Silver: Why This is a Great Investment For The Next 5+ Years

And The Best Stocks

Think of the bottlenecks.

AI started as a computing power problem. It then became a memory and packaging problem. It then became an electricity problem. It’s now a physical materials problem.

Jensen Huang is telling us exactly this as well. He estimated an $85 trillion physical world infrastructure upgrade over the next 15 years and I bet silver plays a bigger role in all of that than many people are expecting right now.

My focus recently has been less on the stocks/thematics people are agreeing with (optics, thermal management, power systems etc) and more with those thematics people aren’t talking about as much (silver, metals, chemicals).

I’m not saying there’s no more money to be made in optics, thermal management, and power systems… I think there is. But I look for outsized risk to reward opportunities and when every man and their dog is on board an investment theme…it tends to be a signal that the risk to reward is diminishing more than many think.

I ultimately wouldn’t be doing my job right if I was discussing the next theme to invest in as being packaging or optics.

That’s why I have started to research silver on a daily basis over the last month or two… all of which I’m going to concisely unpack into this article.

Introduction

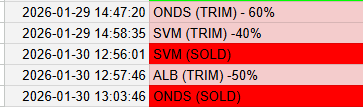

Paid subscribers will know that I have been bullish on silver for some time now. I invested in Silvercorp Metals (SVM) last year at ~$3 and sold it on the 30th of January ~$12.15.

Above is the timestamped alert of that from my Google Spreadsheet (soon to be updated to my web-app).

I invested in SVM more on the basis of a catch-up trade that I thought miners were undervalued compared to the underlying commodity (which I still deem to be very true) but my conviction on the underlying commodity (silver) was nowhere near as high as it is now.

So now I have:

Huge conviction in silver and its potential to head to +$150-$250 in the next 24 months.

A remaining conviction in silver miners being undervalued relative to the underlying commodity.

That creates a strong investment thesis.

Silver has always been thought of a precious metal or a monetary metal. One that acts as an inflation hedge or moves against the US Dollar. Whilst that may be true, it’s only a very small part of the silver thesis today.

Silver is an industrial metal with properties that no other metal has. And unsurprisingly… these properties are core to the entire AI trade.

When you combine the entire demand story which I’m going to explain with a supply picture that was already broken before AI entered the equation properly… and then you overlay that with equity valuations that remain historically depressed… you get a setup where the risk to reward seems very unique.

Contents

Silver Demand

Silver Supply

How high can silver go?

Why silver miners are still undervalued

The best silver miners to invest in

Silver Demand

Silver has the highest electrical conductivity of any element on earth… higher than copper, higher than gold. For most of the AI buildout early phase, that fact wasn’t too important because the near term bottlenecks were so important.

You needed more GPUs, more memory, faster networking, more power etc. It’s why stocks like:

AMKR is up 330% in the last year

BE is up 1,140% in the last year

But the phase we are entering next is different. It’s gradually becoming less and less about brute-force training and more becoming inference at scale and high efficiency. The economics begin to change quite a lot based on this.

The difference with inference is that the demand for continuous compute power is much more than in training. Tasks require thousands of loop-backs, multi-tasks working as part of a larger task, and above all continuous work.

The question becomes more about who can produce AI output at the lowest cost per unit with the least amount of energy wasted. At least, that’s what it is becoming. The first 3 years or so was brute force training and a race to build out AI. At some point efficiency had to become the more important part of the equation.

And that’s exactly why silver is becoming very important.

Silver sits inside all of the current bottlenecks:

You have connectors for AI data centers and high-voltage grid infrastructure.

You have switches for power electronics, circuit breakers, and grid distribution.

You have packaging for advanced semiconductors and microelectronics.

All of these components govern electric loss and thermal performance so as hardware scales, demand for these components scales with it. And subsequently when these components become more important, the makeup of these components (i.e. the materials…i.e. silver) becomes more scrutinized.

But there’s much more to the AI trade than just the data centers. AI is heading to the edge with robotics, drones, medical devices, smartphones etc. And the same logic that applies in the data centers applies to the edge…but its’s amplified at the edge.

Edge devices have to have smaller batteries meaning power efficiency becomes even more important. There’s no room in edge devices just to add another cooling devices if thermal management is the issue. In data centers, there’s always room and capital available to spend your way out of the problem. That is not the case at the edge. You can’t just add more components because weight matters so much.

Here’s where we can take it an extra step.

Silvers cost as a percentage of the total AI buildout is negligible. By that I mean, when you’re building $1 billion data centres, the line item for silver is barely noticed. The material items are the land, the power, the GPUs, the memory, the networking gear. It’s not the cost of the silver within those components.

That means if silver costs rise by 50% over the next 2-3 years, it will still remain an immaterial part of the AI buildout cost. And people will keep buying it because:

It’s so necessary.

It’s so cheap relative to everything else.

So, from the demand side, I put it simply like this:

Bullish on the AI data center buildout? You should be bullish on silver.

Bullish on the Edge AI thematic? You should be bullish on silver.

I haven’t discussed solar, EVs, and other electrification here in this article either. But those longstanding themes remain and are still bullish for silver.

Supply

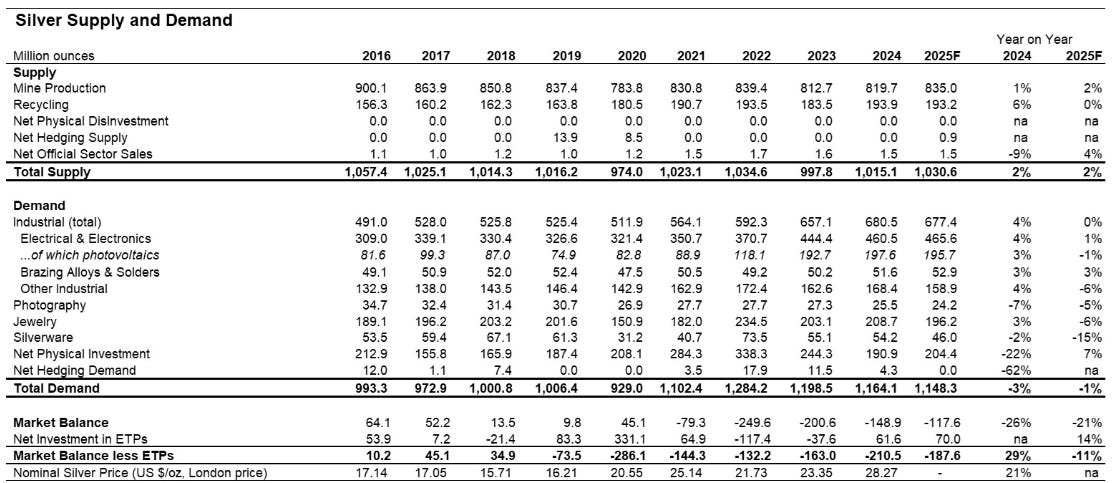

Before AI entered the equation, the silver market was already in a structural deficit. In 2024, the silver market was pressured because of solar demand, a grid upgrade, and general electrification. Today, those same pressures still apply but we also have the AI hardware demand as well.

There is currently ~148.9 million ouches of silver shortage which is the 4th consecutive years we have had a deficit. The main issue in supply is two fold:

Firstly, the vast majority of silver is mined as a byproduct of other extractions like lead, copper, and zinc. This simply means miners can’t just produce more silver. The silver output is fundamentally constricted by the output of copper, lead, and zinc.

Secondly, Mexico. Mexico supplies ~25% of global silver. For reference, that’s a much more concentrated source share than Saudi Arabia holds in oil.

Mexican output has been in a sustained mulit-year decline with no replacement capacity on the horizon. When your largest supplier is structurally shrinking and there is no pipeline of new projects ready to offset it, you do not have a cyclical supply problem. You have a long-term structural issue.

How high can silver go?

This is where the trade starts to get really interesting for me.

At the time of writing this, silver sits at $75.36. Most investors look at this and think that’s a 56% increase on 1980s and 2010 levels which may seem like a fair jump based on CPI and a modest increase in demand.

But it’s way off.

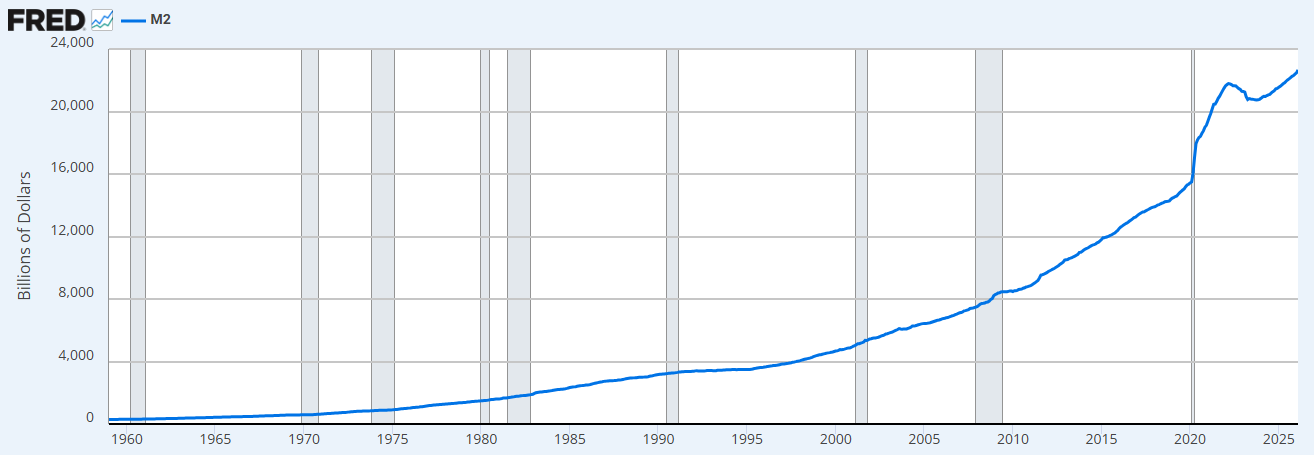

Silver is a monetary asset. It should not be measured against how consumer prices move. Instead, it should be measured against how much money exists to chase a fixed supply of metal…i.e. M2 money supply.

M2 money supply was $1.6 trillion in 1980. It stands at approximately $22.6 trillion today.

That’s a 14x increase.

So, if you apply that multiplier to the 1980 peak of $47, the money-supply adjusted equivalent is $658/oz today. You can look at different money supply aggregators but you’ll end up above $500/oz no matter how you look at it…compared to $75 today.

Let me be clear. This is not a price target. It’s a way of calibrating a bullish outcome and it’s a way of doing it fairly logically as well.

Adjusted for the dollars in existence, silver at $75 represents ~ a ninth of what $47 represented in 1980. Hopefully that gives you a gauge of the potential upside for the underlying commodity.

A reminder as well:

This article is actually going to get all tied up in the section below talking about the silver miners. The silver miners currently have a clear valuation gap between themselves and the underlying commodity…and I just put a logical way (though fairly bullish way) of the underlying commodity prices increasing over 8x from here.

Why Silver Miners Are Undervalued

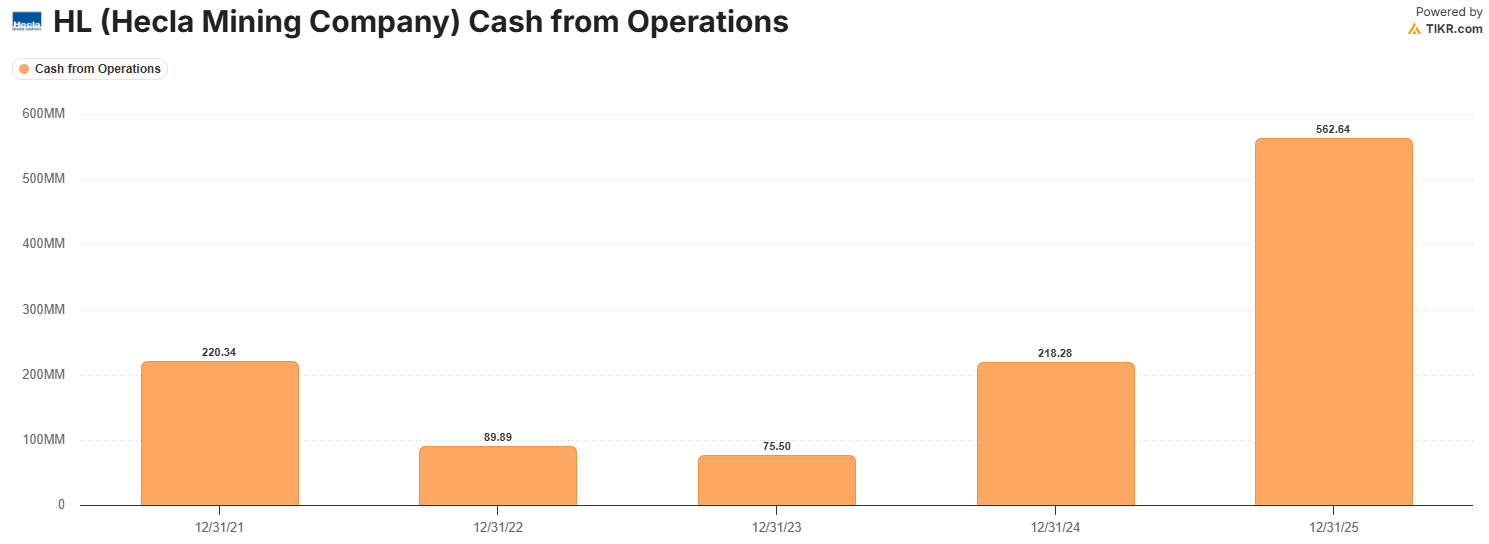

With silver prices above $75/oz the earnings profile of silver miners has changed fundamentally from 2-3 years ago.

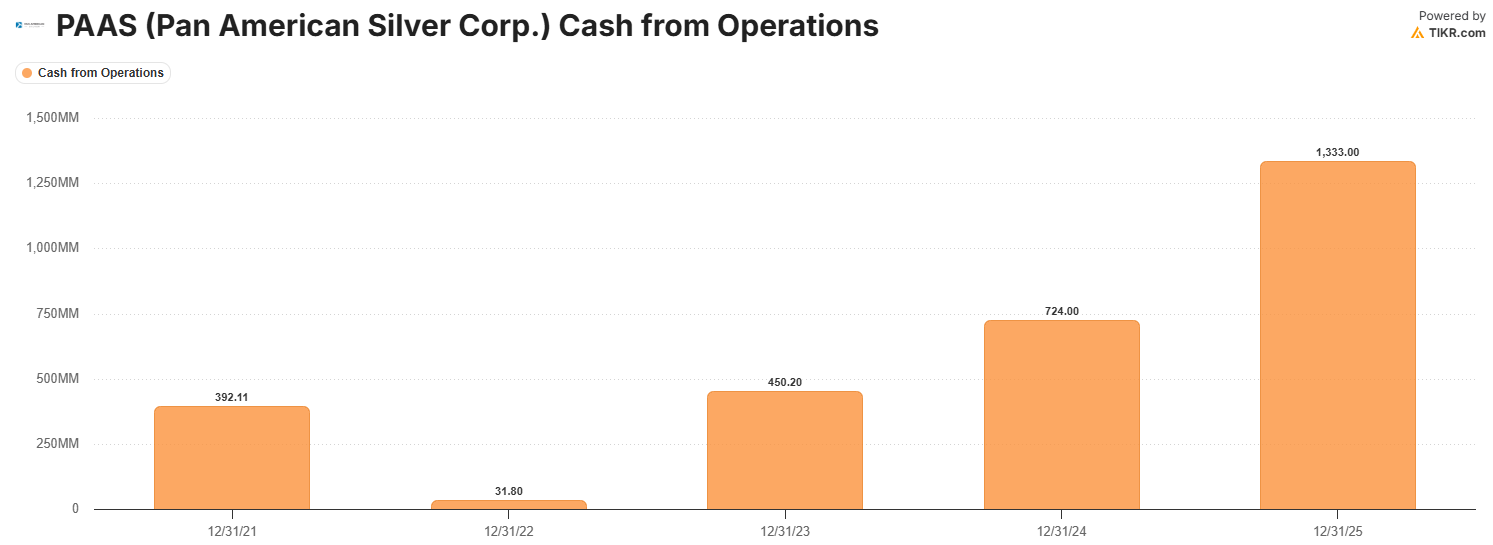

Here’s a couple examples of cash from operations for Hecla Mining (HL) and Pan American Silver Corp (PAAS).

PAAS’s cash from operations relative to FY23 has increased 196%.

Margins have increased from ~2.2% to 31.7% (PAAS) and 6.0% to 37.3% (HL).

It’s a completely different outlook for well operating mines.

Yet, despite this equity valuations have actually depressed since 2023. In 2023, PAAS traded above 22x NTM PE. Today it trades at 12.1x NTM PE. Its the market pricing silver miners as if the current earnings stories are temporary… or as if a reversion in silver prices is likely and therefore cash flows should be heavily discounted.

I personally disagree with all of that as I’ve made evident in this article.

For what it’s worth…if you adjust PAAS for example to measure how the stock is valued relative to the underlying commodity… you see PAAS near the very lows.

So, here’s how the situation can get resolved:

Unlikely: Silver prices break down sharply which would agree with the current multiples miners are trading at but disagree with my silver thesis entirely.

Likely: Equities re-rate upward to reflect the earnings power that these businesses have now silver is at $76/oz. This should only get stronger and stronger over time.

Given my thesis on the structural supply constraints and the expanding demand base, I think my likely scenario has ~80% probability of happening.

Which Silver Miners Are My Favorite?

The natural next question is of course how we play this theme. Here’s my plan: