03.16.2026: Ideas For The Upcoming Week

I deliberately delayed writing this article until as late as possible again as the war drags on.

It’s now week three of the war and I still can’t see much that evidences this is coming to an end. Just a few hours ago, Trump said he is considering putting boots on the ground to seize Iran’s Kharg Island. Here’s some more details on it:

This will likely only happen if tankers remain stuck in the Persian Gulf.

Kharg Island has 90% of Iran’s oil production.

Trump is working to assemble a coalition of countries to reopen the Strait of Hormuz.

All in all, it still appears that there’s tons of unknowns and it’s very difficult to gauge how close to the end we are.

One positive we have taken over the last few hours is BTC now up ~$74,000 again whilst oil prices are staying slightly below $100. It’s nothing to scream home about, but it could be a little positive to take into another volatile week. Maybe the worst is behind us.

It looks quite clear now we’re heading towards the 200 daily. The question now is just whether this is an October 2025 style pullback or a Feb-April 2025 style pullback.

Price action on the SPY looks pretty bad right now, but the macro reasons behind this could change in a day. On the QQQ, it looks like tech had it’s pullback and so far we’re holding structure here, but a break of this 595 and 200 daily MA here will be the key focus this week (again).

Before we get into my 3 ideas for the week, take a look at my March database and portfolio. You get:

Portfolio (real monetary amounts with 100% transparency)

Watchlist

Theme tracker

Valuation models

10+ themes with stocks per theme measured by valuation

Daily notes in the paid chat

1 video chart review per week

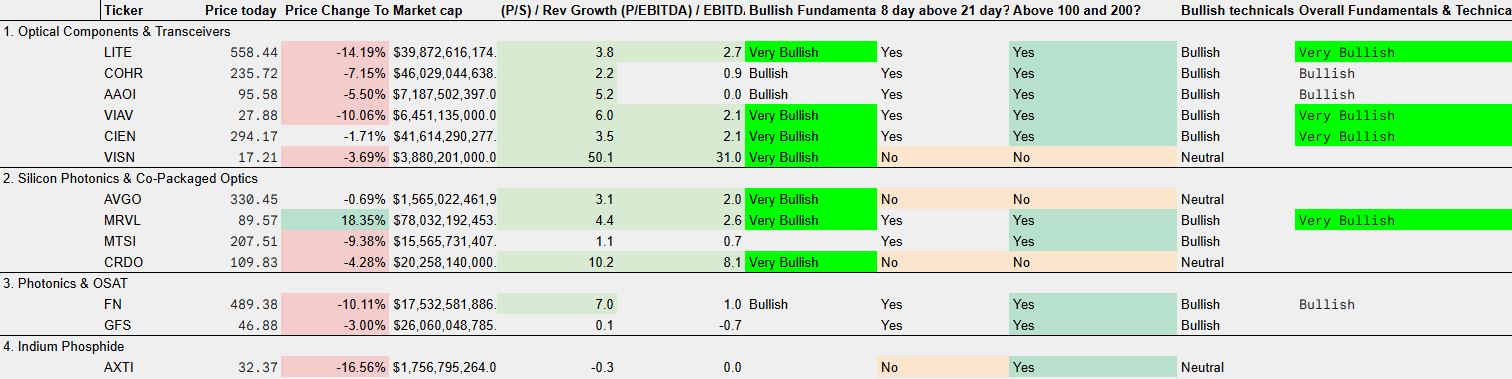

I also want to give an example of one of the many tabs within my portfolio. Here’s the optics tab:

I created this back in December 2025 before LITE and AAOI had their massive runs. It gives you a list of all the stocks within the theme measured by revenue and growth rates relative to multiples and also combines that with where the stock is trading technically vs key MA’s.

As you can see, LITE, VIAV, CIEN, and MRVL are still currently showing as very bullish. Outside of CRDO which I currently own, I think MRVL is my next favorite.

The reason I give access to all this data (and this tab is one of 10+ right now) is because I know we all invest in different ways. I offer complete transparency to my portfolio and my watchlist but I also offer you this extra benefit.

Stock picks are everywhere now. Having access to a nice quick screen is just an added benefit.

Another positive I am trying to take from the market at the moment is that we are seeing some pockets of strength here and there. It’s not a complete market sell off.

CRCL has moved +100% in a month.

HIMS is now +44% in a month.

BE is holding up ~530% over the last year.

LWLG has moved +77% in the last week.

Here’s a snippet from the spreadsheet. It shows prices per theme over the last week.

It seems like the last week still has very weak sentiment, still lots of selling pressure, but the market seems to be holding up a bit better than I perhaps expected for the most part given this. I feel like we’re edging towards a market where buying this dip is going to be the right play, but I need far more confirmation that a gut feeling like that.

I will continue to watch price action across a few key names and indexes and as soon as I see a bit more strength, I will likely start deploying some of my cash pile (~16% of portfolio).

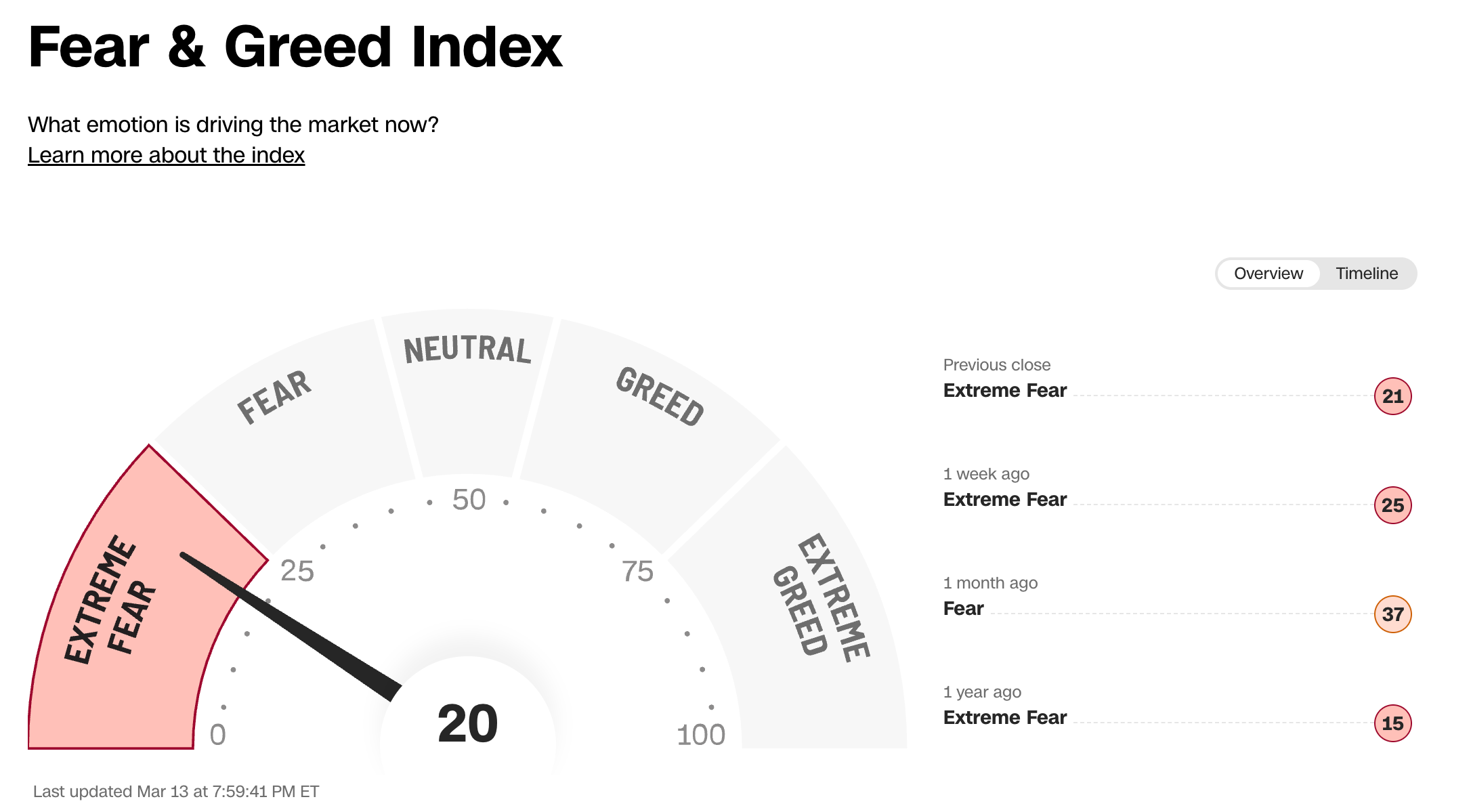

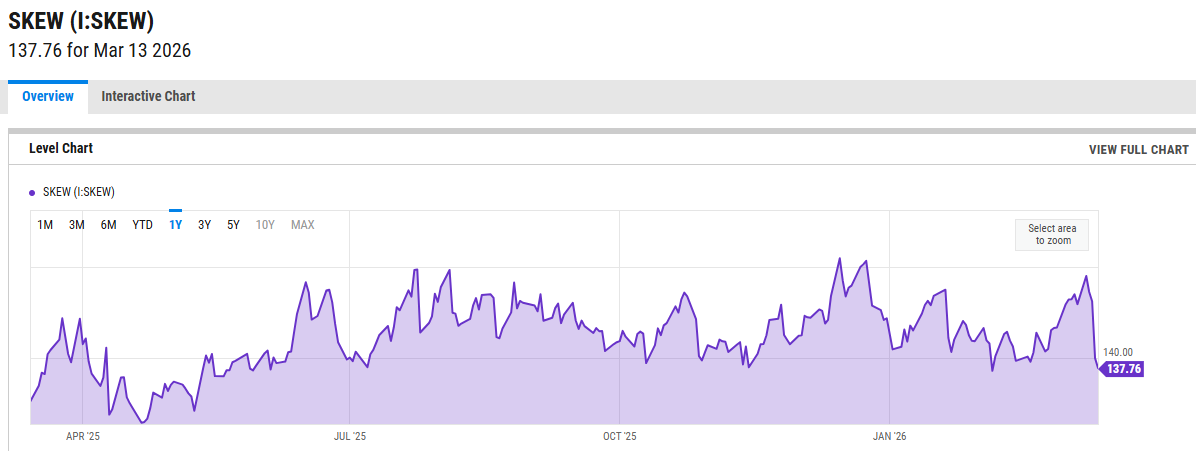

SKEW Index

This shows perceived risk has decreased slightly relative to last week. SKEW measures how deep out of the money puts are vs at the money options on the SPY. 137 is still on the higher end but it’s been +130 since April’s crash. Look at April’s bottom ~125. We’re nowhere near there but the perceived risk compared to 158 last week is another more positive sign to take.

We also have NVDA’s premier conference this week… NVDA GTC.

This tends to be the biggest AI conference of the year where all the leading minds come together to discuss the next wave of AI. Hopefully it acts as a little reminder to the market that we’re still in the very early days of this AI buildout.

Defensive/Lower Risk Idea

XLU & ITRI

I never like to “re-run” ideas in consecutive weeks, but doing so also shows my conviction in the theme. I’ve now chosen XLU (S&P 500 Utilities Sector ETF) as my more defensive play for 3 out of the last 4 weeks.

This is the 1 hour chart but you can see it’s so far held up very nicely despite wider market fear. That’s a nice sign. But XLU isn’t just a pick I like to manage volatility…it’s a pick I like to outperform for the next 2+ years and my individual pick on that is ITRI.

Paid subs will know that I’ve spoken about ITRI a lot recently but have only put a small starter position amount of money into the stock right now. This $90 level that I have charted out is extremely key to hold here.

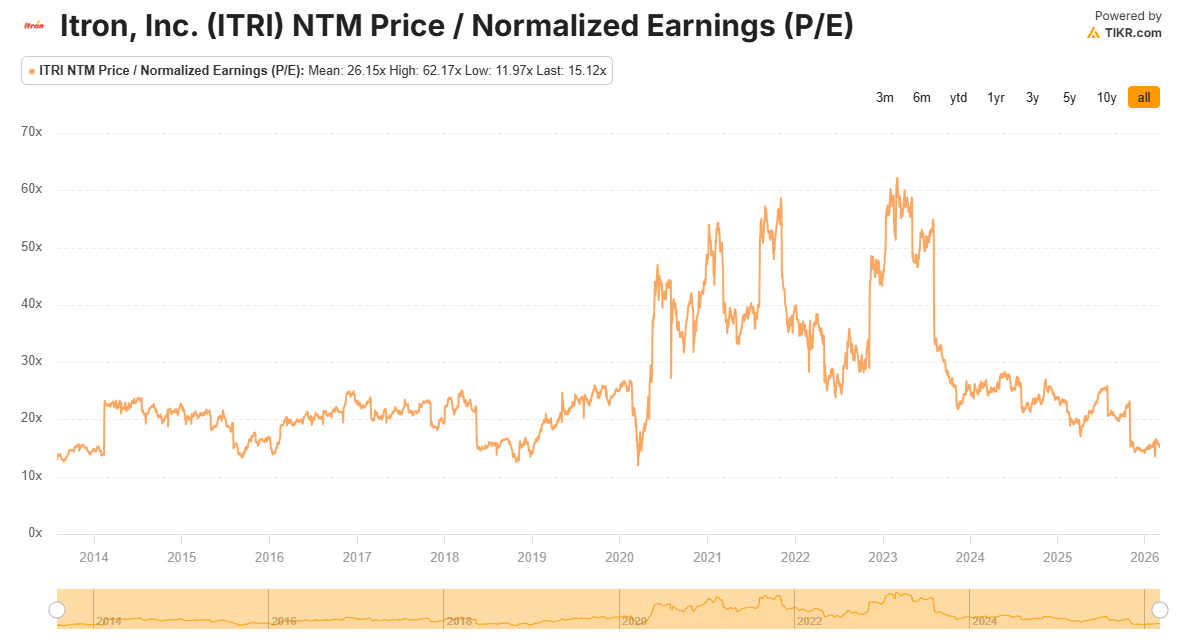

ITRI builds the smart meters and grid-edge hardware and software that lets utilities turn an aged, and overloaded grid into a data-driven network. There’s no modernisation of the grid without ITRI. It also now trades near it’s all-time low PE as the market focuses on the other key players like ETN, PWR, and HUBB. I think ITRI is next to run.

“This isn’t an if. It’s inevitable… It’s the way our customers need to cope with the world around them and the complexity of the environment that they operate in.” - ITRI CEO

“With more than $1 billion of durable Outcomes backlog, rapidly growing annual recurring revenue and expanding solutions for critical customer problems, Itron is well positioned for the multiyear grid build‑out in the years ahead.” - ITRO CEO

This isn’t the time for an ITRI deep dive…it’s more of an introductory idea. If ITRI becomes a top 10 play for me, then I will most definitely do a deep dive on the business.

In the meantime, I have my OUST deep dive coming out in the next 24 hours.

Neutral Risk

Last week I spoke about SOFI, HROW, and NBIS as my neutral risk ideas and I still think they’re arguably some of the best choices. I won’t repeat my narrative on them today but you can view it right here.

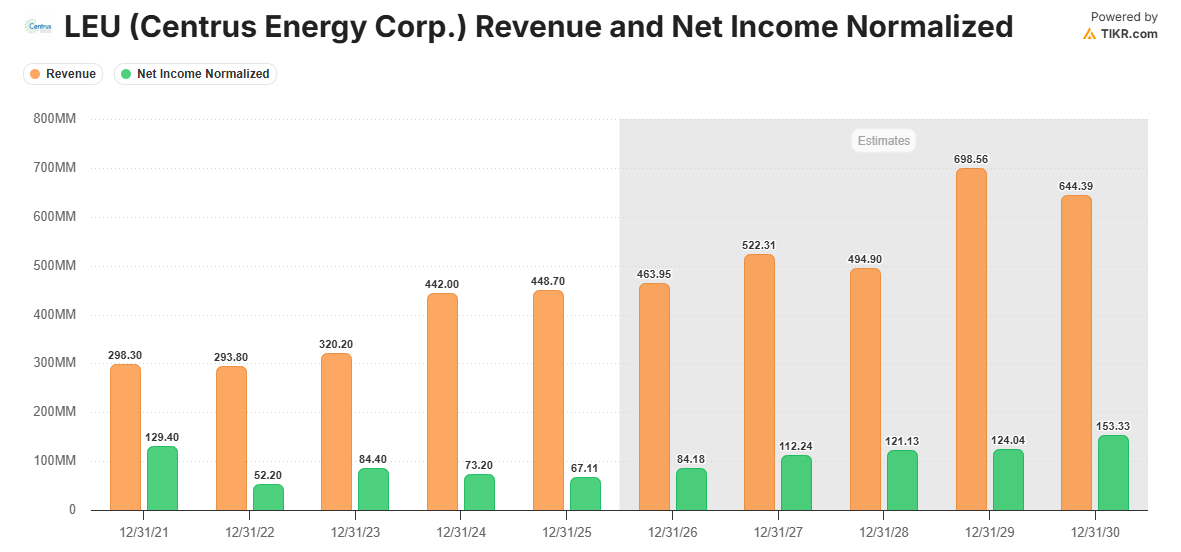

For today, I’ll discuss another idea to save repetition - LEU.

I personally have no position in LEU yet but it’s probably in my top 5 buys as soon as I start deploying cash. It remains still below the 200 and 100 daily MA’s but it has reclaimed the 21 daily.

People underestimate the importance of LEU. It’s effectively the missing middle of the Western nuclear value chain. It doesn’t mine uranium, but it enriches it, and it’s the only Western company that actively produces enriched uranium right now.

Most next gen reactors (SMR’s) which I am very bullish on through my position in NuScale (SMR) need enriched uranium between 5-20%. Most nuclear plants today use low-enriched uranium ~3%. Currently, the US relies heavily on Russia for enriched uranium but this isn’t sustainable at all in the nuclear cycle we’re entering.

LEU currently sits at $2.3B backlog and a multi-billion dollar enrichment expansion plan targeting commercial enriched uranium. Add on the fact that the government is committing $2.7B in domestic enrichment explicitly aimed at reducing dependency on Russia, and you have quite a clear long term bull case.

The next step is just figuring out if there’s value or not which is hard for a company like LEU.

Here’s the way I’m looking at this valuation at $209:

Mid case revenue estimates are ~$650M in revenue in FY28 with $121M in net income. I know the above chart gives $495 in revenue, but I think that’s a data issue and a clear anomaly. LEU currently trades at 59x NTM PE which sounds pricey but when you’re growing net income ~28%, with long-dated contracts, US government support, and a huge backlog it doesn’t seem too high.

FWIW, CEG has historically traded at ~30x NTM PE and I think LEU should trade at a higher multiple based on:

CEG’s economics rely on power prices, capacity auctions, and regulatory decisions. It’s why we’ve seen a massive sell off in CEG lately.

LEU sells the specialized fuel into a capacity constrained market where there’s very few (if any) alternatives. That is a moat that deserves a higher PE. LEU has more pricing power and less reliance on commodity prices.

So, if we conservatively give LUE a 35-40x PE multiple on $120M in net income you have ~$4.8B valuation in FY28 which is higher than today and in my opinion that is based on a very conservative PE multiple. Let’s see. I am still not an owner of LEU, but I likely will be quite soon.

Higher Risk

Last week I spoke about IRDM and OUST. OUST I currently own… IRDM I am hoping to own but it’s at a very key technical level that I am watching closely.

Today, I’m adding one more stock in there that I think is great value today.