SEALSQ (LAES): A Mini Deep Dive

The high risk high reward quantum play?

Introduction & Thoughts on Quantum in General

I’ve tracked quantum for ~4 years now. I wrote my quantum ecosystem deep dive here where I first introduced LAES.

The Quantum Computing Race: How to Invest

I’ve tracked quantum for a while but never fully enough to gain an edge relative to other themes I’m focused on. I never invested in the IONQ, RGTI, QBTS boom etc and I had no regret on that.

I’ve been very back and forth on the topic over that time jumping from it being a distant reality to what I now deem it to be on the verge of potential, and material, breakthroughs.

Over the last few months, we’ve seen more and more news come out on quantum and all of that news has labelled quantum to me as now being a serious technology that is being battled out between US and China.

Governments are now doubling down their quantum investments by committing huge sums of money into labs and foundries. 2026 alone has seen:

May 21 Commerce CHIPS package

China’s accelerated funding

France’s accelerated funding

Trump’s June 22nd Executive Orders

Migration to post-quantum cryptography

If we take a step back, I think it’s important to understand the following:

Peter Lynch: “In stocks, the upside is always greater than the downside. A stock can only go down 100% but it can go up 1000%.”

I don’t always have this exact mindset with stocks. But it’s the mindset I have taken with LAES.

Big picture here’s where quantum is right now:

McKinsey is estimating quantum could create between $1.3 to $2.7 trillion in economic value over the next 10 years.

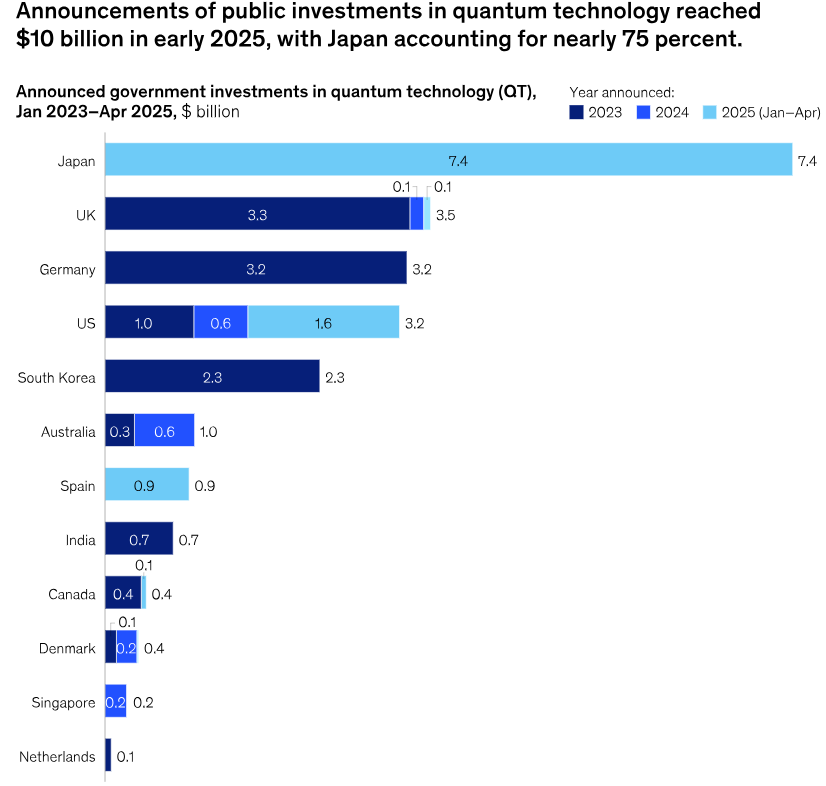

Quantum is rapidly becoming a national security priority. We’ve seen $2 billion investments into quantum companies in 2026 across a range of different quantum architectures.

Now China and US are arguably on a level playing field technologically now…the next big win could come from quantum?

China are currently investing ~$17 billion into quantum (more than the US) and so far it’s paying off. They’ve announced the Hanyuan-2 (world's first dual-core quantum computer) and Jiuzhang 4.0 (most powerful photonic quantum computer) in 2026.

Investment in Europe is also growing with France committing $1 billion in 2026 alone, the UK investing $500 million through to 2030, and Germany investing ~$3.5 billion through to 2032.

The economic value created by quantum will be seen most across chemistry, materials science, and drug discovery. I wrote about the drug discovery angle in my recent article.

In short, it’s one of those very early stage technologies, but out of everything, I think the upside is the most substantial relative to today’s levels (maybe biotech is the other sector with similar upside).

A huge number of challenges remain though. The technology is extremely complex, investment is still very early, supply chains are already struggling, and there’s a clear shortage of critical materials.

But if you’re a high growth investor looking for a higher risk bet, then the quantum market should be on your radar.

Company Name: SealSq

Ticker: LAES

Market Cap: $692M

Headquarters: Geneva, Switzerland

CEO: Carlos Moreira

Before we move on I just want to show you my paid service. I’m building a fully functional web-app / database / research website all in one go. You get:

Daily market commentary

My personal portfolio and watchlist

Weekly thematic commentary

New Ideas

Weekly Videos

All for ease on a nicely designed web-app.

LAES Introduction

LAES spun out from WISeKey (WKEY) which is a Swiss cybersecurity firm. Today, it’s doing something that very very companies in the world can do:

It has built a chip with post-quantum encryption and it’s further along the path to getting certified than any of its competitors have publicly disclosed.

The timing of what LAES is building is key to everything. On June 22nd 2026, Trump signed two executive orders (EOs) mandating that all federal civilian agencies and their contractors migrate post-quantum cryptography by 2030. The previous deadline was 2035 so the whole narrative around post-quantum cryptography changed in an instance and stocks like LAES became far more important overnight.

Post Quantum Cryptography Market

What does “Q-Day” even mean?

Nearly all encryption securing everything on the internet relies on maths. It relies on a math problem that is ultimately too hard to solve in a reasonable timeframe.

Quantum computers break this bet entirely because they can use Shor’s algorithm to solve these math problems in enough time. That makes the encryption secure against classical computers but not secure against a quantum computer running Shor’s algorithm.

“Q-Day” is the term for the date at which a quantum computer that is powerful enough to execute Shor’s algorithm in sufficient time.

Previously this date was ~15+ years away, but today post Google’s March 2026 whitepaper signalling Shor’s algorithm can run with fewer than 10,000 qubits, we’re far close than 15 years.

It’s looking more likely to be the end of this decade.

The main issue however is that full PQC migration (enterprises’s timelines from nothing to protecting themselves against this quantum) is ~12 years. So if “Q-Day” arrives in the next 3-7 years, organizations that haven’t started yet are structurally very late.

This means the threat timeline is now regulatory driven and deadline driven rather than technologically driven. Customers will begin buying PQC hardware not because quantum computers exist today but because:

Governments will mandate this.

The migration process may take years regardless.

Harvest-now-decrypt-later ultimately means waiting is not safe even if “Q-Day” is 10+ years away anyway.

Market Size

This is a difficult one to gauge because research varies and there’s a lot of companies operating in sub-niches different to what LAES does.

Here’s my best estimate:

The embedded security chip market: This is where LAES’s legacy products ultimately operate and this market is forecast to be ~$10 billion by 2028.

The PQC hardware market: This includes secure semiconductors, TPMs, and HSMs (Hardware Security Module) implementing PQC algorithms in certified hardware. There is the most variety in this estimate because the market is very nascent and because its currently gated by certifications.

Estimates put this market ~$2.5 billion (but ranges up to $20 billion).

Take this with a pinch of salt because customers (governments, defense, financial services etc) legally cannot deploy uncertified PQC hardware in production systems yet so gauging the market size is almost an impossible job today.

The market will not grow linearly at all. And this is another reason why LAES is a riskier investment today. But as regulatory deadlines approach and certified products become available, expect this $2.5 billion figure to jump considerably.

The Certification Issue

As I just touched on, regulated sector customers cannot legally deploy PQC hardware in production systems until that hardware holds specific certifications, regardless of how technically capable the product is today.

There are two key certifications:

FIPS 140-3: This validates that a cryptographic module meets specific security requirements. LAES is currently pursuing Level 3 (out of 4). Just like getting FDA approval, this process costs millions and takes between 12-24 months from submission.

EAL5+: Level 5+ is an international security standard requirement for hardware targeting defense, intelligence, and critical infrastructure applications. It is one of the most demanding certification processes in existence, typically taking 2-4 years and costing ~$5 million pre product. LAES currently has four variants in the pipeline that each require their own independent evaluation. LAES has already passed two of the most demanding parts of the process (fault injection and side-channel attack testing).

I’ll dive into this more later, but this matters a lot. It’s evidence that the path from "$200M pipeline”, or “interested customer”, or “115 customers actively testing” to customers actually paying in volume is extremely challenging.

This is the main point I want to get across in this LAES deep dive.

The upside is high. The downside is also very clear and right now it’s definitely considered a bet on things going right.

The other important note is that LAES currently has a certification target of Q4 2026. If they miss this target because of delayed or failed certification, then the risks of missing CNSA 2.0 January 2027 new-acquisition deadline become a real risk.

Recent News:

On March 30th, Google Quantum AI released a document co-authored with Stanford and the Ethereum Foundation establishing that breaking cryptography (the security behind Bitcoin and Ethereum) requires fewer than 500,000 physical qubits.

That’s a 20x reduction from prior estimates.

And the CEO of LAES, Carlos Moreira referenced this in their earnings call:

“Remember last year, in January last year, we were still thinking that quantum computers will be only able to break RSA triple desk. In 30 years’ time, this was reduced to 10. And now Google announced yesterday they are actually dividing that by 10.”

“Now quantum companies are also expanding faster than their qubits generation. The company we have invested and the ones that we are in the process of investing in, they are already able to generate between 10 and 100 qubits. And some of them, they are predicting to be able to reach the 500 qubits, which is what Google says that will actually be enough to break cryptocurrencies.”

The implication is that the algorithmic side of the threat is compressing fast. Faster than the hardware side of quantum anyway.

And then on June 22, 2026, Trump signed:

EO 14411: An effort to produce a scientifically relevant quantum computer within five years, quantum sensors, and networks.

EO 14409: The PQC mandate. Four binding deadlines:

NIST pilot project complete by December 31, 2027.

Federal civilian agencies transition high-value assets for key establishment to PQC by December 31, 2030.

Federal contractors under covered procurement rules meet the same standards by the end of 2030.

Digital signature systems migrate to PQC by December 31, 2031.

Here’s what it actually means:

I think this news gives us a few ideas:

The timelines are still quite a way down the road so expecting these stocks to move considerably in the short term is arguably naive…but it’s a great time now to learn and start to slowly build positions. NIST pilot project by 2027 creates a near-term procurement and testing cycle meaning vendors who can demonstrate compliant products by then will have a structural advantage.

The orders do not name, reference, or contract with LAES in any way. There is no plans to support specific quantum companies over the likes of IBM, GlobalFoundries, or KeysSight for example. That’s something to be aware of and to be careful about.

Despite point 2 above, direct funding recipients are not LAES competitors in the PQC hardware market. IBM and GFS are quantum computing hardware builders, but not PQC hardware builders. That’s an important distinction and not a bear case for LAES.

Despite point 3 above, there is still a lot of competition in the PQC market. American Binary is a pure-play PCQ software company with partnerships with players like Oracle. It’s operating in the exact regulatory environment LAES is targeting but just on the software side. Although they compete in slightly different areas of the market, it’s an illustration that there are a lot of well-credentialed players in the PCQ market.

The “Made in USA” angle got more valuable. These executive orders prioritize domestic supply chains so LAES’s plan to operate mainly on US soil aligns. Those companies that can credibly say “designed, personalized, and certified in the United States” will likely be very big beneficiaries as we head towards the 2030 deadline.

Just a quick note:

I personally use TrendSpider at minimum 3-4 hours per day. I think it’s got the best charting platform in the market, the best AI in the market (SideKick), and very good fundamental analysis.

There’s a July 4th discount happening this coming week if you’d like to sign up. You have up to 45% off, $355 in free bonus upgrades, and the launch of the new Sidekick Portfolio Agent.

Product Portfolio

LAES’s products sit across two categories:

Secure elements

Trusted platform modules

QS7001 - The Secure Element

This is LAES’s flagship post-quantum secure element.

A secure element is a tamper-resistant chip that sits inside a device (a smart meter, an IoT sensor, a medical device, an EV charging station).

It handles all cryptographic operations such as storing keys, authenticating the device, encrypting communications. The simplest way to explain it like a locked vault inside a device.

The differentiation for QS7001 is that it implements ML-KEM and ML-DSA - these are two NIST-standardised post-quantum encryption algorithms. This isn’t a software add-on. It’s directly into the silicon.

QVault TPM

This is a different product for a different type of customer.

A TPM is a security chip that sits inside a computer and acts as the hardware identity card. Every time the device boots up, the TPM checks that nothing has been tampered with, stores the encryption keys that protects the devices data, and provides a verifiable proof to any network it connects to that the device is what it claims to be.

The simplest way I think about it:

QS7001 goes inside devices. TPM’s go inside computers. This means the QS7001 is designed for manufacturers building smart meters, drones, medical devices, sensors etc… products that need a secure identity chip embedded inside them.

The TPM is designed for the computing infrastructure that runs the world - servers in data centres, PCs etc.

The addressable market is therefore slightly different but the underlying mission is the same: post-quantum security baked directly into the hardware.

PKI & Trust Services

PKI and Trust services currently represents just 2% of LAES’s total revenue - approximately $0.4 million in FY25. Most people skip past that but there’s big potential here.

Here’s what PKI actually is and how it connects to everything LAES is building.

Every chip LAES sells needs a digital certificate. That certificate doesn’t just get issued and then forgotten. It needs to be renewed, managed, and verified throughout the chips life span.

It is unlikely to be the main revenue driver for LAES, but even a $0.10 per chip at a scale of 100 million chips per year (the Kaynes JV in India is targeting 300 million chips at scale) is ~$10 million per year in potential revenue. If you look at my model below, you’ll see the potential of this segment.

Competition

This is arguably the most important part of this article I think because it sets the picture for the small cap, high growth stock vs the established well-resourced semiconductor companies.

I’ll break it down via tiers:

Large Cap Players

Infineon (IFNNY): This is the most direct competitor to LAES core TPM market. IFNNY’s TPM is already designed into hundreds of millions of devices across PCs, servers, industrial systems, and network infrastructure - and it’s next gen chip will include post quantum encryption as an upgrade path for existing customers.

That’s the key danger for LAES. IFNNY customers won’t need to switch vendors or go through a new design process, or change their hardware supplier to access post-quantum security. That’s a huge competitive advantage.

But IFNNY currently has no post-quantum chip that is actually available so they’re far behind LAES in that regard. We have no public knowledge of timeline or launch data.

NXP Semiconductors (NXPI): NXPI product is EdgeLock which will compete with LAES’s QS7001 but just like IFNNY the timeline is behind LAES with no publicly disclosed timeline.

It’s a very similar story to IFNNY in that NXPI has an enormous customer base with existing relationships meaning its post-quantum version is just an evolution of a product rather than an entirely new product.

Microchip Technology (MCHP): MCHP announced its entry into post-quantum hardware security on April 28th 2026 with a direct competitor product to LAES’s TPM. It’s probably the furthest ahead but again has no publicly disclosed certification timeline at all so gauging that is much harder to tell.

Ultimately, every company here is trying to build a chip with post-quantum encryption standards baked in and get it certified by federal regulators.

Right now, no company has achieved this.

To put it as simply as I can - LAES appears the furthest ahead at the moment in terms of product and certification (at least from what has been publicly disclosed) so they have a first mover advantage. But MCHP, IFNNY, and NXPI all have the capital and manpower to get jobs far quicker.

They also have the existing customer relationships so first mover advantage actually means a lot less for them.

An interesting battle of the safer compounders vs the small cap that needs to meet the strict deadlines to stand any chance in the market.

Smaller Cap Players

BTQ Technologies (BTQ): BTQ is the most direct pre-revenue hardware competitor to LAES in the small cap space. From my understanding, certifications are ~12-18 months behind where LAES is today in terms of actually delivering chips to customers.

This makes the timeline risk of meeting certification deadlines far trickier for BTQ.

Valuation

Given everything I’ve told you above, valuing a company like this is extremely challenging.

It’s similar to valuing an early stage biotech seeking FDA approval.

But I think the best thing I can do here is model out a bull, base, and bear case over the next 6-8 years.

You can see my valuation models here below. It’s a Google Doc that I am giving viewing access to with 3 different tabs… bull case, base case, and bear case.