The Baskets: Looking Ahead to Q3 2026 (Part 2)

In this article, we’re taking a look at the MMMT high conviction baskets for Q3 2026 with a look at the underlying thesis and the stocks within them.

Part 1 was released on Sunday:

The Baskets: Looking Ahead to Q3 2026 (Part 1)

In this article, we’re taking a look at the MMMT high conviction baskets for Q3 2026 with a look at the underlying thesis and the stocks within them.

Part 2 focuses on:

Robotics

Optics

Solar

Three themes that have been hit hard by the recent market sell off.

Robotics

I think many people appreciate that robotics is a huge megatrend coming up.

But few people realize how much of a national security issue for the US right now it is…which is central to the investment thesis today.

China is currently way ahead of the US. Their 2026 humanoid output is +100,000 vs the US which is ~14,000.

That issue stems because of a few different reasons, but ultimately gaps this visible do attract policy, urgency, and capital into the theme.

The most obvious issue today is the rare earth supply chain. The US isn’t doing anywhere near enough to prioritize this issue right now but that can’t remain which is why USAR to me is a clear thematic opportunity.

But zooming out, the robotics megatrend is so vast.

I wrote about it in depth in the article attached above but a simple summary would go along these lines:

Backbone

Actuation/Bearings: Without actuators robots are just an intelligent statue. There’s only a few key players here.

Sensory & Perception: LiDAR, IMU, tactile and force sensing, analog and semiconductor sensor components. There’s many angles to play this.

Software/AI Integration: This is where the US leads now. The AI foundations are strong but the physical components that make up the robots is where the US is behind quite significantly.

Motion Control: The sophisticated chips that orchestrates a robots every move calculating how much each joint must rotate and at what speed.

Communication: The invisible layer that keeps everything connected.

Frontier:

Medical Robotics: More than just a few niche surgical aids now. It’s set to transform healthcare from surgical systems to diagnostics, to rehabilitation exoskeletons, to pharmacy automation and logistics bots.

Defense Robotics: Low cost robotic systems are now destroying high value manned assets forcing this shift towards unmanned drones.

Logistics Robotics: This will likely be the first large industry to be fully automated. AMZN alone already has over 1 million humanoids deployed.

Humanoids: Once quite an un-investable segment of robotics until CCXI went public.

Professional Robotics: The smaller, specialized, task-specific machines optimized for professional applications.

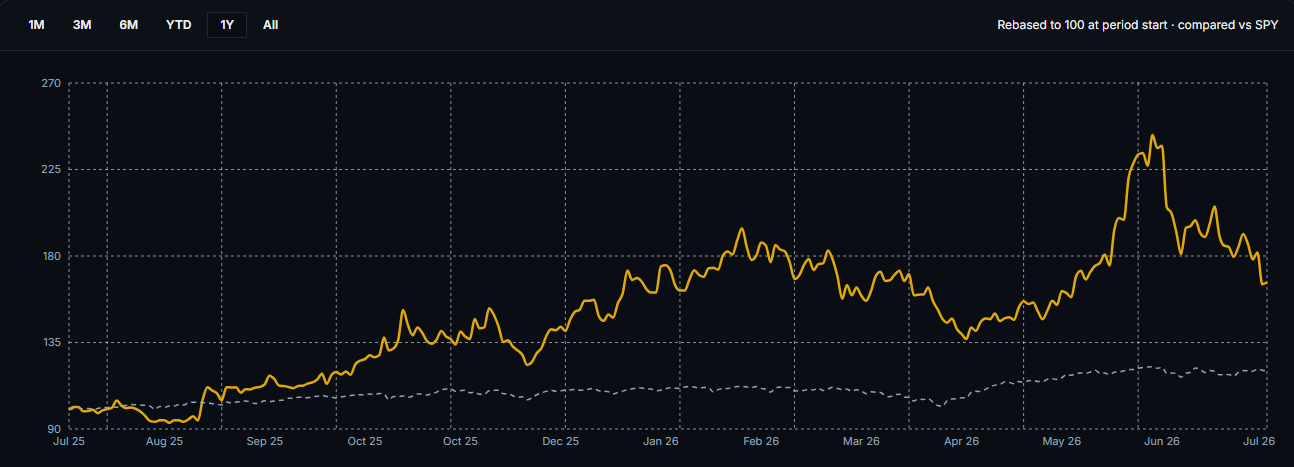

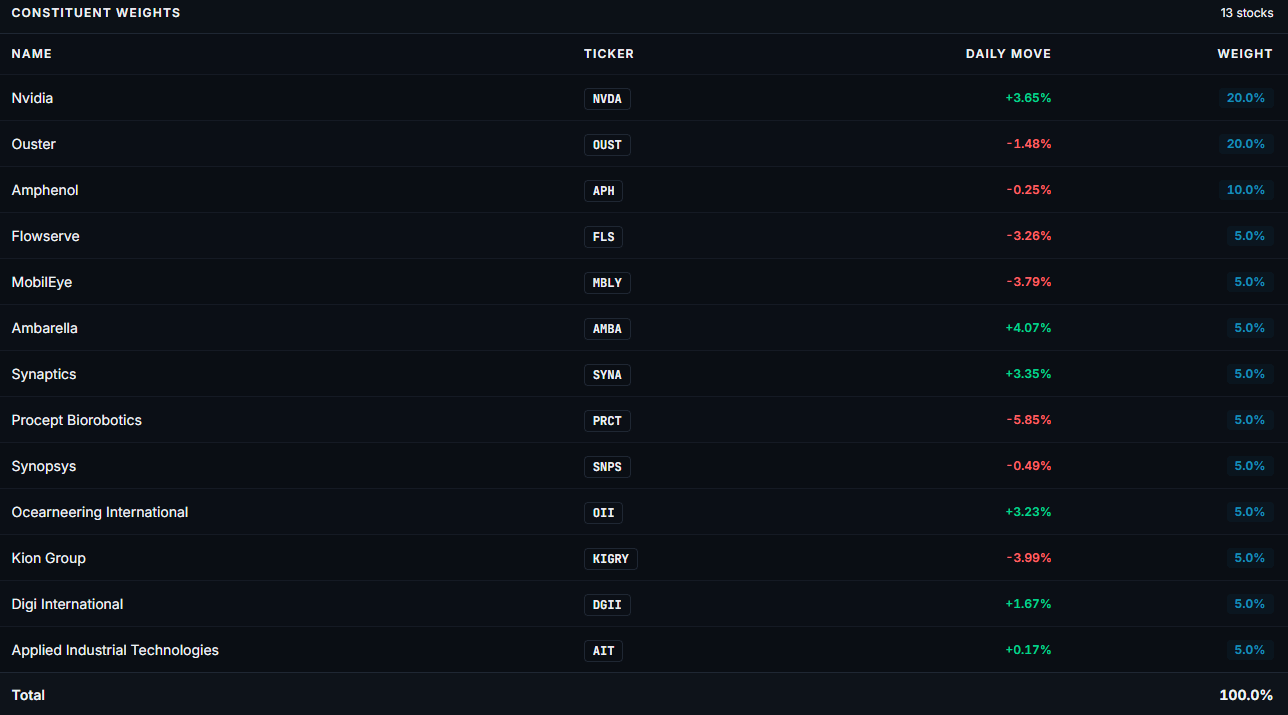

The current basket includes 13 names with 40% of the basket allocated purely to OUST and NVDA.

OUST is in my personal core portfolio as my 2nd largest position so I’m very bullish there.

You can see my prediction with OUST here:

The rest of the basket is made up of some frontier and some backbone plays like OII, DGII, AIT, MBLY, PRCT and FLS.

I’ve weighted all those plays quite small but the two that have my most attention at the moment to increase weighting for are:

PROCEPT BioRobotics | PRCT: PRCT is a surgical robotics company with one product that treats enlarged prostates. The numbers are very interesting on this one if they execute and if they can scale. Most MedTechs like this really struggle for the initial years because operating and gross margins are so thin. It’s only when scale hits that numbers start to look quite interesting. PRCT appears to be at that inflection point now.

PRCT trades at 2.3x NTM sales whilst set to grow revenue at 29% in FY26 and 24% in FY27.

If PRCT reach EBITDA profitability next year (which is expected), then we should expect ~$170M in EBITDA in FY29 based on $680M in revenue and a 24% EBITDA margin.

At $170M in EBITDA and a 20x EBITDA multiple (TMDX today trades very cheaply at 14x), we could expect an EV ~$3.4B which is 3x from today.

MobilEye Global | MBLY: MBLY is building the perception and decision making systems for autonomous vehicles and humanoid robots. It funds its frontier R&D through a highly profitable ADAS chip business. It recently acquired Mentee which is targeting commercialisation in 2027.

Revenue growth has been slow in FY23, FY24, FY25 and likely FY26. But FY27 is when the company is likely to ramp up again to +22% estimated growth which would mean a 3.3x sales multiple would be cheap.

If MBLY meets estimates of $3.8B in revenues in FY29, then they’d be growing revenues at 25% CAGR.

Compare that to a partial competitor like NXPI which is growing ~7.9% CAGR for 5.2x sales, and we start to see the re-rating potential for MBLY down the road.

Last chance to grab TrendSpider at a steep discount.

Get 38% off + $98 in free upgrades if you sign up by July 8th at midnight — once it’s gone, it’s gone.

TrendSpider is the charting platform I personally use, which has helped me spot the most in my investing.

If you manage your own portfolio the way I do, here’s what TrendSpider provides:

- Scanners that surface technical and fundamental setups before they’re obvious - the kind of early entries that turned OUST and NBIS into two of my biggest winners this year.

- Sidekick AI to dig into market data and portfolio holdings without jumping between five different tabs.

- Charting and automated technical analysis to track support levels, breakouts, and moving averages on every name you hold or are watching.

- Real-time options, sector rotation, market breadth, news, and sentiment to understand the broader market context behind any single trade.

This is one of TrendSpider’s biggest sales of the year. If you’ve been thinking about trying it, this is a good opportunity to sign up with a discount.

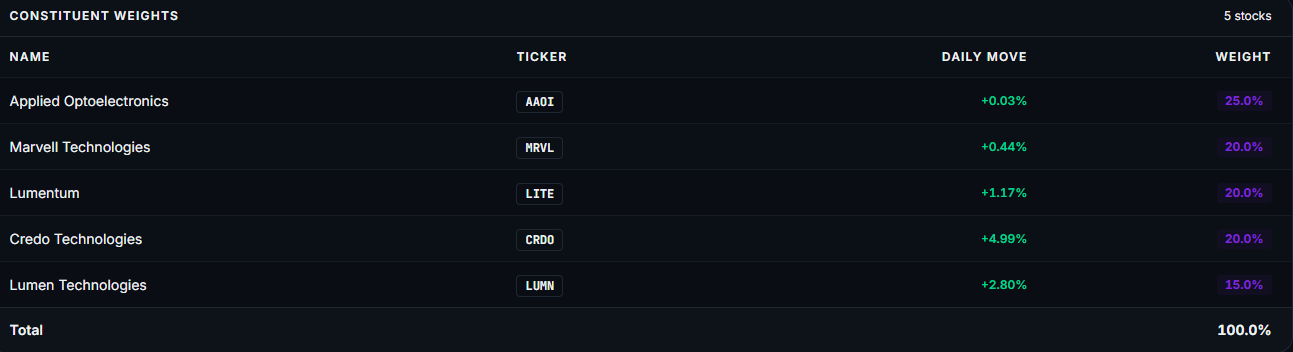

Optics

Copper can’t handle AI-scale bandwidth at 800G and 1.6T speeds which is why photonics is the solution.

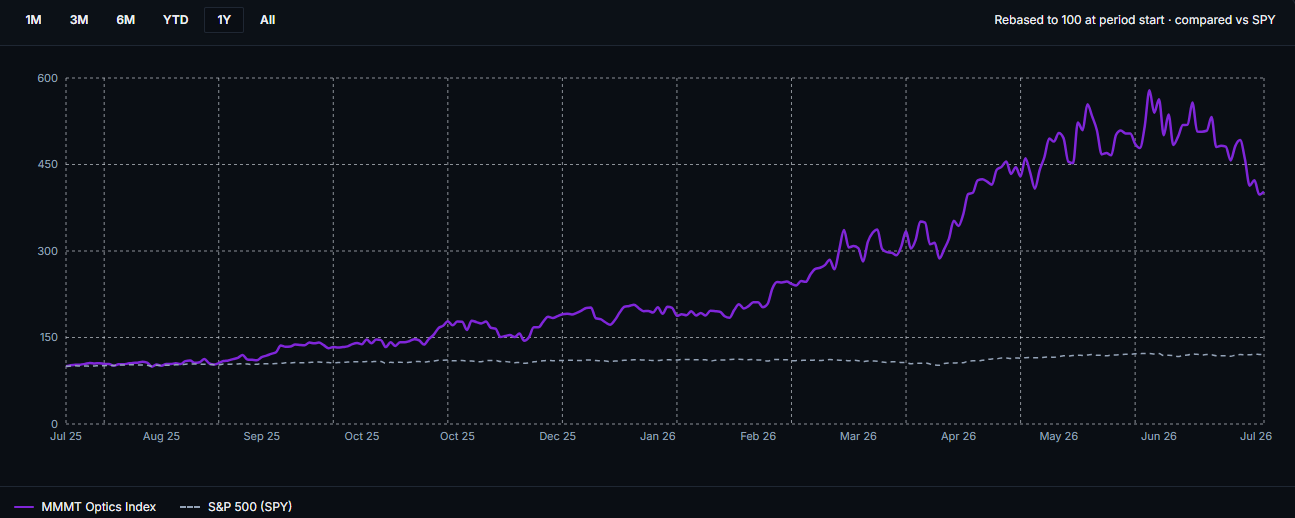

The optics theme was obviously one of the biggest winners in the entire market over the last year with the MMMT index of just 5 stocks now returning 303.1% vs the SPY at 20.2%.

This recent pullback with the likes of AAOI down ~42% in the last month is nothing more than a correction in what I deem to be a long term buildout.

The major inflection point we’ll likely see as per most earnings calls is mid 2027 as 1.6T scales and as CPO broadens past NVDA and AVGO.

Markets will likely price this ramp up before it actually arrives, which is what has happened to an extent so far, but looking at individual valuations I am of the opinion we are far from being priced in.

Here’s my optics piece from December 2025…nicely before all optics plays surged in January and February.

Optics: The Next Big Theme & The Best Stocks Today

Hi all👋Make Money, Make Time is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

My core photonics play is AAOI. It’s a stock I am down ~21% on in my core portfolio, but it’s one of my highest conviction plays right now that I’ll personally keep building out sub $130.

A few reasons for this:

If AAOI hits projections, it’s ~12x in revenue growth from $455M in 2025 to $5.6B in 2028 (that’s being conservative on management assumptions because of the timeline). There’s no other company in the market forecast to grow that quickly especially at 6.5x NTM sales today.

All hyperscaler customers want to buy all transceivers AAOI can possibly supply. It’s a supply constraint and not a demand constraint.

If you have partial trust in management, then looking at current financials for AAOI actually makes no sense. This is a 2027/2028 ramp up story likely like no other in the market. We saw it with NBIS earlier in the year and I personally believe AAOI is in the same boat, if not even more bullish than NBIS was before the recent run from $92 to $300.

Solar

Solar is an interesting, and very underappreciated trend. The MMMT Solar index is up 69.9% in the last year vs SPY at 20.2% but it’s been a very volatile ride.