PayPal (PYPL) Earnings Review - Are They Finally "Shocking The World"?

So many positive catalysts

Hi fellow investor👋

If it’s your first time coming across my page then you’ve probably missed these articles from last month:

Make sure you subscribe so you don’t miss the next one (it’s free).

Company: PayPal

Ticker: PYPL

Website: https://www.paypal.com/

Current Stock Price: $66.98

52-Week High: $75.82

52-Week Low: $50.39

Market Cap: $71.5B

Headquarters: San Jose, California

Number Of Employees: 27,200

PayPal (PYPL) - Earnings Review

“What we said at the start of the year still holds: this is a transition year where we are focused on execution and making critical choices that will set the business up for long term success.” - Alex Chriss (CEO)

Earnings

Beat revenue estimates and beat revenue guidance.

Net revenues increased 9% to $7.7 billion beating estimates by $180 million.

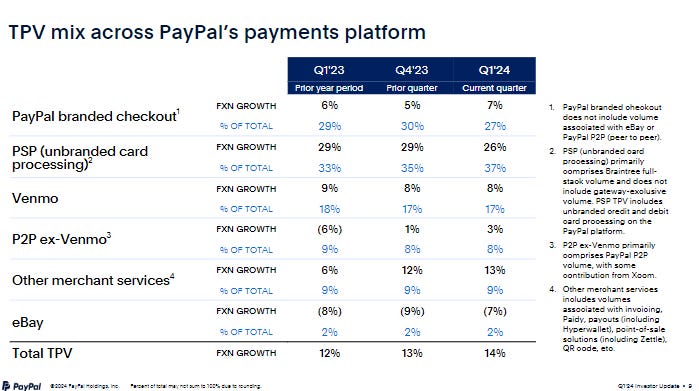

Total payment volume increased 14% to $403.9 billion. This beat estimates by 2.8%.

International total payment volume increased 17% on a currency-neutral basis.

Payment transactions increased 11% to $6.5 billion.

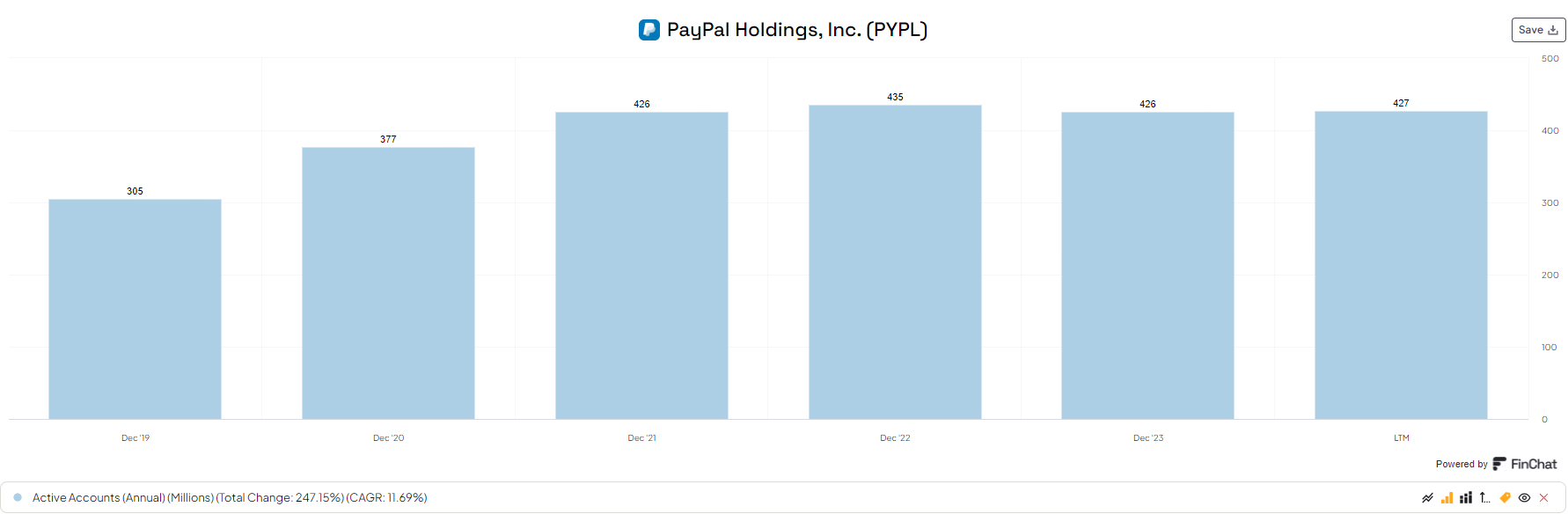

Met active account estimates, though this was a decrease of 1% to 427 million.

Transactions per active account (a trailing 12-month number) was 60 in Q1. This is up 13%.

Profitability

Non-GAAP earnings per share increased 27% YoY to $1.08.

Note that non-GAAP results now include the impact of stock-based compensation expense and related payroll taxes. This makes comps irrelevant. Under the “old method” non-GAAP EPS grew by 20%. This change by management is intended to enhance transparency, operating discipline, and also align performance with how investors actually evaluate our business. I don’t mind it either way but just note that 27% YoY increase is slightly inflated because of the change in methodology.

This growth was mainly driven by higher transaction margin dollars, control of expenses, timing of marketing spends, and interest income improvements.

Beat $0.78 GAAP EPS estimate by $0.05.

Operating expenses fell 2% YoY due to restructuring, expense discipline, and marketing spend timing.

Free cash flow is up significantly. Guidance was ~$5 billion in FCF but in Q1 alone they generated just under $1.8 billion. That “at least” $5 billion in buybacks could be much higher if this continues.

Balance Sheet

Cash & cash equivalents is at $17.7 billion.

Debt is at $11 billion.

Bought back $1.5 billion worth of stock (approximately 25 million shares) reducing the share count by 5%. Honestly, I was hoping to see a bit more than this, and especially now I saw the higher FCF figure. Maybe in Q2 they’ll up it even more.

Guidance

For the next quarter, management expect revenue to increase at 6.5% spot, and 7% on a currency-neutral basis.

Non-GAAP EPS to increase by “low double-digit” percentage. This also reflects adjustments of approximately $150 million including restructuring charges of $70 million - $90 million.

Non-GAAP EPS for full year is expected to grow at “mid to high single digit percentage”.

“We are in a transition year and we do not expect our quarterly progression will be linear.”

Earnings growth is lower for the full year vs Q2 because management intend to reinvest a portion of the strong Q1 earnings back into the business. This will limit interest income.

Increased transaction margin dollars from 0% to “slightly positive for the full year.”

Continue to expect $5 billion in free cash flow and at least $5 billion in share buybacks. This is no change.

Results in Graphs

My Review

I like Alex Chriss a lot, and I don’t think I’m alone in that opinion. He joined last year with full awareness that he was taking over a pretty messy looking PYPL. But he (and his new management team) have put the company on their shoulders and are really driving change.

He’s rapidly introduced product innovation and a new focus on the most core and profitable areas of the business. He’s also managed to convince myself, and many other retail investors and institutions that PayPal should be taken seriously again.

“We see clear opportunities for operational improvements across our large enterprise, small business and consumer businesses, including Venmo, and in driving more efficiency across the organization. But it will take time to prudently drive a meaningful and sustainable transformation. We will leave no stone unturned.” - Alex Chriss (CEO)

Let’s take a look at the progress so far:

Product Innovation

Fastlane

“Click. Pay. Get on with your day.”

Fastlane is a single sign on (SSO) guest checkout experience which Alex Chriss introduced during their innovation day back in January. The aim is to reduce checkout time by 40%. Guests can essentially move through purchases much quicker if they’ve used PayPal before with one of the millions of merchant accounts.

Fastlane is still in early testing with a select group of merchants but the early signs appear to be incredible with returning Fastlane users converting at ~80%. For context, guest checkout conversion rates are normally 40-45%.

If merchants are able to essentially double their conversion rates because of Fastlane, this will have a significant impact on their revenue. If merchants revenue increases…guess who benefits?

And this is a branded checkout option meaning higher margins that merchants will be more than willing to pay if the product is in fact as good as it seems to be currently.

Perhaps even more important is that non-PayPal users are opting to use Fastlane at a 40% rate. An important note on these impressive numbers so far is that this is just with a handful of merchants. As rollout of Fastlane becomes mainstream (in Q3) a network effect will be created and these figures should improve. In order of magnitude, these figures are already the best in the market, and I think the potential is far higher than what they’ve achieved with this beta testing already.

“We think this is the best in the market innovation that all merchants should have access to.” - Alex Chriss (CEO)

Management believe this is the best guest checkout in the market. With 60% of checkout online still being guest checkout, there’s huge potential here. Alex said they will price aggressively early to drive adoption and create a strong network effect. From there, they will normalize the price to value and begin to see noticeable improvements I’d imagine in ~12-24 months.

Just a quick note: Fastlane (and other products I talk about in this article) are not built into guidance at all. These products are strong. Very strong. Expect guidance to be raised over time.

Password-Less Authentication

In further checkout news, PYPL are making their checkout process much more streamlined by removing password requirements. They’re introducing processes like biometrics and completely redesigning the checkout experience to push conversion rates higher (as a result of a reduction in latency by 50%).

This won’t seem like much and it didn’t seem like much when Alex Chriss first introduced the plan on the Innovation Day. But this is important. People have become more and more hesitant to use PYPL branded checkouts due to the latency period. A rework of this was needed, and it’s now here.

Core Focus

Braintree

Braintree is a much more tech-forward payment service provider than PayPal allowing for far more customization and integration. Braintree can accept PayPal payments, Venmo, all major credit and debit cards, digital wallets, ACH deposits in over 130 currencies, and local payment methods. On top of this, there’s tools and services to streamline internal processes such as sales reporting, recurring billing, and integration with third-party apps. It’s an extremely good product.

Braintree currently boasts around 10% market share and is growing at solid rates (~26% in the quarter). They’ve put a big focus into improving auth rates, uptime, and reliability and have created what Chriss deems to be the best in the market.

The issue with Braintree hasn’t been the product though - it’s been PYPL’s inability to price to value mainly because the merchants haven’t been painted a full picture of what Braintree actually offers on an end-to-end strategic roadmap.

Management are therefore now fully focused on these conversations with merchants to really extract the full value that Braintree has to offer, and therefore slowly price the product at a price it deserves. Clearly, this will take time as there’s millions of merchants but for example the recent Customer 360 conference in LA highlighting innovations around these unbranded products saw a lot of positives as per management.

If this is in fact the case, there’s clear appetite for Braintree clients to purchase add-ons at higher margins and really extract the full value that the product has to offer.

Venmo

Venmo is successful, but frustratingly missing out on huge potential which is exciting for shareholders if this can be captured. It was mentioned 23 times throughout the earnings call so it’s clearly a focus for investors and management.

Let’s start with the obvious positives for Venmo. Venmo is the leading peer-to-peer platform with a massive customer basis (60 million monthly active users) with a disposable income 22% higher than the U.S. average. This all leads to $18 billion of net new funds that flow into the platform.

However, despite this base, monetization has been pretty poor. Therefore, there’s now a large focus on massively improving effective monetization.

Here’s some bullet points for you to understand:

Venmo have introduced a debit card which they are integrating with Apple Pay and Google Pay.

Use of the debit card has seen a 21% increase YoY. Solid, but more is needed. BUT only 20% of funds are still there within 10 days highlighting there’s no products or services that customers need when those funds are on the platform.

The debit card is so important because debit cardholders are far more engaged and drive 6x more incremental revenue than the peer-to-peer only customer.

So Venmo need to give customers opportunities and innovations for them to be able to keep funds within the platform, and from there tap and pay and checkout. This would then have a big impact on improving transaction margins.

Xoom

Xoom is PayPal’s product that allows users to safely, and reliably send money abroad. It’s not been performing well and has been pretty stagnant for a number of years now due to less prioritization and just a lack of clarity about the value proposition.

This is all changing it appears. They’re re-working the fee structure and using PYUSD (PayPal Stable Coin) for fee free transfers. They’re becoming more strict on which markets they work with. They’ve redone the interface to make debit card usage much more streamlined.

To be honest, compared to Venmo and Braintree, I’m far less focused on Xoom, but there’s no reason Xoom can’t be a profitable and growing business. I’m not sure exactly how much resources management are putting towards Xoom rather than the other products, but as long as we see some clarity and focus towards this product, Xoom should become a significant part of the PYPL portfolio.

An Overview Of My Opinion

12 months ago I didn’t want to touch PayPal. They were a company just going through the motions with no strategy, innovation, or growth mindset. The brand, data, and reach were not being used anywhere near to their potential. In some industries this may work, but not in the competitive FinTech space. There was a lot to fix and a lot of uncertainties for the new management and a lot of doubt from investors whether the company was recoverable.

From my point of view, I took an immediate liking to Alex Chriss. I think he’s very aggressive and proactive which is exactly what PYPL needed. And in his just 6 months at the helm we’ve already seen solid evidence of big product innovation. There’s lots of data signifying Fastlane will be incredible (shocking the world is a bit much…but it’s going to be better than lots of people realize), Venmo has a strategy, as does Xoom, and Braintree is in the process of getting priced at the value it offers.

I’m not writing this saying this turnaround is complete by any means, but I think we are finally starting to see some actual evidence and optimism for the next 12-18 months. It’s going to take a while for both PayPal to become a strong competitor again and for investors to realize this, but there’s added hope after this quarter.

Alex Chriss - keep working. We’re behind you!

I’m bullish on PYPL.

Like this article?

Here’s some newsletters I’ve been loving recently:

That’s it for the day

I hope you loved this article. As I develop on here, I’m sure there will be some changes to my structure and style, so please do leave some feedback for me.

Please subscribe to my newsletter where I provide investors with all the tools to outperform the market, and retire well before you’re 65. You can also follow me on X.

Great review, Oliver. Technically, PYPL is finally beginning to look primising. The stock completed the bottom and resumed an uptrend, albeit rather slowly. I'd be curious about the percentage of shares held by institutions. nasdaq.com should publish the data in the middle of May.

Nice review. I've never fully understood all the concerns about competition with PayPal and the multiple it's trading at. They have a massive amount of data that lets them have the highest auth rates, lowest fraud rates, approve more people for BNPL with lower delinquency and loan defaults, and they have huge amounts of consumer trust. Now they're using all that data for things like Fastlane and advertising. As far as I can tell, PayPal is the only checkout provider that can go to a merchant and say "use us and you'll make more money", with the data to prove it. That just seems like a recipe for success in the long run to me.