The Chemical Level of AI: Early in The Cycle

The AI infrastructure buildout is the cycle we are currently in…and it could the cycle we’re in for some time. More energy is required, power grids need upgrading, more chips are needed, more complex chips are needed, more interconnect is needed. The demand is through the roof hence why power generation companies like BE have run+1,000%, or interconnect plays like have run +1,000%.

The opportunity I want to talk about today is beneath this. It’s the chemicals layer that makes almost all of this physical buildout possible.

The pipes, the cooling systems, the thermal infrastructure, the chemicals, the adhesives that make all of this possible.

How does advanced packaging work without the chemical systems? It doesn’t…Underfill adhesives mechanically bond the die to the substrate. Die-attach films then manage the heat path between these dies with tolerances measured in microns.

Photoresists and etching are a huge part of the modern fab process and these are predominantly chemical processes.

Where does the capital in the $6B deal between META and GLW go? Yes, optical figure is the core of this deal but many don’t realize that every inch of fibre is wrapped in a polymer system.

Every 800G transceiver is held together with adhesives. Every fab is plumbed with fluorpolymer pipes.

Thinking of the AI infrastructure buildout without the chemicals layer is an incomplete look.

No token can be created without a huge amount of optical fibre, polymer coatings, buffer tubes, fab piping, optical adhesives, thermal interface materials, and ultra-pure fluid etc.

But the most exciting part for an investor is that a lot of these stocks haven’t had their big move yet. Some of them have had a nice move from their lows in 2025 but relative to most “AI driven” stocks, chemical stocks haven’t had their time yet.

Entegris (ENTG) is trading only 30% above where it was 5 years ago.

Chemours (CC) is down compared to five years ago.

Although some of them feel a bit more expensive today, a lot of the target entry prices you’ll see below are fairly close to todays prices.

Before we get into the article…a quick note on my web-app. I am released a web-app that I have been developing for the last 2 months. It’s a good upgrade on my current spreadsheet. It contains:

Full portfolio

Baskets of stocks in all thematics

Data on all stocks

Deep dives

Timely research notes

And much more…

This makes the service I provide the most diversified out there? Looking for quick updates on how I’m managing my portfolio? You have it (with full transparency).

Looking for ways to generate ideas yourself with my assistance and research? You have it.

Give it a try. $24 a month. If you don’t find value in it…you leave.

A Concise Look into the Chemicals Thematic

I’ve edited this section a lot.

My first draft was detailed but long. I realized there’s probably not many of you out there who actually want to learn about the chemicals so I made this section about 50% shorter than it originally was.

I’ll go into a bit of detail… but my aim here is to give you an idea on the chemicals thematic without you having to read a 10-minute chemistry paper.

The money right now is in the industrial materials. It’s why miners has been such an important thematic for me to build positions in. We’ve had SREMF jump +50% this month and TMQ, COPX showing some strength. CTGO is also a new purchase for me too which is up nicely.

And it’s why chemicals is next on my radar. If you need interconnect, cooling, efficiency etc, you need the miners and you need the chemicals players.

For me, here’s the four key shifts happening at once which will lead to a chemicals bull market:

1. Fiber Optic Glass

Light moves far quicker than electricity through copper wires which is why optical fibre has quickly become the backbone of the long-distance interconnect. Copper simply can’t move data fast enough or efficiently enough within data centres or between data centres.

Here’s the chemical angle of this:

A fibre-optic is not just “glass”. It is a glass-polymer composite.

The core (the glass) is useless on its own so to make it deployable you coat the strand for protection, bundle those coated fibres into protective inner rubes, and sheathe the whole bundle in a flame-retardant outer jacket with gels and resins and alike.

For every dollar of glass, there is a dollar of specialty polymer pulled in beside it. And this is where names like Celanese, Chemours, Shin-Etsu, and Arkema operate.

It’s where the narrative around these names shifts from “diversified industrial” to an “AI infrastructure derivative”.

2. Fluoropolymer Pipes

A semiconductor fab is a factory where chips are made. Inside these fabs are miles of pipes that carry the chemistries needed to etch, clean, and pattern silicon wafers. These chemicals are highly corrosive acids and bases, aggressive solvents, abrasive slurries, and ultra-pure water that is cleaner than anything used even in the pharmaceutical industry.

Demand is now driving the largest semiconductor buildout in history. TSMC, Samsung, Intel, SK Hynix etc are racing to add 3nm nodes (3 billionths of a metre) onto a silicon wafer.

The smaller the node the more chemically demanding the process becomes. The content-per-wafer increases at smaller node sizes. This means that chemistry benefits from:

Smaller nodes

More wafers

Every chemistry operation that improves yield by even a fraction directly ties to revenue. Every new fab that comes online requires its own chemical supply infrastructure. Simple as that.

That’s why demand for companies like Chemours, Entegris, and Arkema is set to rise with AI.

3. Liquid Cooling

This is the simplest one.

Today’s AI chips draw ~700-1,200 watts each. And advanced packaging them into a single rack creates power densities that air conditioning cannot physically cool down enough.

This is why liquid cooling is the only way to manage it. Data centres now have coolants flowing through pipes attached directly to the chips (“direct to chip”) or in some cases data centres have entire servers submerged in non-conductive fluid (“immersion cooling”).

This creates a materials problem though. The coolant, the seals, and the gaskets all have to be chemically compatible with each other. There’s only a select few materials that qualify for this which are fluoropolymers, EPDM, silicone, and certain thermoplastics… exactly what Chemours, Arkema, Rogers, and Henkel produce.

4. Optical Transceivers

Back to optical fibre…A fibre on its own does nothing. It’s nothing without an optical transceiver at each end.

A transceiver is a small USB sized device that converts electrical signals from a switch or GPU into pulses of light heading down the fibre. On the other side it does the opposite (i.e. translates incoming light back into electricity).

Every fibre link in a data centre has one of these at each end which means transceiver volumes scale roughly at twice the rate of optical fibre. Here’s where it gets important though.

The speeds that these transceivers have to handle is climbing and will continue to climb. But the device itself isn’t getting any bigger to compensate. At those speeds the issue becomes:

Keeping the glass fibre and the silicon chip lined up perfectly because at that speed even slight misalignment scatters the light and the signal degrades.

Getting rid of the heat the chip throws off without room to add a larger heatsink.

Guess what solves both of these issues? Materials.

Optical adhesives are glues that bond glass to silicon holding the alignment.

Thermal interfact materials are compounds that move heat from optical chip to a heatsink, keeping the module from overheating itself at 1.6T speeds.

Henkel are one of the key players here.

Here’s Your Basket of Stocks:

How I’ve scored them:

1 = Revenue most directly tied to the AI buildout.

3 = Revenue least directly tied to the AI buildout.

Mini Deep Dives into My Favorites:

Celanese (CE) - AI Purity: 2

CE is one of the largest engineered materials and acetyl chain producers. The most relevant AI part of the company is Crastin PBT. It’s a thermoplastic the company explicitly markets as a top choice resin for high performance optical fibre cables. The rest of the business is in the traditional cyclical chemistry industry (engineered plastics for cars and industrial uses for example).

As hyperscalers continue to commit to data canter build out, demand for optical fibre accelerates and CE should remain one of the larger beneficiaries of this.

Valuation:

CE currently trades at $57 ($6.3B market cap) which means we’re trading ~8x 2026 expected EBITDA of $2.15B. CE currently trades in the mid range of its cycle ~8x EBITDA. Historically, this at the top of cycles this has been ~12.5x so if my assumption is correct and we’re heading into a chemicals cycle, then CE on FY27 EBITDA of $2.3B at 12.5x EBITDA gives you $28.75B EV.

If we subtract net debt of $9B you’re looking at a market cap of ~$20B or $181 share price on current shares outstanding.

That valuation target sits around this key resistance level. Probably a worthy trade to consider if you’re long chemicals and if you can wait for a nice entry around these moving average cluster, though not one in the basket I’d look for if I was looking for one that is going to be a lot more tied to AI demand.

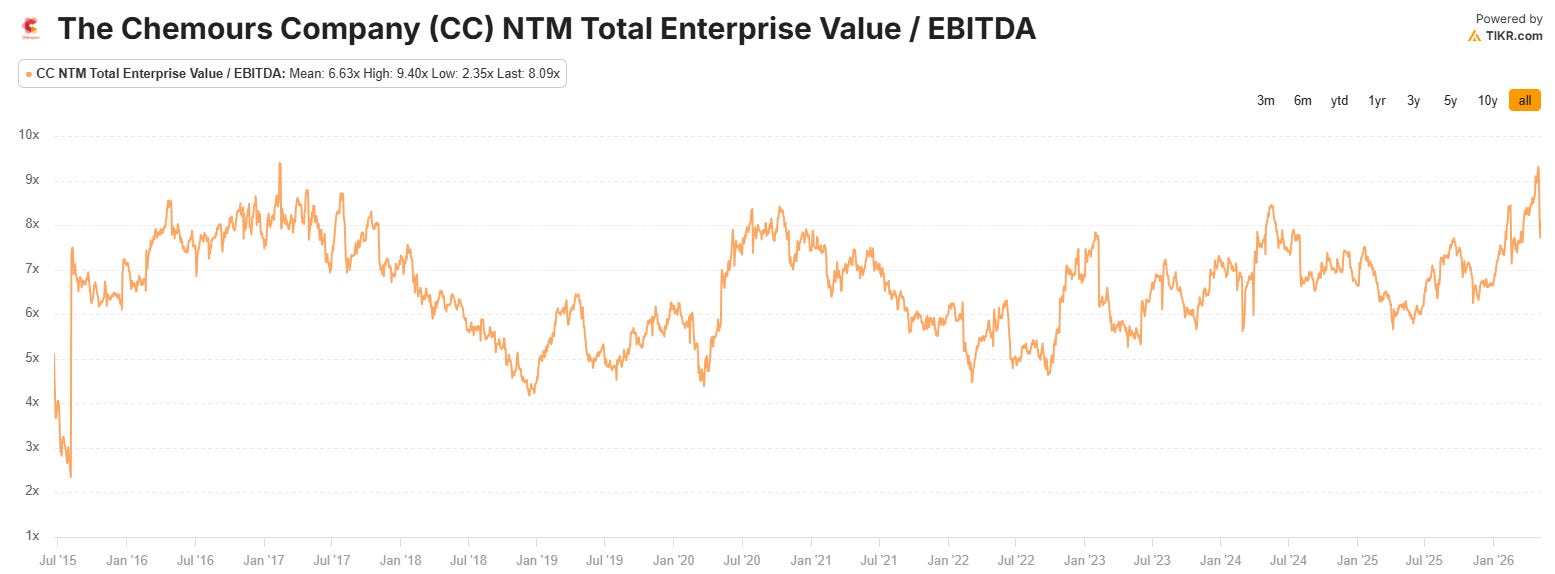

Chemours (CC) - AI Purity: 2

CC is a fluorpolymer company that handles:

Fab plumbing (pipes, valves, and tank linings to move corrosive chemicals and acids around fabs).

Cooling (heat transfer fluids sit directly within the direct-to-chip and immersion cooling systems). This is still in the very early days though with capacity coming online in late 2026 making this more of an emerging opportunity for CC.

The broader immersion cooling fluids market is growing at 24% CAGR to ~$1.6B in 2032. CC has potential here to build a meaningful share which, if they execute, should definitely re-rate the company further towards the more AI pure players in this basket and further away from CE trading in the 8-12x EBITDA range.

These two angles make CC a solid play on the physical AI infrastructure buildout. I see more upside here than a company like CE, but the AI demand story is not yet material enough.

Valuation:

I value CC very similarly to CE… on an EBITDA multiple basis. CC is also in a mid-cycle trading at $23 and slightly further extended away from MA’s relative to CE which has run less.

CC trades at 8x EBITDA and 14x EPS whilst set to grow EBITDA at 14% and grow EPS at 37%. These EPS growth rates are historically quite lumpy though.

EBITDA is expected to be between $800M and $900M in FY26 and $1B in FY27 so despite not being as pure as I’d like on the AI story yet, the growth rates are actually very reasonable for the multiples it trades at which to me gives a nice floor in the valuation.

The upside currently is a bit less certain, but the downside risk here is likely limited.

Element Solutions (ESI) - AI Purity: 1

ESI is a pure advanced packaging play… far more “AI Pure” than CC and CE above. It’s arguably as close as we get to a pure play infrastructure materials company that exists in the chemicals space.

It’s involved in the plating, solders, and metallization processes that hold modern AI accelerators and HBM memory stacks together.

Here’s the AI angle:

Semiconductor Solutions: Advanced packaging materials for leading-edge chips where AI GPU demand is the key driver.

Semiconductor Solutions: Thermal interface materials for high power consumption AI GPUs and CPUs.

Kuprion: This is a next-gen die-attach material that uses copper rather than silver sintering. It is currently a supply constrained segment of the business but ESI are investing into capacity to make this a material revenue generator in 2027-2028.

Circuitry Solutions: This is the chemistry involved to plate and etch the dense multilayer PCBs inside AI servers and networking gear that just generated a record quarterly revenue growing organically 17% YoY.

AI pure but pricey…see below: