Is Alibaba Too Cheap To Ignore Now?

I think so.

As primarily a value investor, I’m looking for opportunities where there is limited downside, and large upside.

“If you buy stocks with a sufficient margin of safety, the probability is with you” - Bruce Berkowitz

Well, with Alibaba the upside potential is huge, but the downside potential is still larger than I’d hope for.

We’ll dive into the numbers later, but to me it’s clear that there is a huge margin of safety when looking specifically at Alibaba’s business

One-Pager

Here’s the One-Pager I put together for Alibaba.

It gives you a brief outline of the business and some of the fundamentals to look for. I’d recommend if you analyze a stock yourself, to dive further than just what I included here though.

China

Now there’s one main problem that makes this BABA 0.00%↑ investment riskier than I’d like it to be…and that’s China.

Specifically:

China’s Debt Trap

Slowing Economy and Deflation

Taiwan Conflict

In many cases, I ignore the macro noise, because quite frankly nobody has ever consistently predicted it correctly.

Take a look at this post on X I just did!

However, China has some more complexities currently and these need to be analyzed as part of a general risk assessment for BABA 0.00%↑

Let’s take a look:

Debt Trap

Real estate accounts for over 30% of the GDP of China and China’s property developers collectively owe more than $390 billion to suppliers.

Now of course this isn’t ideal. But we’ve seen similar crises in other countries before.

The issue with the China narrative is that it’s being compared to a depression like Japan where times of rapid growth and success are over, but it’s very different.

Japan had more than just a property bubble. Everything was inflated. This isn’t true in China…prices are at some of the lowest valuations ever.

Secondly, in Japan everything was intertwined. Banks owned companies and companies owned banks. This led to a complete breakdown of the economy all at once. Again, this isn’t the same in China. One industry will not affect another industry.

Slowing Economy and Deflation

There’s been a slow recovery post COVID, worries about deflation, and political concerns. Subsequently, sentiment isn’t strong.

But, since 2022 income and consumption have made a strong comeback. Consumption grew 8.4% in the latest quarter (compared to nominal GDP growth of 5.4%).

This means that the narrative about consumer sentiment isn’t what is causing these issues. It more related fewer exports, and debt, basically global economic weakness.

This can be seen looking at imports into China which fell 8% in the first half of 2023, but as I’ve been talking about this whole time so far, it’s not as bad as it seems.

The only reason for this drop is due to import prices, not volume, which has actually been growing, thus rising domestic demand.

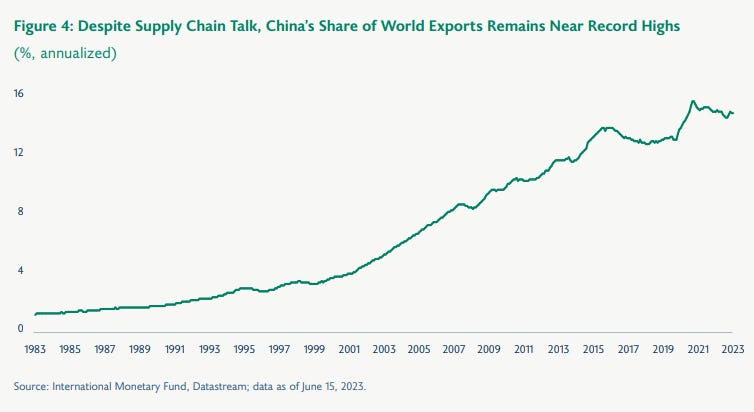

Exports also remain at record highs and China remains an integral part of the global supply chain.

Taiwan Conflict

The ongoing potential war with Taiwan is scary to say the least. I hope for peace but I’m not sure.

But what I am sure of is if a war breaks out between China and Taiwan, stocks will be of little worry compared to a war.

Furthermore, (as always) I believe the media has been exaggerating any news recently. The Taiwanese population, and experts in the field, do not believe that it is probable there will be any military conflict.

This risk is only priced into Chinese equities too. Many companies (Apple to name just one) wouldn’t be Apple without China. If a war breaks out, the value of AAPL 0.00%↑ would drop 20%-30% at minimum.

19.2% of Apple revenue is from China

95% of products are made in China

So why is risk only priced into Chinese equities?

Nevertheless, it gives a BABA 0.00%↑ investment (and many other Chinese companies) a good margin of safety.

Macro Conclusion

I see long-term fundamental value in Chinese equities because:

The pessimist outlooks do not appreciate China’s role in the global economy and how important China is to global supply chains.

Beijing has begun stimulating the economy (see below)

Periods of risk can lead to emotional selling by investors and this is exactly what has happened in China. With risk comes opportunity, and China will remain a global superpower despite all the media you hear.

With diligence, value investors like ourselves can generate solid returns with good margins of safety by investing in fundamentally strong Chinese companies.

Now, Alibaba…

A background

Many associate Alibaba as an e-commerce giant, but BABA 0.00%↑ has much more than that. There are 6 main divisions at Alibaba:

Taobao TMALL Commerce Group - This group covers Alibaba’s domestic e-commerce marketplace and builds an ecosystem for brands and merchants on the platform.

Cloud Intelligence Group - This groups houses the cloud business, the AI applications of Alibaba, and Ding Talk (communication service).

Global Digital Commerce Group - This group controls overseas marketplaces such as Lazada and Trenydol.

Local Services Group - This group covers good and grocery delivery services such as Ele.me app and Amap (China’s equivalent to Google maps).

Cainiao Smart Logistics - This group is in charge of logistics and serves 3rd party clients.

Digital Media and Entertainment Group - This group houses Alibaba Picturs and Youku (which is China’s equivalent to YouTube).

Cloud Inelligence Group (Note)

In late 2023, the US expanded its export control rules to further restrict the export to China of advanced computing chips and semiconductors.

This will not doubt affect the Cloud Intelligence Group the most which is perhaps the largest micro risk to Alibaba right now.

This has also created uncertainties for a proposed spin-off of the Cloud Computing Group which is unlikely to now happen.

Financials

Income Statement

Alibaba was growing revenue between 2018 to 2022 at huge rates. I’m talking 30%+ annually.

Those days are over and that’s another reason for the bad sentiment around Alibaba’s future, but those revenue returns aren’t sustainable.

Currently revenue growth is at 6.5% vs March 2023, which is a solid period of growth compared to a slump in late 2022, and early 2023.

Though growth has slowed, we are seeing a strong return to profitability and stronger revenue growth. This is in line with our macro analysis above that Chinese consumers are starting to spend again.

Balance Sheet

Alibaba has a huge amount of cash which gives any investor a peace of mind. Cash is currently at $33.4B and short term investments are $45.3B, giving a combined $78.7B.

Compare this to total current liabilities of $53.4B, there’s no concerns about short-term liquidity or long-term liquidity as long term debt sits at $21.7B. Again, BABA 0.00%↑ is in a position to pay these debts at any time in cash.

The current ratio currently sits at 1.9.

Share Buybacks

Becuase of this huge amount of cash (and retained earnings of $87B), and a low stock price, Alibaba is currently in the middle of a share buyback program worth $25B.

This is bullish. It increases one’s share in a business, and it shows management are able to allocate capital well.

Over the last 12 months, BABA 0.00%↑ have spent $9.5B on share buybacks which has reduced the total outstanding share amount by 3.3%.

Although history at Alibaba has suggested that they rarely use the total allotted amount in the end towards the program, this is still a positive sign. Nevertheless, investors would be a lot happier if we saw BABA 0.00%↑ using the full $25B.

Economic Moat

There’s no doubt Alibaba has a strong economic moat, especially in the e-commerce market where Taobao and TMALL are China’s two dominant e-commerce marketplaces. The platform is the largest in the world and this scale alone gives the Company advantages in logistics infrastructure.

However, BABA 0.00%↑ is in far more than just e-commerce which gives them a strong moat in terms of diversity too. This has helped Alibaba reduce its dependency on e-commerce and therefore enter new markets.

Looking from a purely financial perspective, gross and net profit margins have shrunk about 8% since 2019 which is likely due to costs and pressure from competitors. The moat isn’t as strong as it once was, but it’s still there.

Opportunities

Cloud Market

The Cloud market is expected to grow 15% annually and its currently a $250B opportunity. The winners in this market will reap massive rewards.

Currently, the five big players in the market are:

Amazon (AWS)

Azure (Microsoft)

Google Cloud

Alibaba Cloud

IBM Cloud

However, 65% of the market is taken over by Amazon, Microsoft, and Google. BABA 0.00%↑ only has a 4% market share and is growing less than the other big players.

However, the positives are as follows:

China doesn’t want US Cloud providers in their market.

The economic situation in China will bounce back, and the China Cloud market will inevitably grow fast once it does (predictions are above 25% annually).

China has the largest online population in the world. Whoever dominates this sector will do well. Currently the China Cloud market breakdown is dominated by Alibaba (39% market share). Next up is Huawei with a 19% share and Tencent with a 15% share.

E-commerce

Alibaba has plans to expand into Europe, which has an anticipated e-commerce growth rate much larger than Asia and the Americas.

Alibaba have tried this before, but ultimately failed due to fiscal measures imposed by policymakers. The new tactic is more locally focused on individual countries with a pilot project in Spain currently underway.

In my opinion, I think they’ll struggle due to dominance of Amazon. But, let’s see. It’s an opportunity nevertheless.

Valuation

Discounted Cash Flow

Let’s take a look at the relationship between expected future cash flows and the current price.

Obviously many assumptions are made, but I get a price per share of $233.72 here. That’s a 228% increase from today’s price.

Let’s look at the assumptions I made:

Base case: I assumed a growth rate of 8%. I do expect growth to be more than this, but I’m uncertain when the Chinese economy will recover. I therefore chose 8% as an average over a 10-year period.

Worst case: In the worst case, I’ve essentially assumed everything negative the Chinese media talk about comes into fruition. GDP growth will decrease and Alibaba will only just outperform that at 4% per year. Also, all investments will basically stop which would lead to a terminal value of ~8.

Best case: The best case scenario considers that Alibaba Cloud performs well and returns to double-digit growth (which I think is possible in the Chinese market). Based on this, the multiple would be 16+ easily. I don’t think this is an unrealistic expectation by any means.

FCF Yield + PE Ratio

Here’s a graph showing FCF Yield (black line) and PE Ratio (blue line).

FCF Margin is the highest it’s been in and PE ratio is the lowest its been. More signs to show that the company is undervalued.

Overall

I know that a lot of this article actually focuses on China, rather than Alibaba. The more I researched, the more I realized that Alibaba’s price is currently far more dependent on the Chinese economy, rather than the business.

So that’s where I tried to put my focus.

To close, I’m personally a buyer of $BABA. The margin of safety is huge, and the upside potential is also huge.

That’s it for the day

I hope you loved this article. As I develop on here, I’m sure there will be some changes to my structure and style, so please do leave some feedback for me.

Please subscribe to my newsletter where I provide investors with all the tools to outperform the market, and retire well before you’re 65. You can also me follow me on X.

Oliver, I decided to stay away from Chinese stocks even if they're traded on American exchanges. They don't always comply with listing requirements and adopt obscure financial practices. Not to bash $BABA here - I'm not blaming them for anything in particular. It's that some Chinese stocks have had issues on US stock exchanges.

Now, technical analysis suggests the stock is below its fundamental value. There was institutional accumulation between $88 and $100. But... This doesn't mean the stock is about to surge. Overall, $BABA is a solid company but I see other bargains in the market.