one of the small number of Western manufacturers with the engineering capability to build the transformers. It’s also acquired Resilient Power Systems making them a play on solid-state transformer technology too (see below).

Considering the growth rate estimates for ETN (mid teens for EPS growth), a 27x PE is quite expensive…but there are many stocks that are expensive for a reason and I’d put ETN in that basket.

GE Vernova | GEV | $242B

GEV does much more than solve the transformer bottleneck. It’s a massive global energy company operating across:

Power

Wind

Electrification

Its electrification segment is the fastest growing segment and supplies the hardware and software that connects generation to consumption. The business has an extremely strong moat but the investment thesis relies on you being comfortable buying a stock trading at 62x NTM EPS.

Here’s how I do “back of the napkin” maths on GEV:

Management guidance implies $5-6B in FCF in FY27-FY28 which means GEV is currently trading ~48x 2027 FCF which is a premium multiple, but it’s also a multiple that can be justified when FCF is growing at +40%. I can’t see GEV earning much more than 50x FCF multiple even if the electrification backlog doubles, and the wind segment stops becoming a drag. I wouldn’t be bearish on GEV at all, but I think at current levels you’re not aiming for more than 20-30% upside from here in the near term.

With that being said, I think GEV is one of those stocks you should always follow. If you get a +20% pullback I’d be inclined to invest as a fairly comfortable way to earn ~50% from a trade.

Solid-State Transformers (SST)

There’s a potential long-run solution to this transformer bottleneck though in Solid-State Transformers (SST) and the SiC Revolution.

The conventional transformer is a passive iron core filled with oil. It does one thing and one thing only: It converts voltage.

The emerging alternative is a software-designed power conversion built on Silicon Carbide (SiC) semiconductors. Instead of sitting on a pad and just converting voltage at a fixed ratio, an SST consolidates voltage conversion, fault isolation, power factor correction, frequency regulation, harmonics control, and phase balancing into a single programmable package managed in real time by software.

This means you replace not only the transformer, but the switchgear, tap changers, and capacitor banks as well.

The SST market is still in its infancy. It’s valued ~$180M as at 2025 but the technology is moving faster than I think most realize.

—> Eaton (ETN) acquired SST developer Resilient Power Systems in August 2025.

—> Navitas (NVTS) demonstrated a 250kW SST at APEC in 2026.

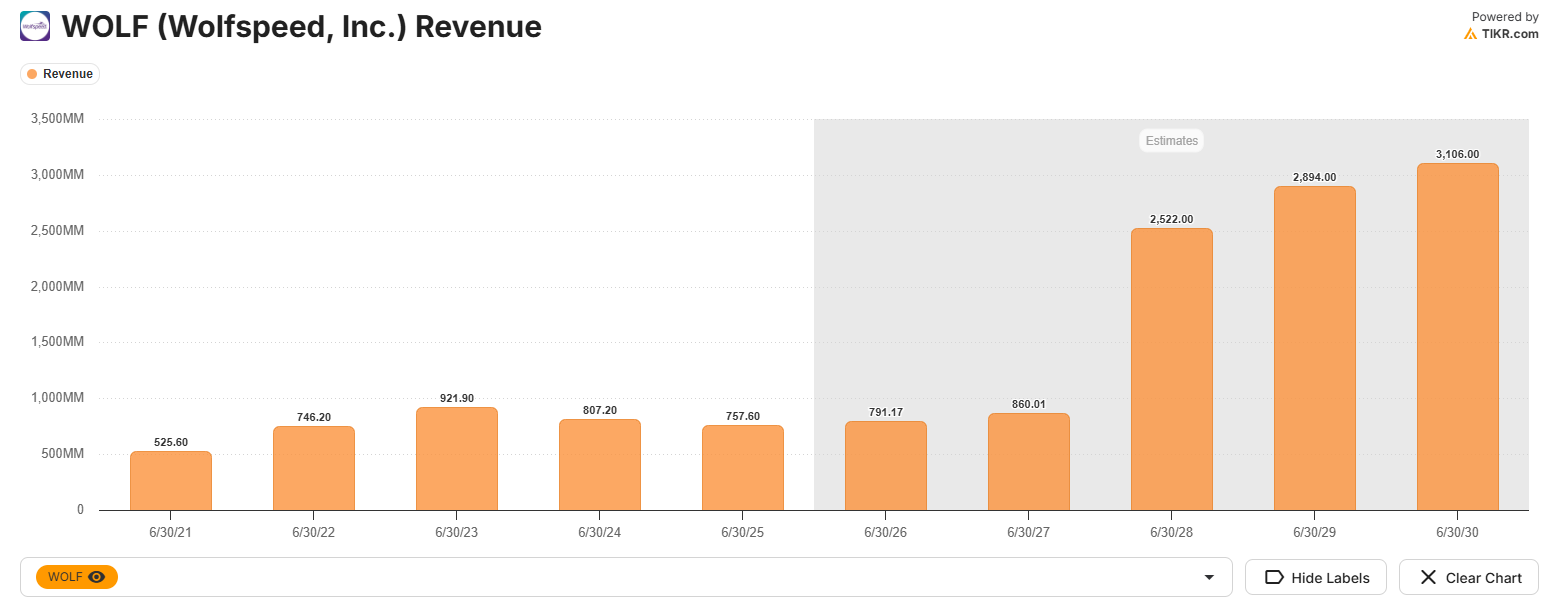

—> Wolfspeed (WOLF) launched the industry’s first commercially available 10,000-volt SiC MOSFET (the enabling technology for SST) in 2026.

Here’s the names you need to know in the SST space:

Wolfspeed | WOLF | $430M

WOLF is the most important name in the SST SiC layer. It’s the US pioneer of silicon carbide…Here’s what a professor from Duke said:

“The timing of WOLF’s commercialisation could not be better. The world is racing to connect AI data centers to the grid, and this will be the enabling technology.” - Dr Subhashish Bhattacharya

This still remains a very high-risk and investment stories aren’t just a play on technology. WOLF’s financials are pretty poor with net income rising, huge debt, and a lot of dilution.

WOLF just issued $379M in convertible notes with is dilutive at $20.14 per share meaning if WOLF trades above $20.14 at any point before 2031, noteholders can convert into equity. The other side to this is that proceeds are being used to redeem existing senior notes…making this more of a debt refinancing rather than a cash raise for continued operations.

“There is a transition happening from traditional transformers to solid-state transformers where silicon carbide is the perfect solution. That transition is starting to happen here. So we’re really playing in terms of energy generation, energy storage systems, solid-state transformers.” - WOLF CEO

It’s a messy capital structure, and a high-risk bet, but I think the reward is there assuming execution. It’s one of those speculative bets I’d be happy to take but position accordingly.

Navitas Semiconductor | NVTS | $2B

NVTS is probably the purest play on the SST thesis today and the financials also look far more solid than WOLF (though the competitive environment is worse), although the stock has moved 450% in the last year alone. That tends to be quite off-putting for some investors, me included, but the thesis is so intact for NVTS here.

Two very important quotes from the recent earnings call:

“You’re going to see first couple of megawatt SSTs, bundled with battery energy systems. Then you see high single-digit megawatt type of SSTs coming up.”

“You cannot deploy remotely half of what we’re trying to deploy with AI data centers with the grid we have today. So for me, AI data center and grid is the same thing.”

Despite the competitive environment being a challenge for NVTS, most competitors are either pure GaN or pure SiC. NVTS has both.

The part I’m slightly cautious about with NVTS is the lack of transparency around profitability timeline. Analysts currently aren’t estimating EBITDA profitability anytime in the next 3-4 years and management haven’t given any specific timeline so this is certainly something to be wary off.

Bottleneck 2: Grain-Oriented Electrical Steel (GOES)

This one is quite multi-faceted.

Grain-oriented electrical steel is the critical raw material used in most transformers. It’s a silicon steel alloy rolled and heat-treated which gives it very strong magnetic properties. Without it, you can’t build a power transformer.

And the vast majority of supply is controlled by a single US producer - Cleveland-Cliffs (CLF).