Alibaba Deep Dive

Here's how much BABA is undervalued

Hi fellow investors👋

Want to see previous articles I have wrote?

This is my first deep dive of 2025. You can expect me to give you 1 deep dive per week along with 1-2 other articles per week (screens + market summaries for the week). I’ll aim to do about 45+ deep dives over the course of the year so as a paid subscriber you’re getting each deep dive for ~$5. That’s less than a cup of coffee.

In addition to my newsletter, I’m also very active on X heading towards 40,000 followers hopefully in the next couple of weeks. You can find me on X here.

Company: Alibaba

Ticker: BABA

Stock Price Today: $80.53

Stock Price High: $307

% drawdown from high: 74%

Market cap: $199B

Layout of this article

Brief Summary

China Analysis

My Take on China

Alibaba Introduction

Alibaba Financials

Alibaba Segment Analysis

Valuation

Brief Summary

I think it goes without saying that excluding the Chinese macro environment, Alibaba is incredibly undervalued. However, we have to be diligent when investing into a country that does have a lot of risks, particularly government risk, and is in the midst of a fairly low single digit growth era. Whether there is substantial upside in the Chinese equity markets or whether there’s too many risk factors is what makes this market such an unknown. However, with investing comes unknowns and it’s up to the individual investor to come up with their own conclusion on the matter.

This first section of the article will focus solely on the macro environment in China. I’ll do my best to make this an extremely fact based analysis without any bias and I’ll of course give you my opinion too on where I see the Chinese economy and the Chinese equity markets.

China Analysis📊

Before we get into this section, I want to admit that I’m no macro expert so any macro experts who disagree or can add any comments to this information, please do not hesitate to reach out.

The below chart is a nice summary of exactly what is happening in China👇

As you can see China’s GDP grew at 4.6% in Q3 2024 which was below Q2 and Q1, and below the average of 2020-2023, and below the Chinese goal of 5%. The obvious downside of this is that GDP growth is slowing but 4.6% growth isn’t too bad... (USA is 2.8%, India is 6.6%, Japan is 0.3%, UK is 1.5%, France is 1.3%, Brazil is 2.3%). Relative to China’s previous years of 6%-8% though, this is of course weak.

What was most surprising to me was this:

A GDP growth in China of +5% contributes to 34% of the global GDP growth. If this doesn’t highlight the size of the China economy relative to the rest of the world, I’m not sure what will.

Industrial Production

Domestic demand rose slightly back into the “expansionary zone” after a 9 month period. This is of course a positive sign reflecting growing demand in construction, infrastructure, and alike and is a strong sign that China can become a consumption driven economy, rather than reliance on exports, which at this time in geopolitics is probably a good thing. However, of course China is still mainly an exporter.

We’ve also got to take this with a pinch of salt for because it perhaps shows China’s growth is still concentrated in specific heavy industries like manufacturing, whereas in high growth areas like tech (which we will talk a lot more about here because of Alibaba, they lag).

Nevertheless, the numbers are fairly positive and China has to take what they can get at the moment.

Tariff’s

This is a big talking point with news of 60% tariffs being Trump’s plan. Realistically, we have no idea but what we can do is present a balanced approach on how these would affect China and the US. UBS pointed out that a 60% tariff would halve China’s growth rate, but what people are missing is that a 60% tariff would also massively disrupt the US.

The above shows the current tariffs of US against China, and China against US. 60% would be a ginormous ramp up.

As touched on, China is now very reliant on exports given the weakness domestically. Many argue that the US only accounts for 15% of China’s exports, but the US are by far the single largest country on China’s export list, 3x larger than the next. It would have a very material impact on China’s GDP. Whether or not that will affect the stock market returns over the next 4-5 years is a completely different question, and even more unknown.

It’s probably worth pointing out that the consensus is that a 60% tariff is highly unlikely and is going to be more of a negotiating tool more than anything else. It’s also not beneficial for the US. As JP Morgan have stated, China account for 13.5% of all imports to the US. This would translate to 33bps upside for core inflation. Not what the US want right now.

Foreign Investment

Outbound direct investment (ODI) is something I follow quite closely as someone with less macroeconomic experience and knowledge because it’s a positive indicator that foreign investors still have confidence in China even though FDI (foreign direct investment) continues to trend downwards ever since late 2022.

One of the arguments I see scattered all over online is that FDI is decreasing which is completely true. There is much less investment from foreign entities into domestic Chinese businesses. The downsides of this trend are:

Historically FDI has boosted GDP, so there’s weakness here.

Lack of innovation and job creation.

Weaker integration into global supply chains

Of course FDI is positive, but if China want to evolve into becoming a tech giant and a service based industry, they can’t be the “world factory” as they have been for the last 15 years. FDI on the decline is therefore not a bad thing.

ODI on the rise signals this transition towards investment into tech focused and green industries.

Real Estate

The property market represents 23% of GDP, and is therefore a leading indicator of general growth and sentiment around China domestically, and internationally.

And well…there’s a property crisis in China and the stimulus and rate cuts over the last 12 months likely won’t increase consumer spending enough. Here’s a pretty worrying graph:

The main issue is all about investor confidence. The Chinese people don’t have the confidence that developers can complete purchased homes and that house prices will not continue to fall. Despite some improved fundamentals, a lot more data and time is needed to spur purchasers confidence in property as an investment.

Stimulus

In response to the economic headwinds in China, the government has consistently introduced a set of stimuli to support consumption, investment, real estate, and capital markets. The stimulus news definitely gave the markets a short term boost as stocks like BABA rose ~20% in the weeks after the stimuli. However, as I’ll speak about in the section below (My take on the stimulus), these moves weren’t prolonged as the stimuli isn’t exactly what is required.

Here’s a brief summary of the recent stimuli:

Cut the required reserve ratio (RRR) by 50bps. The RRR is the minimum percentage of a banks total deposits that can be held in reserve.

A debt restructuring plan to resolve $14.3 RMB ($1.93 trillion) in government hidden debt.

A relending program of $68 billion for equity buy backs for companies in China.

Lowered the minimum down payment ratio for a second home to 15% and reduced mortgage rates by 50bps to aim to boost property spending.

SOE bank recapitalization (injecting capital into state owned banks to de risk them).

My Take On China

The previous part of this report was mostly facts and figures. Here’s what I think👇

Many of the narratives of China “dying” and being completely “uninvestable” are wrong in my opinion. Firstly, as I showed you above, BABA is growing economically and they’re growing quite well. Compared to previous periods, they’re growth has slowed but they’re still a fast growing, digitalizing nation.

I spent time reading threads online from people in China, and what I can gather is that the economy isn’t performing badly at all. Tourism is high. Domestic tourism is high. People are spending. Consumer confidence isn’t so bad.

As always though, sentiment on a company (or country in this instance) and as the China stock market continues to drop, so does people’s opinions on China.

One issue that I do think is most hindering to China is deflation. Property prices are down 9%c, car prices are down 5.8%, and food prices are down 5.9%. Whilst this is arguably great for the average person in China, it’s not good for growth and it never will be.

The reason for this is there’s limited upsides of growing wealth in China. You can get great food, and good cars for a fraction of the price in the US. For those who have invested in the stock market or property market, they have lost wealth. All in all, this means individuals are living a moderate easy life in China. Productivity is down and talent is down. It’s destroying demand which will continue this cycle of deflation and cause the economies growth to slow even further than what it was. Remember China had GDP growth of +8% a in the 2010s when productivity was booming.

That’s the first issue I wanted to touch on.

The second issue is the stimulus which the China government introduced in late 2024.

To be honest, all the stimulus did was prop the markets up for a week or two until people realized there wouldn’t actually be much change. All the stimulus did was allow publicly traded companies and financial institutions to seek funding without relying on the capital markets. Nothing materially changed and I don’t know if there is any plans to materially change anything.

I think the situation in China is very complex, and I’d be naive to think I understood it all. At the end of the day, no matter what numbers you look at, no matter what headlines you read, China is a communist country and they do things very different to the Western world. They do not prioritize the markets and will likely not introduce a stimulus that improves the market. The government is entirely focused on the people of China which is why prices are low. People in China can now afford to live a more comfortable life in urban areas without working as much and this is exactly how the Chinese government sees it. Not the headlines we see in the Western world.

So, to flip that. China is a communist country, with weak growth, deflation, low productivity and a terrible housing market. So why would I look to invest in a country like this….?

Because it’s incredibly undervalued and full of deadweight companies that the Chinese Communist Party doesn’t care about.

As long as you invest in a company within China that is net positive for China as a whole, I do believe these investments will pay off. BABA is a company that is net positive for China and if the CCP wanted to truly attack it, they would have done already. The markets are immensely undervalued.

I also see full potential in China being the leader in AI over the US, but they’re not there yet. The next 12 months should see models develop further and compete more favorably with the likes of OpenAI, and Google. There’s a number of issues Chinese developers need to solve, arguably the most important being the restrictions on GPUs imposed by the Biden administration. There’s also the issues of lack of investment, data centers, cloud-computing facilities, advanced networks, cybersecurity etc. Compared to the US talent of Google, Meta, Amazon, OpenAI etc, China are way behind.

The fintech and EV space are looking a lot more positive for China. It’s likely that China are world leaders in both industries.

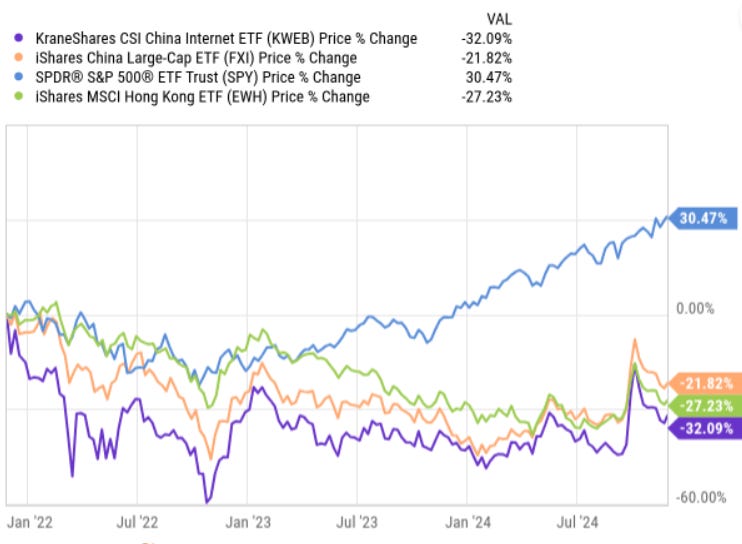

Alibaba | BABA

This link above to StocksGuide is an affiliate link meaning if you purchase anything through this site I may directly benefit.

Introduction

I have a position in BABA as I’m sure you may know, unless you’re new here. It’s not one of my largest positions, but it’s definitely not one of my smallest.

I first bought BABA in the mid to low $70s back in early 2024 and have not added or trimmed much since then. I have considered adding to my shares, but ultimately decided I didn’t want to expose myself to more risk in China as I’ve explained above.

But fundamentally, BABA is a company that has now returned NEGATIVE 20% over a 10 year period. In that 10 years:

Revenue has gone from $8.5 billion to $130.35 billion - a 15.3x increase.

Free cash flow has gone from $3.3 billion to $21.6 billion - a 6.54x increase.

EPS has gone from $1.84 to $4.33 - a 2.35x increase.

What’s happened is in the past, and the market is forward looking so I need to get over the fact that a stock has DROPPED 20% despite a 15.3x increase in revenue and focus this article on what I think the company can do over the next few years in terms of technology advancement, operational efficiency, and growth.

Alibaba is one of the most diversified companies in the world. Think of it this way👇

E-Commerce

Taobao - C2C retail online. Like

Tmall - B2C online e-commerce connecting international and Chinese brands with consumers.

Alibaba.com - Global wholesale platform connecting buyers and sellers.

AliExpress - International retail platform allowing worldwide consumers to purchase from manufacturers in China.

Lazada - E-commerce in Southeast Asia.

1688.com - Wholesale marketplace serving SME’s in China.

Idle Fish - A platform to buy and sell second-hand goods.

Cloud and Technology

Alibaba Cloud - Cloud computing services (data storage, processing, analytics etc)

Digital Media & Entertainment

Youku Tudou - One of China’s leading online video platforms, offering a wide range of user-generated content.

Alibaba Pictures Group - Film and television production, distribution, and marketing.

South China Morning Post - An English-language newspaper based in Hong Kong.

Logistics

Cainiao Smart Logistics Network - A logistics data platform.

Financial Services

Ant Group - Operating Alipay, one of the worlds largest digital payment platforms.

Local Services

Ele.me - Online food delivery and local services platform

Amap - Digital mapping and navigation.

There’s truly not many companies as diversified as this, across industries that have fairly limited correlation. To me, they’re the Amazon of China and companies like Amazon will be around for a very long time.

There’s lots of reasons I’ve invested into BABA, so before I make this a paid only post, let me run through them quickly:

The BABA valuation is quite frankly insane, even considering the China risks and applying a large China discount.

Alibaba is a diversified tech company. Not a Chinese e-commerce company. Once some of these smaller unprofitable companies turn profitable, people will realize this. A tech company will always trade at a much higher multiple to an e-commerce company too.

BABA has weathered the weak macro environment in China excellently growing revenues on average 16% CAGR over the last 5 years.

The BABA balance sheet is incredibly strong meaning they’ll be able to continue to weather the China storm, continue to invest in high growth areas, and continue to make huge share buybacks.

They’re the largest Cloud provider outside the US.

China is one of the fastest growing countries in the world, despite what people think. For all of the information on China, you can refer to Section 1.

Various other superinvestors like Michael Burry and David Tepper are investing heavily here.

BABA has been in a high capex and high R&D cycle for the last 10 years or so, but this figure is trending downwards and they’re now in a position to reap the rewards from these high tech and efficiency initiatives. We see this over and over again with companies like UBER who spent years and years, and billions of dollars optimizing their platform to then reap the rewards handsomely. Previously, BABA was completely dominant with limited competition. The story has changed now, hence why management have invested huge amounts over the last 10 years. I think looking at this graph below we are slowly nearing the end of this huge capex cycle which will of course raise profits, EBITDA, EPS etc.

Some links throughout this post are affiliate links meaning if you purchase any product on that site, it may benefit me.

Even though, I think fundamentally there’s some things to like about BABA, there’s definitely a lot of risks too:

Slowing growth

Unprofitable companies that are taking longer to become profitable than I thought

Somewhat weaker earnings

Geopolitical tensions and China risk (already covered in Section 1)

For these reasons, I’d personally keep BABA as a moderate position, but never a huge position. Just doing a very quick valuation here (they’ll be a lot more in depth valuation in the paid section below), but analysts are expecting EPS of $9.46 by 2028. With a 20x PE, you have a $189 stock. With a 15x PE, you have a $141.9 stock.

The slight trouble with using PE here is that we are negatively valuing all of the unprofitable BABA businesses which is ridiculous, so even these quick valuations I did above are lower than my fair value.

I’ll report on all of that 👇I hope you all enjoy this next section of the writeup.