HIMS vs AMZN - Everything You Need To Know

HIMS AMZN

Hi there👋

A little different to my normal email but I just wanted to come on and comment on the HIMS AMZN news.

Two weeks ago HIMS dropped about 20% following the news that AMZN were upping their investment into telehealth services (something that we knew already and was already a risk). Since then, the market has recovered fully to $31. I actually started drafting this article as soon as HIMS dropped and really wanted to get it posted last week but life got in the way and I only just managed to finish it.

Anyway, I wanted to write a quick article explaining my viewpoint on this news and why I’m still extremely bullish on the future of HIMS👇

Introduction

Let me start by saying AMZN has attempted to enter into the telehealth industry for a long time and they’ve had very little success. Too many people think that just because AMZN is one of the biggest companies in the world with billions of dollars at their disposal to invest means that they’ll be successful in any industry they enter. This is not true.

AMZN have failed to enter the smart phone market in 2014 which tried to compete with Apple.

Amazon tried to compete with Groupon but failed.

Amazon tried to compete with Expedia and Booking. com but failed in 2015.

Amazon have failed with their Game Studios venture.

Amazon failed to compete with Pinterest and Instagram in 2017 with Spark.

Amazon are still struggling to compete in China against competitors like BABA and JD.

Amazon Halo was meant to compete with Fitbit and Apple watch in 2020, but failed.

Simply, people do not view AMZN as their go-to place for healthcare services and I don’t expect this to change.

Meanwhile, HIMS has invested huge amounts into their sole purpose of reinventing healthcare. They’ve managed to strike a perfect balance between size and efficiency, and a personal touch to healthcare which AMZN will not be able to replicate.

Whether bears question the HIMS moat or not, they’re growing subscribers at 42% annually and increasing order value. This would not happen without a strong moat and a dominant (50%) position in the telehealth market.

Business Models

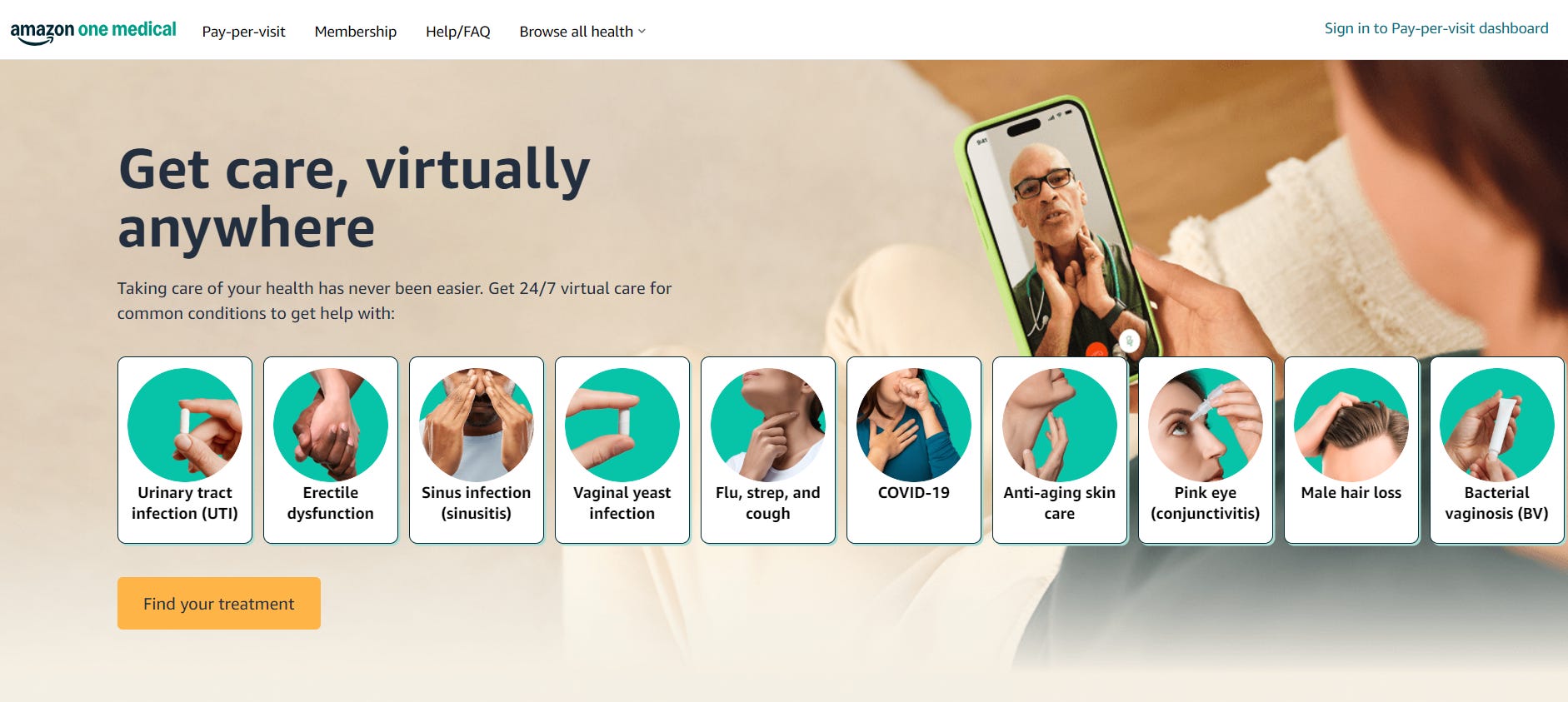

Here’s the AMZN model in a nutshell:

Consumers must have a prime membership to be eligible for telehealth services.

Consumers must pay $29 for messaging a physician and $49 for a video call with a physician on top of the prime membership and other costs.

Very limited customer-centric experience. It’s very similar to a normal AMZN e-commerce purchase where you go online and simply just purchase a good. This is beneficial for those seeking very quick remedies, but people don’t tend to make these random quick purchases with their health. They want education, care, and support. AMZN does not offer that.

Very strong delivery and logistics services meaning patients get drugs and treatments very quickly post purchase. AMZN bulls will argue that this is a big advantage but I don’t see it. If you’re receiving treatments on a monthly (or weekly) basis, you’ll still get them on a monthly or weekly basis with AMZN or HIMS. HIMS also have a 24 hour turnaround from treatment approval to prescription release. This “advantage” isn’t such an advantage here.

Here’s the HIMS model in a nutshell:

All consultations (messaging and video calls) are included in the monthly subscription.

The platform includes educational tools to assist patients with decisions.

Regular follow-ups with physicians are normal.

Physicians have access to tons of data and information to make informed, personalized choices on the best method of treatment.

Where do AMZN & HIMS even compete?

Before I build my case on why HIMS shouldn’t be threatened by AMZN, let’s just touch on exactly where they compete…which is quite a lot.

AMZN offerings (I highlighted in bold those that HIMS also offer):

Erectile dysfunction

Other sexual health issues

Skin care

Hair loss

Flu, strep, or cough

HIMS offerings (I highlighted in bold those that AMZN also offer):

Weight loss

Hair loss

Sexual health

Mental health

Skin care

Advantage: HIMS

A huge difference lies in HIMS offerings in weight loss (and mental health but weight loss is a key driver for HIMS at the moment). HIMS currently offers both an oral solution and a compounded version of semaglutide which is a GLP-1 medication. In a recent article 👇

I spoke about the risks and uncertainties around GLP-1 but also touched on the positives and high growth prospects. AMZN aren’t competing here meaning HIMS have a huge competitive advantage in the wide range of offerings. Don’t forget that a lot of new product offerings are coming for HIMS too.

So HIMS and AMZN currently compete in hair loss, sexual health, and skin care. But is it really a competition?

AMZN offer generic drugs that are widely available in pharmacies and they come in standard dosages.

HIMS offer compounded medications that are less widely available, and that provide a very tailored approach to customers health.

For example, HIMS physicians can:

Offer tablets, chewables, creams depending on patient preferences.

Offer different dosages to ensure side effects are limited.

Offer different drug combinations to improve the efficiency of treatment.

Offer multi-condition products to tackle different conditions at the same time.

It’d be naive to suggest that AMZN will never offer compounded medications with the huge investment they have. However, I don’t think they’ll do this unless they start to see some momentum in their telehealth business.

To conclude this section, consumers wanting quick generic drugs may find AMZN slightly more useful. However, the HIMS competitive advantage lies in the fact that they can provide niche treatment solutions tailored to individuals.

This is a huge advantage and essentially makes HIMS and AMZN compete in different areas.

Brand

I touched on this in my introduction.

Consumers care about their health, hence why individuals will choose a niche, specialized, healthcare focused company over a AMZN which resonates with speed and convenience.

How will consumers begin to trust AMZN who have next to no establishment in the healthcare niche?

AMZN are a logistically savvy, tech savvy, e-commerce giant, with a huge portfolio in various industries. HIMS are a specialized healthcare expert. I know which one I’d choose.

This allows HIMS to have a huge advantage in their marketing efficiency. AMZN’s telehealth marketing has to firstly convince consumers that they can even provide good healthcare. HIMS consumers already know this.

Again, I’d be naive to say that this viewpoint I hold is followed by everyone as I’m sure there’s some very price-sensitive consumers out there who may decide speed and price is advantageous to quality. This is essentially why AMZN has turned into one of the largest companies in the world.

But healthcare is different and I’m confident in saying that more individuals will chose quality treatment over convenience.

It’s not a winner-takes all market

I hate to admit, but of course I can be wrong here. Competition, mainly from AMZN has been one of the main bear cases for HIMS for years.

So let’s say I am wrong and AMZN take some market share and become a strong competitor in the telehealth market.

The US telehealth market is set to be valued between $160 billion and $420 billion by 2030 depending on different research firms. $420 billion seems very high to me and I’m more on the lower side which would suggest approximately a 19% CAGR.

This huge size means it’s extremely unlikely that there will be one dominant player. HIMS and AMZN can easily co-exist in their respective niches and both still perform extremely well.

The other point that I think is necessary to make is that if AMZN are successful in the telehealth market, it is very likely that the adoption of telehealth will accelerate simply because AMZN are one of the most influential companies in the world. This would benefit HIMS if they manage to keep their respective share and hold a competitive advantage.

My Take

AMZN become a risk

There’s 2 ways that I see AMZN actually disrupting the HIMS business:

I am wrong about consumers and they actually favor a cheaper price generic drug. AMZN win here as they have the ability to leverage their huge logistics capabilities and vast infrastructure. They can price HIMS out of business if it comes to it. Likely? For me, not at all. As I said, consumers don’t value price as much when it comes to their health. They value good care and good quality.

AMZN acquire a compounding pharmacy to then offer personalized solutions and compete with HIMS everywhere. Likely? Perhaps more likely yes but it will take time.

AMZN/HIMS co-exist

As I said before, the telehealth market is huge and HIMS and AMZN could easily co-exist in their respective niches. AMZN will offer generic drugs and dominate there and HIMS will offer personalized solutions and dominate there.

Likely? Yes.

AMZN fail to disrupt HIMS

I think the other likely scenario is that AMZN fail to affect HIMS at all (as price action this week has perhaps suggested). Whatever people do believe, it’s difficult to deny that HIMS have a moat. It’s not one of the strongest moats in the world, but it’s a moat that a company like AMZN couldn’t just replicate in a year.

Years of clinical data

Years of clinical trials

Years of building a team

Years of personalization through HIMS AI tools

Years of data

AMZN can for sure do this, but in the time they take to do this, HIMS will continue pushing ahead and compounding their successes so far.

It’s far more likely that AMZN don’t compete with HIMS here directly.

Conclusion

I hope this article explained logically why AMZN will not destroy HIMS. AMZN may well invest massively into telehealth but that doesn’t change the fact that they will really struggle to disrupt HIMS.

The two most likely scenarios are:

HIMS and AMZN co-exist in their respective niches within telehealth.

AMZN does not disrupt HIMS at all.

Both scenarios will mean HIMS will continue to grow and continue to become a powerhouse in this rapidly growing market.

That’s it for the day

I hope you loved this article. Please do leave some feedback for me.

Please subscribe to my newsletter where I provide investors with all the tools to outperform the market, and retire well before you’re 65. You can also follow me on X.