Zeta Global Holdings (ZETA): Updated Thoughts, Valuation & Why It's a 3x Opportunity

Here's why it's a top 6 position

ZETA released Q4 earnings last week so I thought now was the perfect time to write my updated thoughts on the stock after basically being flat for the last year.

Like a couple other stocks in the portfolio (LMND and SOFI), ZETA has been punished on some quite stellar results. I want to reiterate how strong this business is today and why I feel extremely confident owning this one for the foreseeable future.

For reference, here’s the first article I wrote on ZETA back in 25th July 2025.

Paid subscribers will know that ZETA is a top 6 position for me. My average cost is currently $16.52 so I’m currently just slightly in the green on the position.

Company Name: Zeta Global Holdings

Ticker: ZETA

Market Cap: $4.61B

Headquarters: New York

Shares Outstanding: 244M

CEO: David Steinberg

Revenue Growth: 25.4%

| 美股之家")

Outline

Introduction

Q4 Numbers

Opportunities

Valuation

Technicals

Introduction

Let’s start big picture.

Phase 1 of the AI trade has been very simple. More GPUs in more data centers as quickly as possible. The call was simply that model performance scaled roughly in line with computer so hyperscaler capex and the “picks and shovels” complex (NVDA, SMCI, memory, optics) would also be huge winners.

That trade has played out and it seems like that trade is still playing out. Whether we’re in the early innings of that trade or not, I’m not completely sure. I’m still very bullish on optics, interconnect, energy, and the power grid upgrade etc.

You can see my stock portfolio and basket of themes here.

Anyhow, over time inference is getting structurally cheaper and access to GPUs at some point will no longer be where the edge is.

The next phase, of which I think we’re in the early days, is about who knows how to best use cheap and abundant AI. As open source models catch up to frontier systems for many workloads, and hyperscalers squeeze economics at the model layer, the economics migrates upwards.

The next stage of value will accrue to the companies that can turn a generic model into a durable, high margin workflow. Those that can embed agents into the day-to-day tools.

That’s why the application layer is where a lot of my portfolio weighted towards. The real moats are going to be about:

Data

Products

Running these products cheaply enough that unit economics improves with scale

This is Agentic AI where systems do the work and those who do it best will be built on a layer of extremely valuable data. It’s why LMND is my biggest position. It’s why I remain bullish on PATH. It’s why ZETA is a big position.

That’s the big picture.

Now let’s talk ZETA.

ZETA sits perfectly in this AI application layer. ZETA sells an AI powered market cloud. Most big marketing firms today have a mess of system (a CDP, an ESP for email, separate tools for SMS, one media buying platform, and a stack of reporting tools for example). The inefficiency in this is that each has its own data model and none of them truly share data.

Zeta’s solution is Zeta Marketing Platform - a single environment where identity resolution, data enrichment, segmentation, orchestration, and media buying all sit on the same level and are all orchestrated by Athena (conversational AI that rides on top).

Think of how the process of marketing works today and you’ll start to see the vision for this $4B company.

Let’s say the Head of Marketing at company X wants to figure out which demographic to target this week and via which channel or which offer. A simple question.

Today that would involve:

Data engineer pulling a cohort from a data warehouse.

Marketing operations recreating those segments in an email or ad tool.

Campaign managers launching experiments.

That’s an overly simplistic answer, but I hope you get the point. It’s also a process that will likely take 1+ weeks.

With ZETA all you have to do is ask Athena that question directly. Athena then orchestrates the entire operation to understand first-party data, work out models to score who is likely to convert, and identifies behavioral signals.

This only works because the core of ZETA is the data layer. The Zeta Identity Graph spans over 245 million U.S. adults which equates to trillions of real-time data points. This allows ZETA to take an anonymous website visitor and turn them into a real person with a known history, collapsing fragmented data into a single, persistent Unified Customer View. Once this identity is locked, the ZMP turns marketing into an automated flywheel where Athena can sense a customer’s intent and instantly optimize the entire marketing they see.

The real moat here is the data flywheel. Every new customer and use case makes the models better which improves outcomes and improves the return for customers (which is already at 6x). Economically, this data flywheel is obvious if you look at the number of +$1M customers as ROI becomes more clear to them. That’s why we’re seeing consistent beat and raise quarters.

It’s the numerical sign of an AI application business that is compounding extremely well. If management keep executing like they have been, then investors will continue to get a high recurring revenue mix, higher margins, and an application layer that is becoming the operating system for many Fortune 500 companies to deploy their marketing budgets.

Q4 Numbers

Demand:

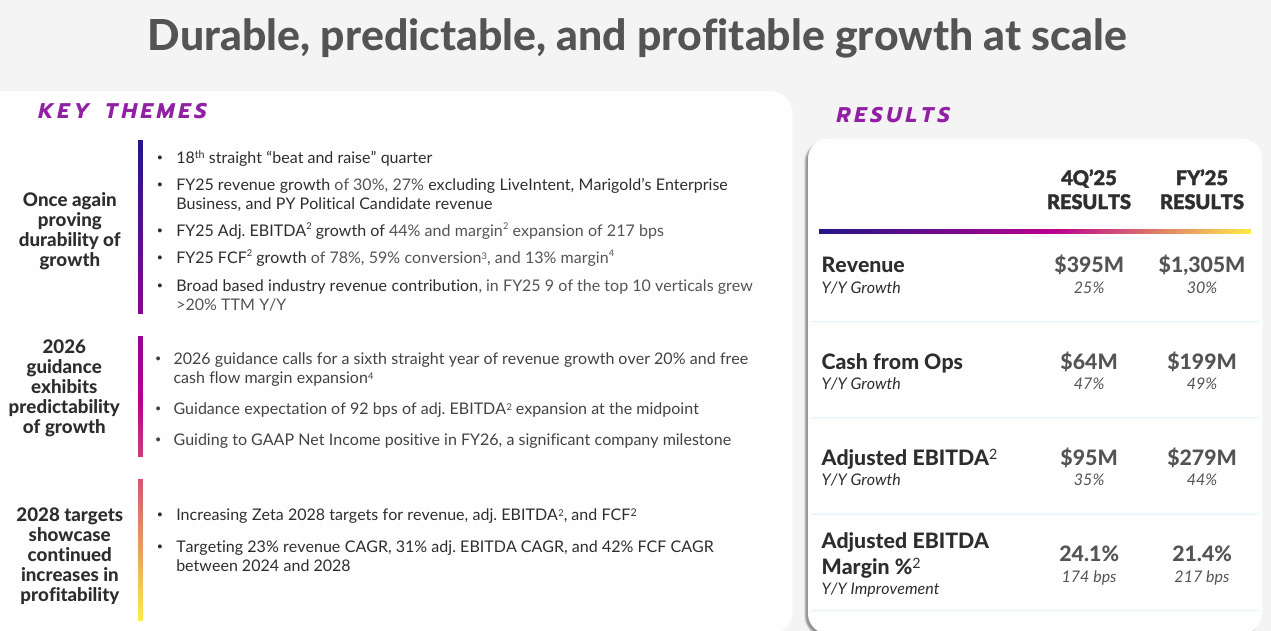

Q4 2025 revenue was $395M, up 25% YoY.

FY25 revenue was $1.305B, up 30% YoY excluding Marigold.

Revenue CAGR FY22-FY25 was 30%.

16 consecutive quarters of +20% YoY revenue growth.

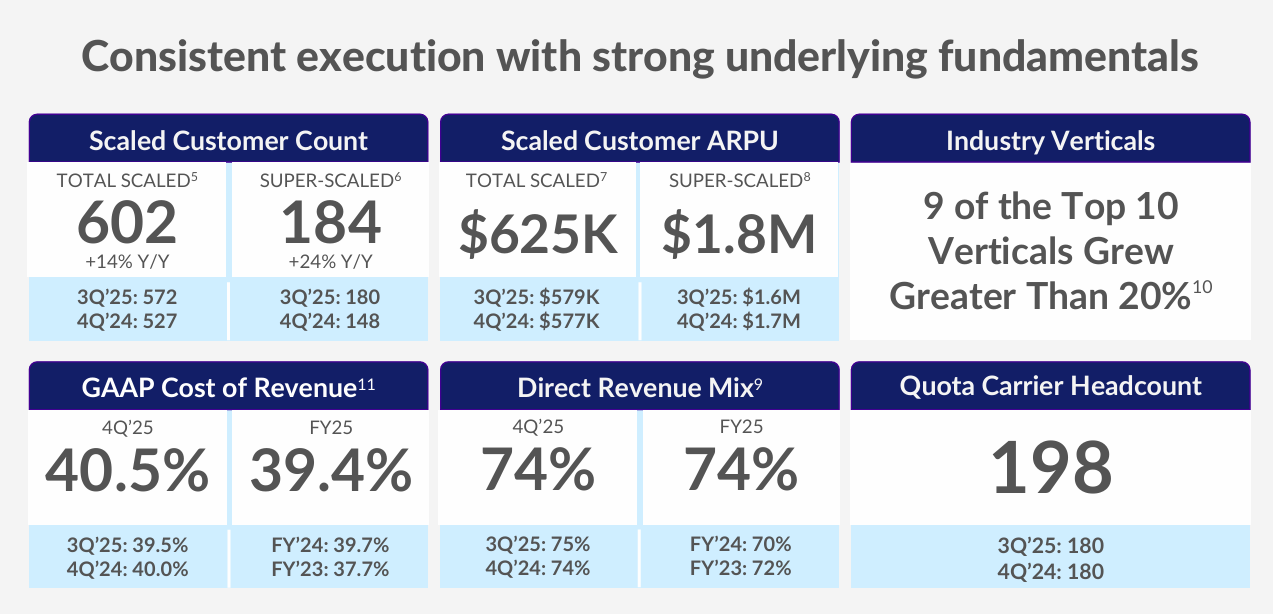

Scaled customers (+$100k) up 14% to 602. Super-scaled customers (+$1M) up 24% to 184.

Now serving 51 of the Fortuna 100.

“Net revenue retention hit a record high of 120% in 2025, up from 114% in 2024…Customers are spending more and new prospects are showing up faster, both signals of the same thing - that ZETA operating system is working, and working at scale.”

Profitability:

Q4 2025 Adj. EBITDA was $95M, up 35% YoY.

FY25 Adj. EBITDA was $279M, up 44% YoY.

Adj. EBITDA CAGR FY22-FY25 was 45%.

FY25 FCF up 78% YoY with FCF margins at 12.6%.

Guidance:

FY26 revenue guidance midpoint is $1.755B, implying 35% YoY growth.

FY26 Adj. EBITDA guidance midpoint is $391M, up 40% YoY.

FY26 FCF guidance is $231M.

Guiding for positive net income in FY26.

2028 targets revenue at $2.3B (23% CAGR from 2024) and Adj. EBITDA at $573M (31% CGAR), with FCF at $371M (42% CAGR).

These guided numbers alone are very impressive. I’ll make sense of it all for you in the valuation section below.

But to paint the picture even more now…ZETA presented at the Morgan Stanley Technology conference just a couple days ago. Here’s a couple key snippets:

“To be clear, our 603 global enterprise clients spent $100 million in marketing last year.

Last year we had 1.3% of that wallet share, this put us to about $1.3B in revenue…our clients are growing about 10% a year. So you would say that grows to above 1.6-1.7% of wallet share.

Our long-term goal is to get to 10% of wallet share or build a $10B/year business with 30% operating margin and +75% of that into free cash flow.”

More on all this below in the valuation section. That’s the bulk of this article in terms of value.

Take a look at my March database and portfolio. You get all this for just $24 a month:

Portfolio (real monetary amounts with 100% transparency)

Watchlist

Theme tracker

Valuation models

10+ themes with stocks per theme measured by valuation

Daily notes in the paid chat

1 video chart review per week

Opportunities

TAM

“MarTech” covers an entire stack - CRM, CDP, marketing automation, analytics, performance measurement, content management, and AdTech. The common problem across that stack is that data doesn’t talk to itself well enough. Each new channel or vendor adds another silo and another interface that very few companies can turn into a single coherent decision system.

The specific TAM for ZETA is hard to gauge… my assumption is that David Steinberg as per the quote above tags it about $100B today. Some estimates suggest the entire MarTech niche is $450B today with forecasts approach $1.3T by 2030 at ~20% CAGR.

If ZETA simply grows in line with the market holding share, that math alone gets you to ~$22.1B in revenue by 2032 assuming 1.7% wallet share of a $1.3T market. I think the $1.3T assumption here is probably overstated but it shows the size of the MarTech niche in general.

More realistically, with a little over $1.3B in revenue today against a market measured at +$100B, ZETA’s current share is only at 1.3%. If they can compound faster than the market and move the needle from 1.3% to 5% (modest improvement relative to long term goal), the revenue opportunity becomes extremely substantial.

Profitability

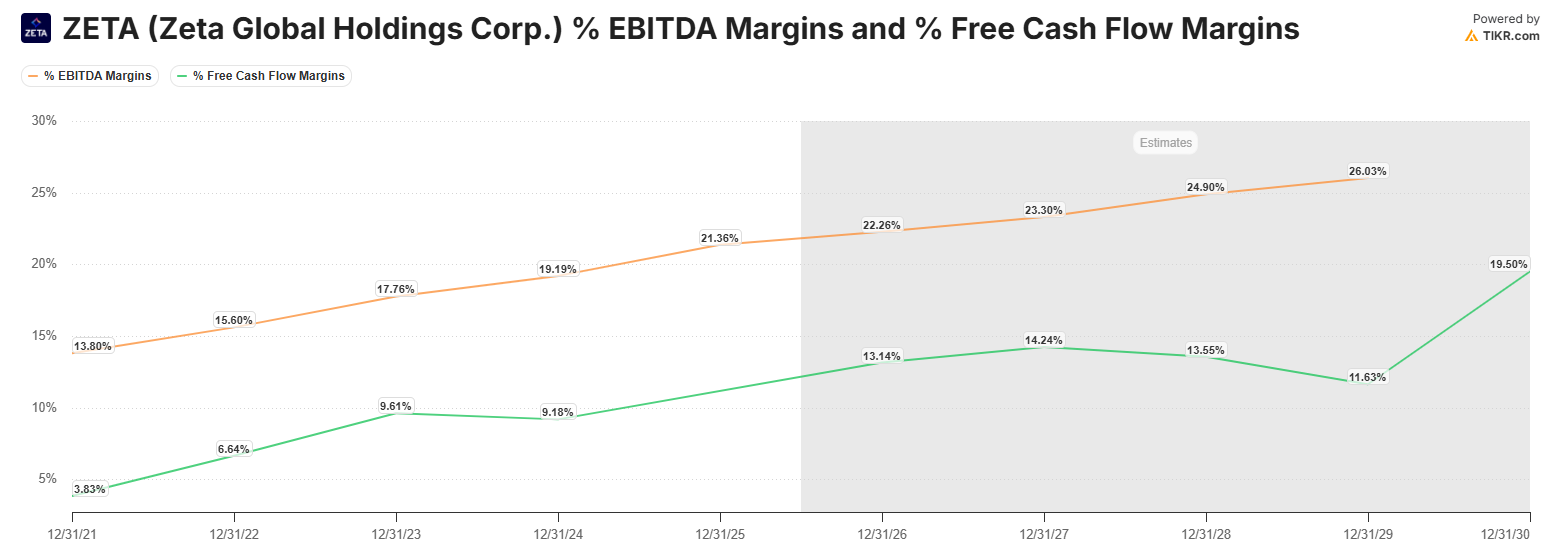

The trends in profitability are very clear.

Here’s the margin growth which revenue has CAGR’s at +30%. P.s. I use Tikr for most of my charting and estimates.

Management’s 2028 targets explicitly assume that EBITDA and FCF continues to grow faster than the top line which is exactly what you’d expect from a business with the characteristics of ZETA. Crucially, most of this growth is set to come from doing more with existing customers, not spending heavily on CAC. Super scaled customers now contribute close to 90% of revenue, up from 70% in 2020 and their ARPU is 17x the $100k-$1M cohort.

As these customers adopt more channels and more autonomous workflows, the contribution margin on incremental revenue should continue to improve quite impressively.

It’s the same playbook we’re seeing with LMND, SOFI, NU etc.

M&A

In 2025, ZETA acquired Marigold for $32.5M. Strategically this added 100+ large enterprise brands, deepened the footprint in loyalty and retention, and expanded ZETA’s EMEA presence.

We’ve so far seen 18 acquisitions in the last 18 years… and David Steinberg seems to suggest we’re on track for a 19th this year. I’m never normally a fan of M&A…I naturally prefer organic growth but when management teams successfully prove over and over again they are strong at M&A, there’s no argument against it.

Valuation

The important bit…ultimately what it’s all about.

I’m going to split this section up in to three:

Comparison against other Marketing public companies

Comparison against other AI Applications peers & high growth names

Assumptions and model moving forward through to 2030

Marketing Peer Group

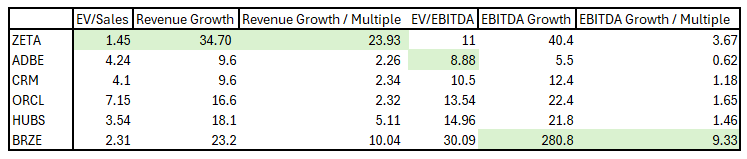

Direct peers: ADBE, CRM, ORCL, HUBS, BRZE

Quite clearly compared to ZETA’s peer group, ZETA is in a league of their own in terms of revenue growth especially relative to multiples. From an EBITDA perspective, they’re growing far quicker than all aside from BRZE which is expected to grow EBITDA at 280.8% this year though they have an EBITDA multiple nearly 3x ZETA’s which I wouldn’t be comfortable buying with where the market is today. The BRZE EBITDA margin is also far below ZETA’s by about 19 bps.

High Growth Peer Group

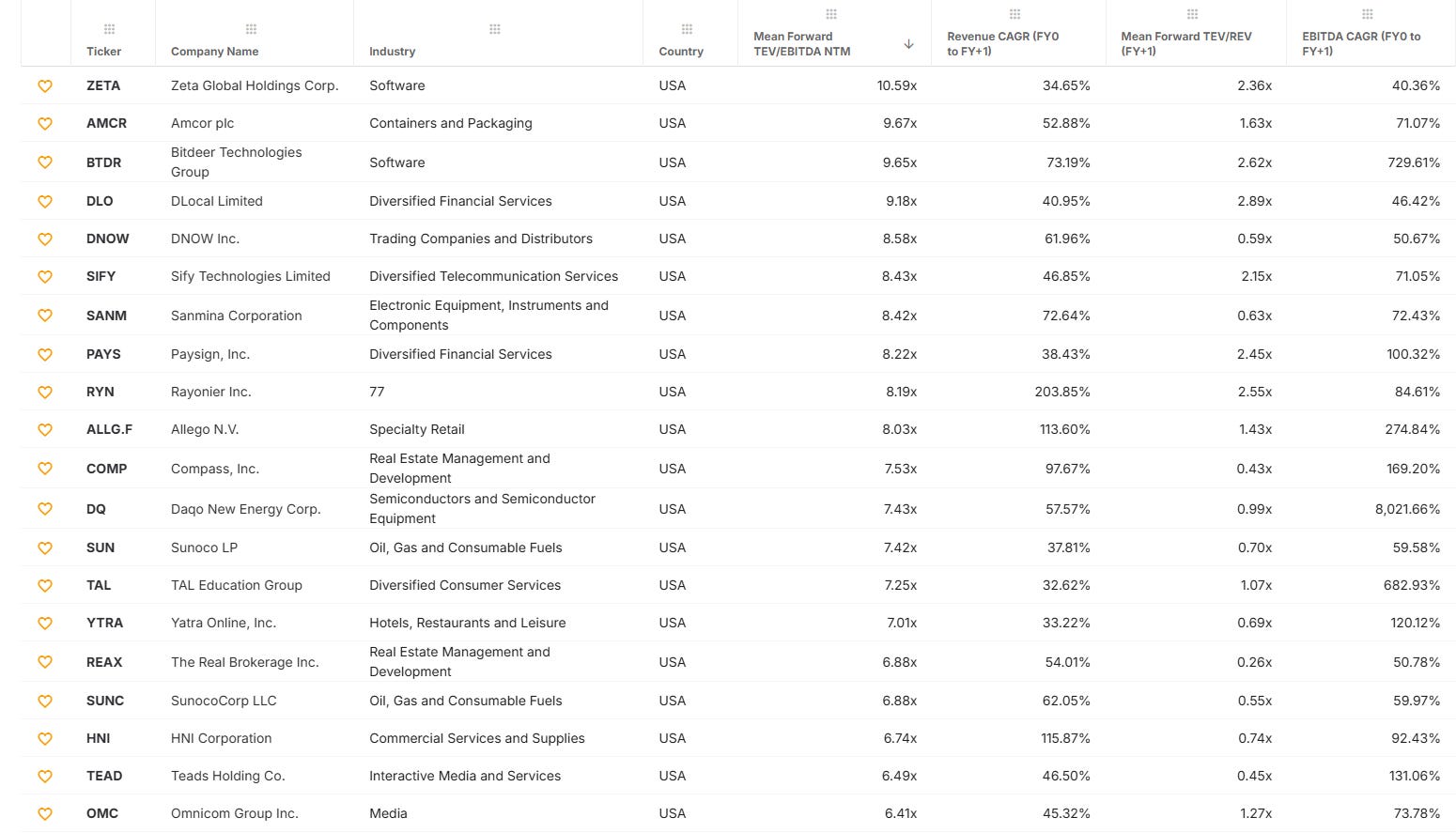

To make this easier I ran a screen on Tikr for the below criteria:

Revenue growth above 30%

EBITDA growth above 40%

Revenue multiple below 3x

EBITDA multiple below 15x

Here’s the results:

I then filtered this list down further for companies with an EBITDA margin ABOVE 10% (ZETA sits at +20%). The list then becomes:

AMCR

DLO (portfolio)

SIFY (Indian based information and communication technology company)

PAYS

OMC

ZETA

This puts ZETA in a league of their own in terms of growth to valuation.

Let’s now look at everything we know and decipher a 2030 target for the stock.

Assumptions

Management’s 2028 targets are:

$2.3B in revenue

$573M in Adj. EBITDA

$371M in FCF

Let’s focus on EBITDA to start.

If ZETA hit $573M in EBITDA by 2028, that implies a 31% CAGR from today. For most regular high growth stocks I’d anticipate a multiple ~0.5-0.8x the growth rate. For ZETA, that hasn’t been the case yet but I think the market will rerate accordingly.

If my assumption is correct, then we should get ~23x multiple on $573M in EBITDA which equates to an EV $13.32B (or 3x from today) by FY28.

Alternatively, we can focus on FCF where we’re looking at $371M by FY28 at a 42% CAGR and a 16% FCF margin. To 3x from here with $371M in FCF, it takes a 35.6x FCF multiple which at that CAGR is very reasonable.

For reference, a company like NET is growing FCF at 41% but trades at a 171x FCF multiple. SNPS is probably a better example at 41x for 45% FCF growth in FY26 (note that is FY26 growth and not a 3-year CAGR).

Both of those assumptions make it quite clear that a 3x is entirely possible in the next 2-3 years.

And this is also only looking out to 2028 with revenue at $2.3B. If you’re prepared to hold longer, and have trust in management and trust in the trends continuing at the rates they have done for the last 2-3 years, then this is a reminder that Steinbergs longer term goal is a $10B/year business at 30% operating margin.

This produces $3B a year in net income which is only slightly below the market cap today. I think the big next question is when could we assume $10B/year in revenue. My best guess ~2035 assuming a 18-20% CAGR from 2028 target of $2.3B. This could be much sooner though depending on M&A.

At $3B a year in operating profit, assuming net dilution of 3% (with active buybacks), I think we have ~300 million shares outstanding by 2035. $3B / 300 million is an EPS of $10. If they’re still clearly outgrowing peers by this time, then a 25x multiple I think is fair. I think the big question is more surrounding how the overall market deals with the AI revolution. For me, that’s the biggest bear case for my AI application layer stocks.

Maybe a 25x multiple is quite rare by that time, and a 15-20x multiple is more reasonable which puts the stock price in the $150-$200 range. All very reasonable.

Short term, 3x. Longer term, 10x.

Excellent 👏👏👏

Thanks for the research, very comprehensive and compelling. The FCF growth is incredible, ZETA is a cash cow…