Ouster (OUST): Here's My Prediction

OUST Deep Dive

“Everything that moves will be robotic someday, and soon.” - Jensen Huang

Company Name: Ouster

Ticker: OUST

Market Cap: $1.34B

Headquarters: San Francisco

Shares Outstanding: 62M

CEO: Angus Pacala

Revenue Growth: 52.5%

Introduction

The vast majority of my ideas stem from identifying megatrends, finding the quality companies within those themes, figuring out what is a fair valuation for that business, and then finding a nice technical entry for that position.

This is a perfect example of how I first initiated my position in OUST.

I dived into the basic numbers in my database for robotics, I then spent hours diving into the company and the valuation, and then I tracked price closely to find a nice first entry.

OUST is now sitting slightly below my initial $25 entry at $21. It’s now at a level where I feel extremely comfortable going bigger on the position.

Just like I did with LMND in the $30s, SOFI below $10, PLTR below $40, SVM below $3, ALB below $80, AMPX below $12… and so on.

The only difference with OUST currently is that it has yet to make its move.

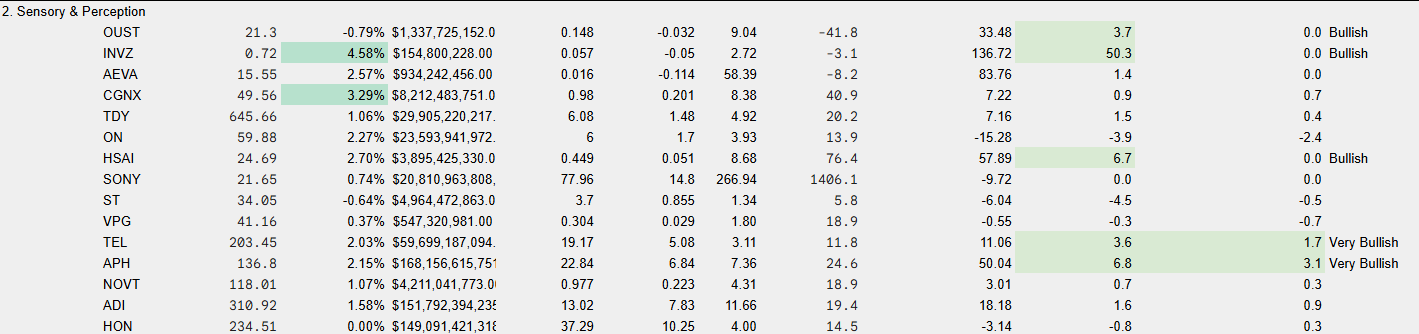

Big picture, my view is that OUST is positioned perfectly in the middle of the robotics and automation megatheme. More specifically it’s in the sensory & perception subtheme of this basket. Here’s a snippet of my database which my paid subs have access to.

As you can see other players in this niche (though not competitors to OUST) are AEVA, CGNX, INVZ, TEL, APH etc. My database tracks multiples, expected growth rates, and technicals like MA’s to give an initial recommendation of the stock and its valuation.

It screens out all of those positions that likely are too expensive, or with too slow growth right away for you allowing you to focus your time on those quality stocks.

For example, in the sensory and perception niche, the best names are OUST, HSAI, TEL, and APH.

Just within the robotics tab alone, we have +140 stocks broken down in subthemes within the wider theme.

Paid subs will know that I already have a position in OUST at $25 which makes it my biggest pure robotics play (if you exclude NVDA and GXO). I’m currently down 15% on the position but with the robotics megatheme likely to be a +10 year theme, I’m fully prepared to own this one for the next few years unless anything materially changes within the business.

In this Deep Dive, I’ll cover the following:

What OUST does

Recent financials

Opportunities

Valuation

Technicals

My take and plan

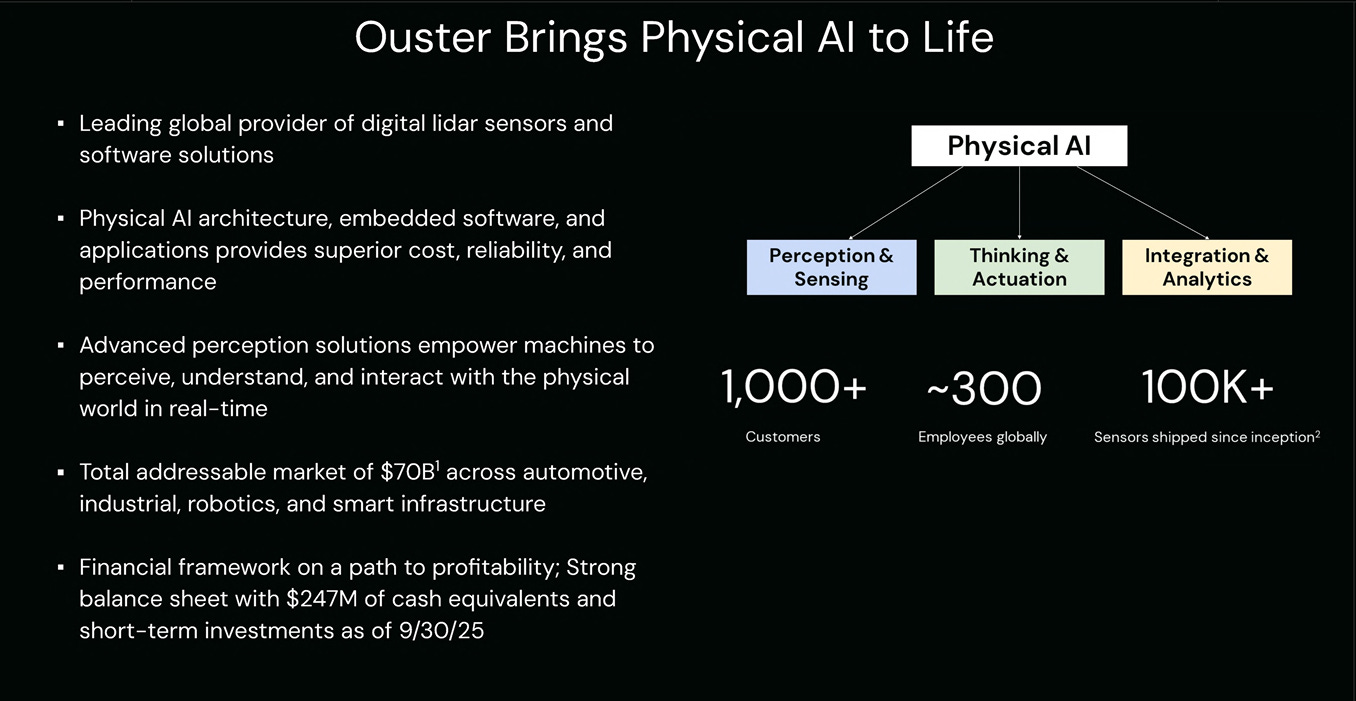

What does OUST do?

OUST is the largest Western LiDAR provider (Light Detection & Ranging). LiDAR is a remote sensing technology that measures distance by emitting short pulses of laser light at objects and calculating how long it takes for the reflected light to return. It then converts that time into precise 3D distance and position information.

It’s basically the eyes of a robot, or the eyes of machines that need to move autonomously.

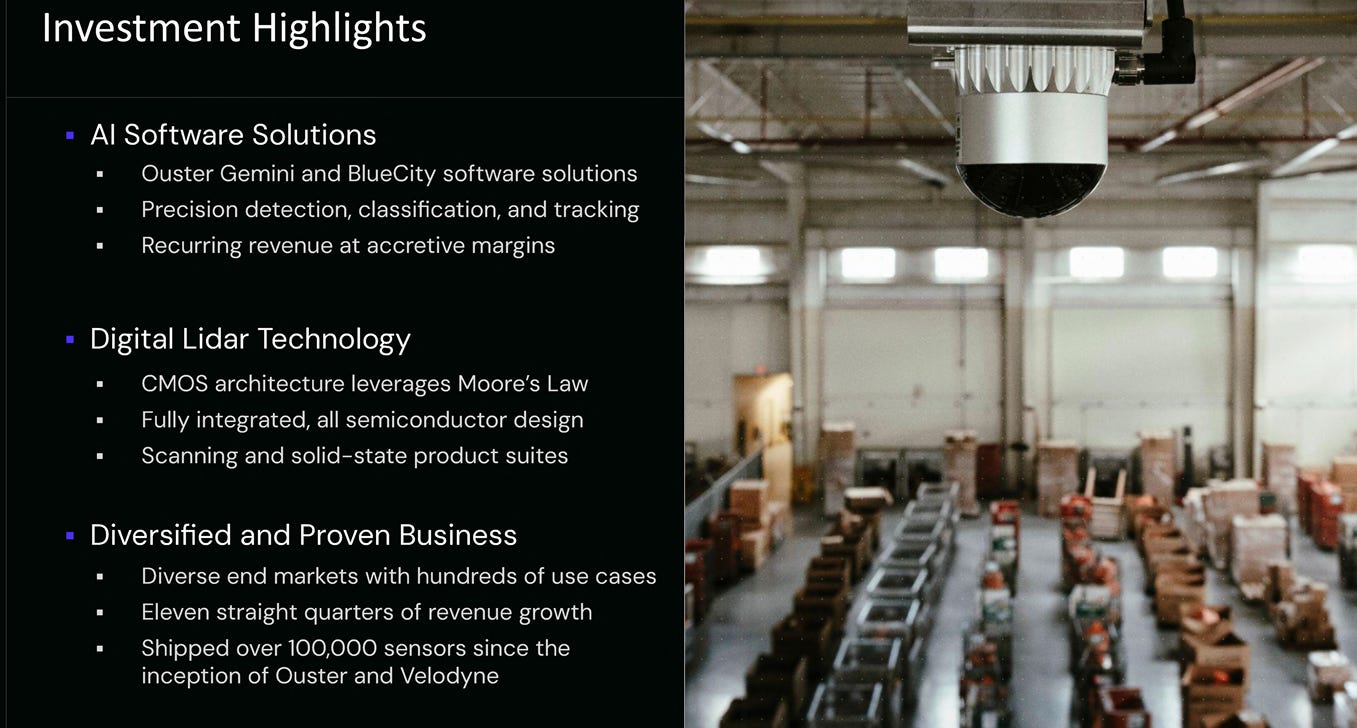

OUST’s differentiation is that they’re a digital LiDAR company.

Traditional LiDAR is analog meaning you fire a laser, swipe it mechanically, capture returning photons, and then reconstruct a 3D point load with a lot of complexity. Each new product generation must mean a new optical design and a new assembly process.

Digital LiDAR on the other hand is the idea of putting the complexity of LiDAR technology onto a silicon chip. Key functions of the sensor (photon detection, timing, signal processing etc) all are implemented in custom semiconductor chips rather than bulky analog assemblies. Here’s why this matters:

This allows OUST’s products to ride the Moore’s Law wave with performance. This means that OUST’s technology improves exponentially like other semiconductor products have done over the last 3-5 years.

Digital LiDAR is also designed to follow the semiconductor cost curve, i.e. OUST can make smaller sensors that are more power efficient and have better performance.

I can’t write this Deep Dive without acknowledging LiDAR’s biggest bear… Elon Musk.

Here’s a summary of Musk’s argument:

Cost: Musk says LiDAR adds an expensive and unnecessary sensor to vehicles when cameras can achieve autonomy at a fraction of the cost.

Weather sensitivity: He claims LiDAR performance is poor in rain, fog, and snow so it’s not fundamentally robust.

Power requirements: He claims LiDAR has far higher power requirements and system complexity.

An “unnecessary, expensive appendices.” - Elon Musk

Whether you agreed with Musk or not, the risk of LiDAR not fulfilling the expected forecasts has been mitigated quite a lot post 4th February 2026 OUST’s acquisition of StereoLabs - a leading AI vision and stereo-camera company.

OUST paid $35M in cash and 1.8M OUST shares (vesting over 4 years) for the company. I’ll dive into the expected numbers of this acquisition in the valuation section but fundamentally here’s why this acquisition will work so well.

Overnight, OUST went from a LiDAR company (with risks as Musk claims) to a LiDAR + camera + AI vision software company.

This repositions them as the leading Physical AI sensing and perception platform…rather than the leading LiDAR company. The market is still underappreciating this transition as the stock is flat since the news. This OUST stack now includes:

High performance digital LiDAR

Stereo cameras and depth cameras (ZED line)

AI compute and sensor-fusion middleware

Perception software and AI models that detect, classify, and track objects in 3D.

OUST can now sell a full perception layer to customers rather than selling LiDAR / sensors into someone else autonomy stack. Financially, it also allows OUST to work towards higher margin, recurring, software revenue on top of their hardware sales. Most one-off sales hardware companies struggle to ever get rewarded with strong multiples like recurring revenue software companies do.

“This acquisition builds on Ousters momentum and positions us as the foundational end-to-end sensing and perception platform for Physical AI.” - CEO Angus Pacala

If customers want more vision and less LiDAR, OUST can still participate. If customers decide they want more LiDAR and less vision, OUST can still participate.

Financials

Demand

Q4 25 Revenue: $62M

$41M was product revenue and $21M royalties (primarily one-tme).

Product revenue growth was +36% YoY in Q4 and full year revenue growth was 52% YoY (or 32% excluding royalties).

2025 full units: 25,000 sensors shipped which is +48% YoY

Industrials was the largest contributor to revenue, followed by robotics and smart infrastructure.

Software is now on ~15% of sensors shipped which is a 120% increase in software attached sensors relative to last year.

Profitability

Q4 GAAP Gross Margin: 60% with 20 pts from royalties which implies a 40% ex-royalty margin.

Full year 2025 Gross Margin: 49% with 8 pts from royalties implying 41% ex-royalty.

Full year OpEx: $157M (+9% YoY)

This increase relates to investment in the roadmap, StereoLabs costs, compliance etc).

Q4 25 adjusted EBITDA: +$11M (mainly because of royalties). Full year Adj. EBITDA was negative $12M (vs negative $42M in FY24).

Analysts expect EBITDA profitability in FY28.

Guidance

Q1 26 revenue guidance: $45-48M which includes ~7 weeks of StereoLabs contribution.

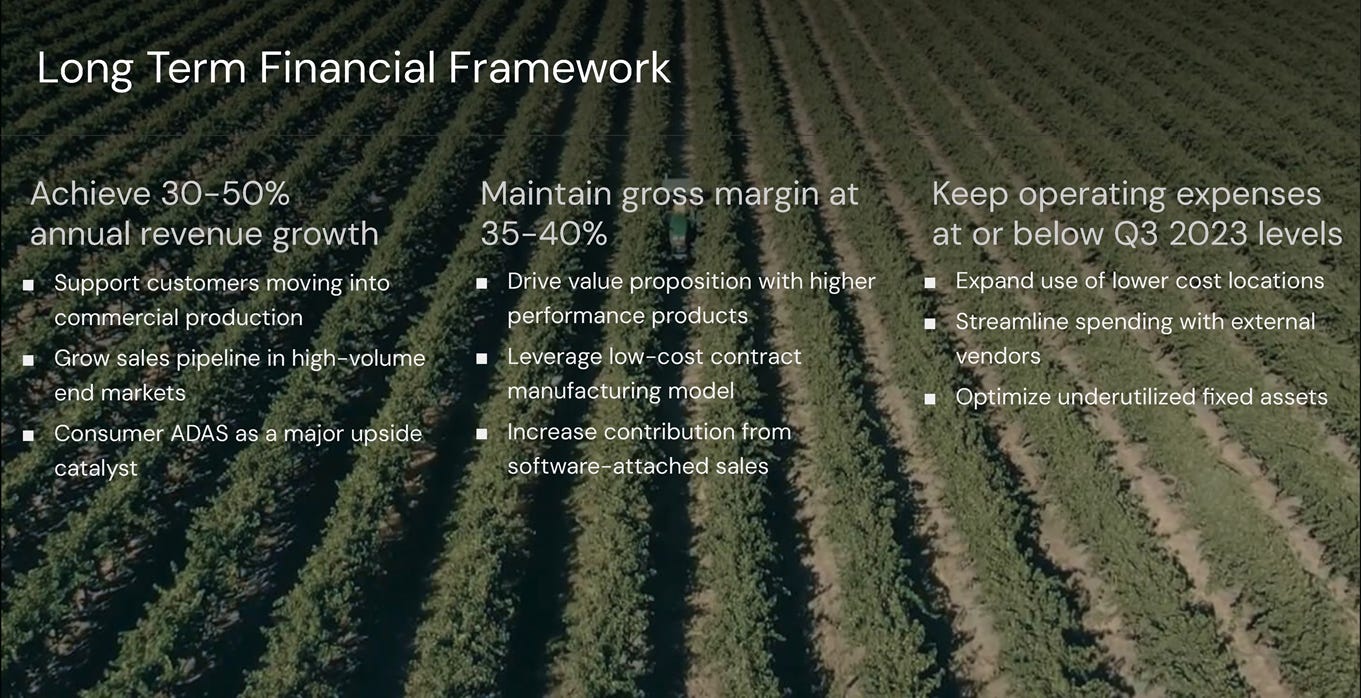

Long term financial framework reiterated 30-50% annual revenue growth with 35-40% GAAP gross margins.

Management expect growth and operating leverage to provide a “clear path” to positive operating FCF and profitability with “plenty of operating runway.”

Balance Sheet

Q4 25 cash position: $211M (note this is pre StereoLabs)

StereoLabs acquisition led to a $35M cash outlay (plus stock)

Debt: $0

Opportunities

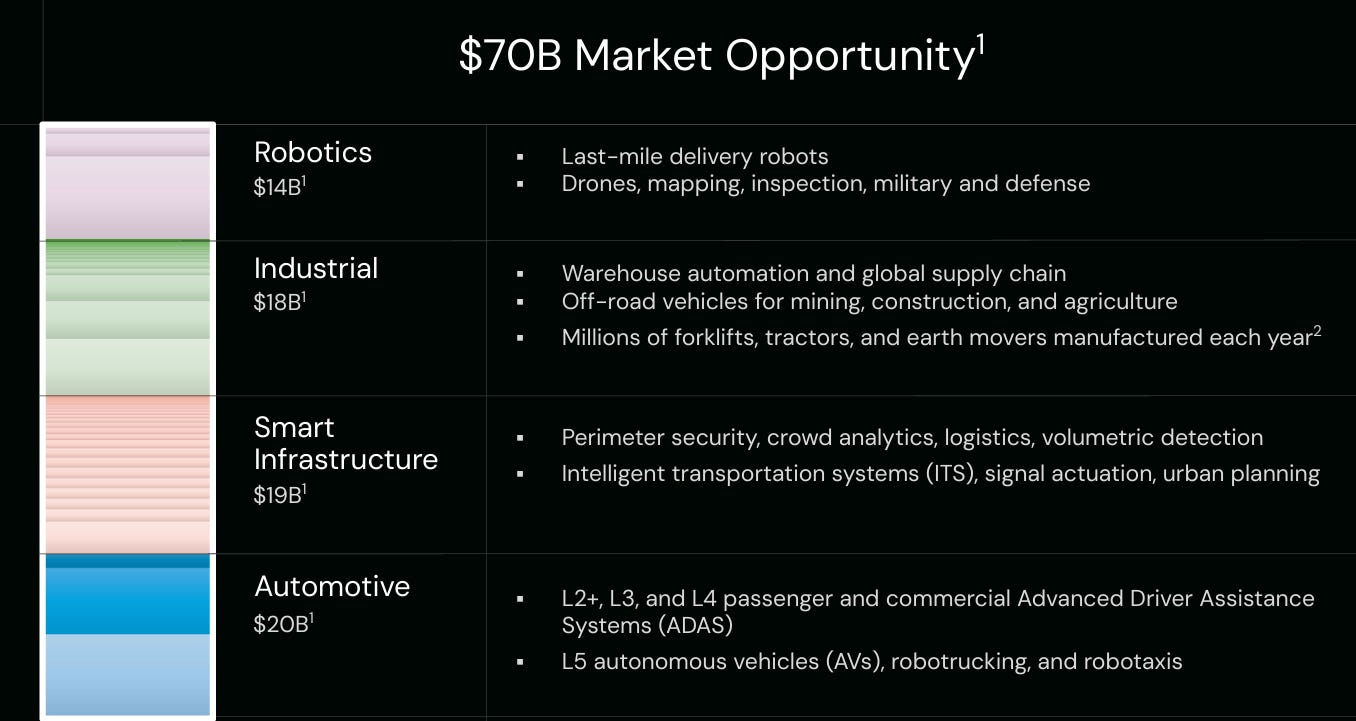

Total Addressable Market (TAM)

OUST management have consistently said $70B is their TAM. This has been the case for the last 18 months or so. With OUST expected to do $220M in revenue in FY26, that means OUST has currently won 0.314% of the opportunity right now.

This kind of TAM reminds me of companies like LMND, PLTR, SOFI etc with almost unlimited growth ahead.

But here’s where it gets more interesting for me. All of this $70B commentary came pre StereoLabs acquisition. StereoLabs is a small business today, but it’s very meaningful in terms of the value add it offers.

The stereo-camera / 3D camera market that StereoLabs operates in is a $2.5B market but the software and perception layer that this acquisition adds probably puts the TAM far above $70B in the long term. I won’t put a forecast out there for what I think the TAM likely is as it’ll but no more than an educated guess, but I suspect it adds far more than just a few billion dollars to the market OUST can win.

More importantly, in the short term it should increase OUST’s share of the wallet within the existing $70B Physical AI stack.

Many investors still label OUST as a “auto LiDAR” play. Let’s dive into how far off this narrative is:

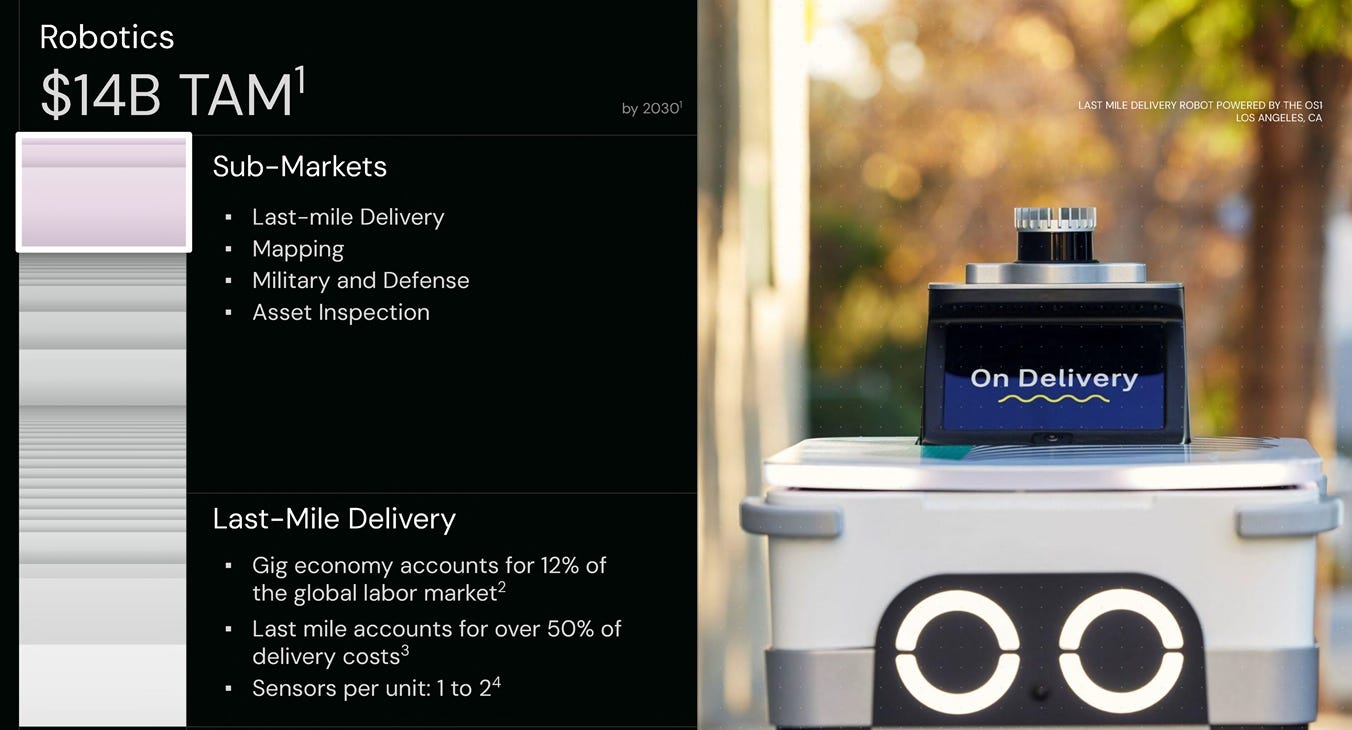

Industrial LiDAR is OUST’s biggest (or 2nd largest) segment today and management peg it at a $18-19B opportunity by 2030. This opportunity encompasses the heavy machinery plays like AGVs/AMRs in warehouses, ports, mining trucks, construction, and agricultural equipment (John Deere for example). Current industrial revenue is in the tens of millions range within the $169M 2025 revenue. This implies far below sub 1% penetration in a market that is set to move from R&D to production very quickly. I’ve said this about my bullishness on GXO, but this subtheme within Physical AI is very likely to be the niche that moves first. This is the theme that is in the most repeating and stable environment in a relatively constrained labour market. In agriculture, this is exaggerated even more.

Humanoids is OUSTs small, but emerging opportunity. OUST’s customers include Serve Robotics (SERV) for example but this will likely take a lot more time to materially affect the numbers. But if you’re aware of the forecasts someone like Elon Musk has put out for the humanoid market, then ignoring OUST’s potential here is naive. This is where OUST’s management team have been very intelligent. OUST could have easily been grouped into the AV and humanoid niche like many other LiDAR providers. The timeline on these subthemes is still very unclear and likely will be quite unclear for the next 2+ years or so. If that were the case, then I would understand OUST’s valuation here at $1.2B market cap a bit more, but OUST has industrial and smart infrastructure scaling quite rapidly now.

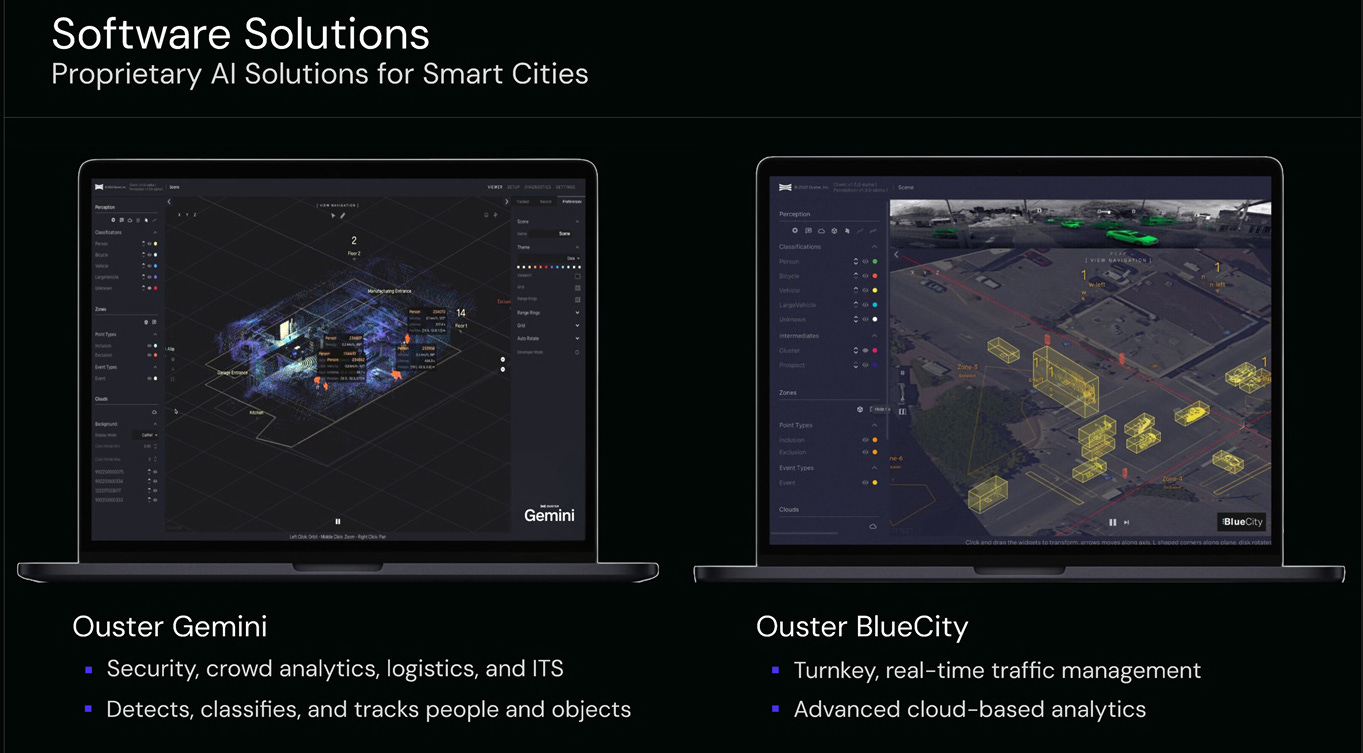

Smart infrastructure is OUST’s largest or second largest segment today with an estimated $19B TAM. This spans traffic management, security, spatial analytics for example. Gemini and BlueCity have been the most important contributors in this segment for OUST not only for material revenue today, but also because software attached bookings have more than doubled here. Contract developments for BlueCity and Gemini now exceed 1,200 sites worldwide. A lot of this opportunity depends on if LiDAR based detection becomes a standard for intersections, public spaces, and private campuses but if it does the TAM will likely be much larger than $19B. Ultimately, we’ve seen through Gemini and BlueCity that the market is looking for full stack solutions. Not many enterprises want pure components now since it becomes too complex to integrate everything. There’s already evidence in the software attached sales that OUST are strong here and it’s only the very early days.

Automotive is the other smallest revenue contributor (single digit percentage) today but a huge piece of the long-term value. Most of the reason this revenue is quite slim today is because programs are largely in pre-production even more so than in the other segments. Robotrucking is a multi-billion dollar ($70B+) opportunity itself with the LiDAR specific part of that likely well above $1B. For OUST today, it’s mainly small R&D and pilot revenue, but once autonomy on the roads becomes a lot more common, these small wins so far can flip into a huge amount of units sold.

I think it’s clear that OUST is a diversified and proven business so far, and it’s still in the very early innings. They’re selling into 150+ use case across four key verticals whilst LiDAR peers generate little revenue on negative margins in one or two segments max whilst they wait for one or two OEMs to ramp up.

For example:

Hesai (China): Extremely concentrated in automotive and robotaxis. It’s essentially a one-theme bet on Chinese AV adoption.

RoboSense (China): Extremely concentrated bet on robotics. Another one-theme bet.

Innoviz (US): Extremely concentrated bet on automotive market.

There’s no other LiDAR player that is anywhere near as diversified, with such strong margins, that is investing into the entire Physical AI perception stack like OUST.

This mismatch between current revenue and segment specific TAM alone should give you a pretty good read on where OUST is likely to head. OUST is already embedded across those niches so the 2030 outlook is not whether there’s room for OUST to grow, or how much they have to win, but it’s how fast those deployments and those markets scale from R&D (hundreds and thousands of units) to full production (tens to hundreds of thousands of units).

Financials

Growth Rates: OUST management has given us a reasonable way to look out to 2030. I’ll dive into this a lot more in the valuation section, but with 30-50% annual revenue growth we can quite easily hit $700M in revenue by 2030 (absolute base case), and much more likely we hit $850-$950M.

Profitability: OUST management have consistently said that GAAP gross margin will be in the 35-40% range. You’ll note that Q4 25 gross margin came in higher but this was artificially boosted by high margin royalty revenue. This is why the market didn’t react a lot. Firstly, I think 35-40% is the absolute base case. There’s clear potential that post StereoLabs and the mix towards higher margin recurring revenue should create more upside than perhaps management are forecasting (publicly). In the near term though, my models are assume ~40% gross margins. The main reason 40% gross margin is likely for the next few years is because as customers go into volume production, unit prices from OUST will drop. It’s healthy/necessary to ensure that OUST win large unit contracts but it’s also a headwind for margins. It will be the main offset to cost controls and software integration which are margin expanders.

OUST management are clear they will happily trade some gross margin for a 10x increase in volume. As an investor, with a TAM the size of $70B, going after margins and profitability as a $1.2B company would be massively off-putting.

If the opportunity wasn’t so large, then sure, it’s arguably just as important to focus on profits as soon as possible, but OUST management know the space they’re trying to win. There’s no point sacrificing a huge ramp up in revenue for a few bps on gross margin today.

Edge AI Upside

If you look at exactly the roadmap that has happened with cameras you’ll note the first phase is always raw imaging, specs, resolution, low-light performance etc… just as LiDAR is today with range, points per second, and cleaner point clouds for example.

Now leaders like Hikvision, and i-PRO are shipping cameras with embedded NVDA chips that run AI models on the edge. This object classification is happening in the camera itself rather than on a backend server.

For OUST, the opportunity is to make LiDAR run the same playbook over the next few years and capture the huge value shift that will happen when intelligence moves into the sensor (i.e. at the Edge). If LiDAR follows the same camera-style evolution that we’ve seen, OUST’s digital LiDAR chip, and it’s full stack physical AI perception profile, will be a ginormous market.

NVDA Partnership

NVIDIA is becoming the de facto compute standard for robotics, automotive, and industrial AI – and Ouster is wiring itself directly into that ecosystem. When an OEM picks an NVIDIA platform like Jetson or Isaac, they effectively lock in a 3–5 year roadmap: they build and validate their perception and control stack around that compute, then roll it out across product lines. Ouster is doing the same thing on the sensing side. Customers choose Ouster’s digital LiDAR, perception software, and datasets, then spend years integrating, validating, and hardening that stack in parallel with NVIDIA’s platforms.

The result is that Ouster ends up embedded alongside NVIDIA in long‑lived deployments. Strategically, Ouster is making sure this scales horizontally: DRIVE and ADAS for autonomy, Jetson for edge robotics, Isaac and Omniverse for simulation and digital twins. As long as Ouster’s sensors are natively supported, well‑documented, and easy to use inside these NVIDIA toolchains, it can position itself as the default 3D sensing option for developers and OEMs who are already all‑in on NVIDIA. Being “the LiDAR that just works with NVIDIA” is a very attractive place to sit.

The economics for Ouster are straightforward. On the growth side, NVIDIA is plugged into almost every high‑growth segment of Physical AI – from warehouse robots and industrial arms to AMRs, drones, construction equipment, and autonomous vehicles – and Jensen is on record saying they’re working with essentially every robotics company they know. If Ouster consistently ships the LiDAR and perception stack that rides shotgun with Jetson and Isaac into those designs, it effectively surfs the same demand wave. On the retention side, every new application built on NVIDIA + Ouster increases the customer’s sunk cost in Ouster’s data formats, calibration, models, and integration code. You don’t casually rip out that sensor and swap it for a competitor without redoing years of engineering and validation.

Put differently: NVIDIA provides the gravitational pull on the compute side; Ouster supplies the LiDAR and 3D perception that click into that gravity well when depth sensing is required. If a developer standardized on NVIDIA can also standardize on Ouster with minimal friction, you get exactly what long‑duration investors want to see – more growth, more retention, and increasingly durable attachment of Ouster’s sensors and software to the winning Physical AI compute stack.

US Manufacturing

One underappreciated opportunity for OUST is how well it positioned itself to line up with the current US onshoring and secure supply chain. They’ve proactively shifted manufacturing outside of China and de-risked themselves here. Whilst Chinese leaders like Hesai and RoboSense will undoubtedly dominate the Chinese auto and robotics markets, Western OEM’s, defense primes, and infrastructure operators will be encouraged (in some cases obliged) to source from Western providers like OUST.

Valuation

Here’s where it all ultimately matters. There’s no point buying a quality business if the valuation doesn’t make sense.

For OUST it makes complete sense. Here’s why and here’s my 2030 prediction.

I’m looking at this valuation a few different ways.

Relative to LiDAR peers

Relative to perception/physical AI peers

Model through to 2030

Keep reading with a 7-day free trial

Subscribe to MMMT Wealth to keep reading this post and get 7 days of free access to the full post archives.