Highest Growth NASDAQ Stocks With An EV/Sales Below 10

SMCI MELI DASH ZS

Hi all👋

This week we are looking at some high growth NASDAQ stocks that have been beaten down and are trading at pretty low EV/Sales multiples.

Of course EV/Sales isn’t the only way to tell if a stock is cheap or not as it doesn’t give you information about the quality of revenue growth. Looking at it from an EV/EBITDA multiple basis may be better (if they are EBITDA positive) but still it gives us an idea of some undervalued stocks and that’s the whole purpose of these screener articles.

For this screener I used StocksGuide, a new up and coming stock analysis tool that I’m loving. You can click the link above (it’s an affiliate partnership so just a heads up).

My criteria were as follows:

Index: NASDAQ

TTM Revenue Growth: >20%

EV/Sales: <10x

Here’s the results:

SuperMicro Computers (SMCI)

Pinduoduo (PDD)

MercadoLibre (MELI)

ZScaler (ZS)

DoorDash (DASH)

Meta Platforms (META)

Atlassian (TEAM)

DexCom (DXCM)

I’ve decided to look at four of these that interest me the most…which are SMCI, MELI, ZS, and DASH. Let’s get into them👇

SuperMicro Computers (SMCI)

Company: SuperMicro Computers

Ticker: SMCI

Website: https://ir.supermicro.com/ir-overview/default.aspx

Current Stock Price: $438.27

52-Week High: $1,188

52-Week Low: $235

Market Cap: $25.58 billion

Headquarters: San Jose, California

Number of Employees: Not available

Numbers

Revenue growth: 143%

Gross profit margin: 11.2%

Net profit margin: 6.6%

Commentary

SMCI has managed to ride the AI wave with strong partnerships with NVDA, AMD, and INTC but there’s been doubts about the company over the last few quarters. SMCI has performed very poorly over the last 3 months dropping ~49% since June. If you’re looking for a more stable compounder over the next 3-5 years then SMCI isn’t a stock for you. If you’re a slightly higher risk taker then I think SMCI could be worth a consideration due to its volatility.

For me, I’m quite reluctant to invest in SMCI despite some obvious catalysts I see and a fairly cheap valuation mainly because competitors are winning at the moment and it’s never the best idea to invest in companies who aren’t leaders unless the valuation is extremely cheap.

Here’s some information on the opportunities, risks, and valuation:

Opportunities

SMCI have carved out quite a niche part of the AI market in that they focus only on servers and enterprise customers such as NVDA, AMD, and INTC. Competitors are focused on both retail customers and enterprise customers. Whether this is a good strategy or not I’m a bit undecided on but it’s evident that SMCI has a niche that they are aiming to dominate.

The opportunity of being a leader in generative AI hardware is pretty substantial. Gartner upgraded their outlook recently to a 24.1% CAGR in this market so there’s little argument against the fact that SMCI are a big player in one of the fastest growing industries. That alone holds a lot of weight in an investment case.

To become an even more niche leader, SMCI are positioning themselves as the go-to for more energy efficient computing. Many competitors use air cooling systems but SMCI use liquid cooling systems which although is currently more expensive (and one of the reasons for the margin pressures) should play into SMCI’s favor over the coming years as consumers strive for more energy efficient alternatives.

Risks

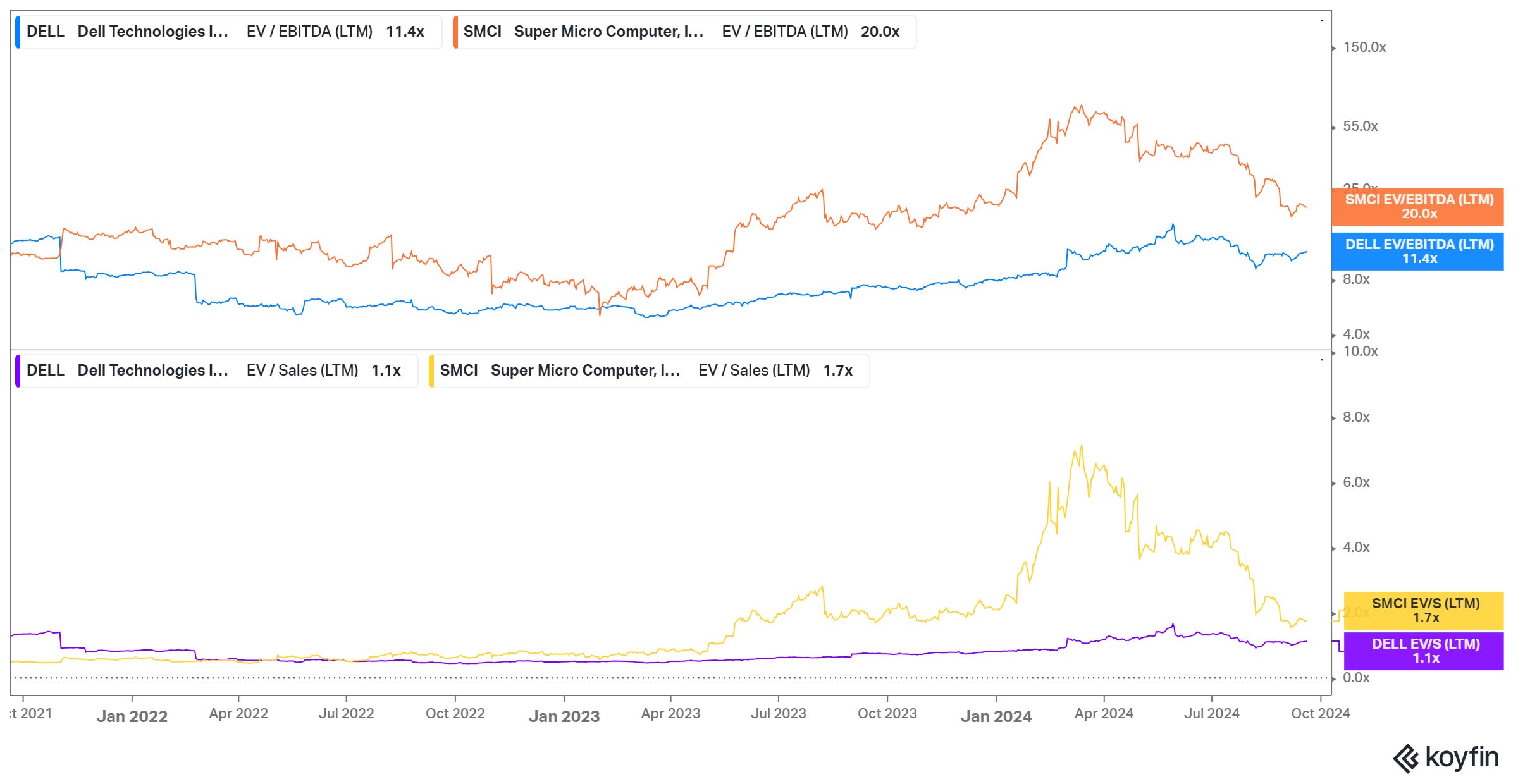

A year ago I was very convinced by SMCI’s growth strategy but I’m starting to have some doubts as competitors like DELL have started to catch up. SMCI were very aggressive in their growth early on, but they have recently struggled to expand margins like DELL have. Whether this is completely down to the liquid cooling systems or not, I’m unsure but the fundamentals for DELL are going from strength to strength whilst SMCI’s are struggling.

Ignoring the numbers, DELL are also starting to win clients from SMCI. For example, TSLA used to work exclusively with SMCI but they now work with DELL. This is the same for CoreWeave, and Digital Ocean.

Here’s a chart that represents DELL vs SMCI at the moment quite well. From a revenue growth perspective (bottom graph) we can see both SMCI and DELL are increasing nicely but SMCI’s FCF has been struggling lately (currently in negative net FCF).

Valuation

To be honest, the valuation is the only reason I am partially interested in SMCI but I’m still not fully convinced that it’s worth it.

Considering that NVDA and SMCI have similar revenue growth, this chart makes SMCI seem undervalued. Particularly on a EV/Sales multiple ratio.

However, then if we compare to DELL which I spoke about a lot above, SMCI is more heavily valued on a multiple basis. I do believe SMCI as a company deserves a higher multiple today but there’s potential that the tide is turning and therefore I don’t believe SMCI is worthy of an investment.

Good company. Impressive growth. But just not good enough.

MercadoLibre (MELI)

Company: MercadoLibre

Ticker: MELI

Website: https://investor.mercadolibre.com/

Current Stock Price: $2,109

52-Week High: $2,122

52-Week Low: $1,180

Market Cap: $106.6 billion

Headquarters: Buenos Aires, Argentina

Number of Employees: 58,313

Numbers

Revenue growth: 41.5%

Gross profit margin: 46.6%

Net profit margin: 10.5%

Commentary

I’ve spoke about MELI a few times in this newsletter so I won’t just repeat what I’ve said before.

What I will do is look into the valuation compared to competitors such as AMZN, SHOP, and SE to gauge how attractive MELI is today. Let’s take a look at the graphs below:

As you can see, MELI trades below SHOP and above AMZN (which I love and now own) and SE. At a revenue growth of 41% I think this is probably a fair multiple but it doesn’t offer an “opportunity” at today’s levels neat ATH. I do think MELI is a very good company in an exciting geographical region, but the opportunity today I don’t believe is there, especially compared to a competitor like AMZN.

Graphic

Revenue growth in the last 3 quarters has stabilized and even grown a bit. Will MELI be able to increase their rate of revenue growth any further?

ZScaler (ZS)

Company: ZScaler

Ticker: ZS

Website: https://ir.zscaler.com/

Current Stock Price: $172

52-Week High: $254

52-Week Low: $148

Market Cap: $25.7 billion

Headquarters: San Jose, California

Number of Employees: 7,348

Numbers

Revenue growth: 30.3%

Gross profit margin: 78.1%

Net profit margin: -2.5%

Commentary

The cybersecurity industry is highly competitive and ZS aren’t currently keeping up with the intense competition. In Q2 earnings they:

Sold off by 18%

Issued weaker guidance (11% decline) for non-GAAP EPS

Margin contraction?

Revenue growth declined for the 10th quarter in a row

Said billings growth is down and expecting only 13% YoY growth

Decline in net retention rate

Decline in current remaining performance obligation

Yet still trades at an EV/Sales multiple of 11.6x which to me seems a bit too much. For these multiples to be worthy of an investment, the fundamentals of ZS simply aren’t good enough.

On a more positive note for ZS, they have managed to expand margins and increase efficiency. We saw operating and net margins continue to trend upwards YoY but there was a decline from Q1. This margin expansion allowed ZS to maintain a Rule of 40 score in the 50% range which is still promising.

Overall, for a company competing in arguably one of the most intense markets (cybersecurity), ZS aren’t performing well enough for me to even consider being an investor. I still believe that SentinelOne is the best opportunity in the cybersecurity industry.

DoorDash (DASH)

Company: DoorDash

Ticker: DASH

Website: https://ir.doordash.com/overview/default.aspx

Current Stock Price: $137

52-Week High: $138

52-Week Low: $71

Market Cap: $53.4 billion

Headquarters: San Francisco, California

Number of Employees: 19,300

Numbers

Revenue growth: 23.3%

Gross profit margin: 47.3%

Net profit margin: -6%

Commentary

I’ve not researched DASH much at all, nor have I spoke about it on X or here on my newsletter so I enjoyed my research on this one and I was pleasantly surprised with my conclusion.

DASH has a core growth initiative of massively expanding its offerings, and therefore its TAM. DASH are in the process of a transformation from a food delivery service to a more general convenience provider that delivers goods such as alcohol, beauty, home improvement, and sporting equipment. Even though these transformation aren’t fully complete yet, the company is still managing to grow top line in excess of 20% YoY which is promising. There’s no reasons we can’t see increased revenue growth rates over the next couple years.

Despite these bullish tailwinds, DASH is still very reasonably valued. Here’s my take:

At a current EV of $38.45 billion.

And 2025 revenue estimates of $12.34 billion (which is 43.99% growth from today)

And 16.3% adjusted EBITDA margin (no change to today)

We have the following multiples:

2025 EV/Sales: 3.1x

2025 EV/EBITDA: 19.1x

For a company with EBITDA growth of 164%, margin expansion, and revenue growth above 20% YoY with big cross-selling opportunities coming up…I think these above multiples are more than reasonable.

I like what I see with DASH and I’m going to add this to my deep dive list.

That’s it for the day

I hope you loved this article. As I continue to develop on here, I’m sure there will be some changes to my structure and style, so please do leave some feedback for me.

Please subscribe to my newsletter where I provide investors with all the tools to outperform the market, and retire well before you’re 65. You can also follow me on X.